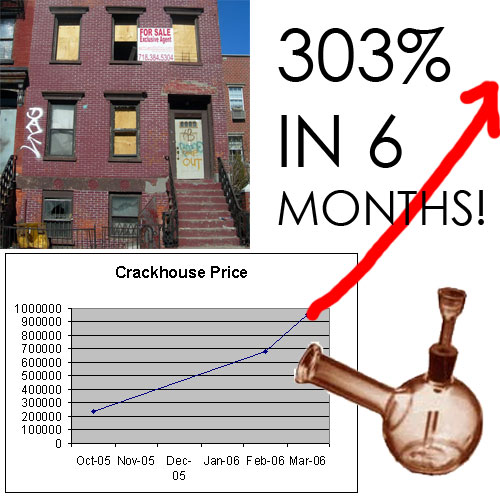

Bought in October 2005 for $235,000. Flipped four months later for $680,000 (wow, gotta love a good bubble!). Then put back on the market a few days later for $900,000 now.

Are people really THIS stupid?

Yup, they are.

Wonder how long until it's back under $235,000?

Thanks to gothamist for the reporting:

Now, does anyone else think is just redonkulously insane? How can anyone look at evidence like this and NOT conclude that a full fledged real estate mania is currently in swing and approaching its peak? How can anyone expect to buy this place, put in $1m worth of renovation, and make a profit? How can someone sell this building at this price with anything approaching a straight face? GAAAAAAAAAAAAAAAAAH!

March 31, 2006

Real Estate Bubble Reaches $1m Crackhouse Phase

The perfect housing bubble tracking site

Now you can track your favorite bubble market like you used to track your pets.com stock.

Brilliant!

Thanks popla

Let's offer to buy Baja California from Mexico

I've been floating this one for some time, let me know what you think.

I've been floating this one for some time, let me know what you think.

How did the US become the US, in terms of geography? Well, after invading and unethically stealing the land away from the native population, we went out and legitimately bought land. Louisiana Purchase, Seward's Folly, etc etc.

Well, who says we can't do that again?

Let's offer to buy Baja

I figure we've got about 20 Million illegal Mexican immigrants in our country today. There are about 2.5 Million Mexicans living in Baja. Mexico's debt burden is a crushing $173 Billion.

So here's my proposal. We buy Baja for say $300 Billion. Mexico has no debt, and can spend the retired debt service money and additional funds on services for their people, business development and infrastructure - thus getting them out of the rut they'll never get out of otherwise and stimulating their economy.

The people of Baja at time of purchase (2 years + of proven residence) get dual citizenships. The illegal Mexicans here will be encouraged to move to Baja to help build what we'll build there - jobs will be plentiful, where they definitely will not be here (post-bubble). We offer a process for ALL Mexicans where they can immigrate to the US LEGALLY after going through the legal process - mainland or Baja.

We get Baja and we build the heck out of it, stimulating OUR economy. Ports, pipelines, LNG plants, refineries, factories, tourist meccas, homes, etc. We break up California into three states - New Baja California, Southern California and Northern California.

Many details of course to work out, but start with the concept. Someone's gotta figure our way out of this mess. Here's a start.

And of course, the closed minded weirdo crowd will rip on this for being racist, as they do any ideas when it comes to solving the Mexico problem.

Pop pop fizz fizz oh what a relief it is

You just know condo project after condo project in Vegas, Miami, Phoenix, San Diego, Boston and city after city will be cancelled - some even in mid construction.

Here's yet another from Vegas announced with so much hype (pets.com anyone) - and then out with just a whimper... Anyone hear any other cancelled projects? How about those "X10 Wine Lofts" in Scottsdale - my favorite!

Clooney high-rise condos hit snag

The $3 billion Las Ramblas luxury condominium-hotel project backed by actor George Clooney is no longer taking reservations at its sales office on Convention Center Drive.

Las Vegas-based Centra Properties and Related Las Vegas formed a joint venture last year to acquire the land for $85 million. Clooney had reportedly invested $10 million in the project.

Las Ramblas was among $20 billion in condo and hotel projects to be developed along the Harmon Avenue corridor, from the Hard Rock Hotel to the Palms.

"The sales office is not closed," Related Las Vegas President Marty Burger said Tuesday. "There are lots of rumors. Don't believe everything you hear. When something is concrete, we'll call you. I can't talk about it now. Sorry."

March 30, 2006

Checking in with bubble guru Robert Shiller

Seems Mr. Shiller, like Michael Jackson "gets it" when it comes to Bubbles.

Seems Mr. Shiller, like Michael Jackson "gets it" when it comes to Bubbles.

Bottom line, he got the .com bust right, he got the housing bubble bust right, and he'll get the next bubble right too. It's not rocket science, it's just the way it is.

Robert Shiller, the Prophet of House Prices

If a prophet is only as good as his last prophecy, then you'd be wise to listen to Robert Shiller. On "Nightline," Shiller offered his considerable analysis of the current real estate market ... and he doesn't bring good news.

It was back in the heady stock market days of 1996 that Shiller, an economics professor at Yale University, gave voice to his first prophecy. He warned that the stock market was overheating and that investment had risen to what he described as irrational levels. The stock market crash that followed was no surprise to Shiller and proved that he had called it right.

Now he's warning that a similar collapse may soon apply to the real estate market. And there's evidence that he may be right here, too.

Shiller said that the same psychology that applies to stock market investors now drives the real estate boom. He called it irrational exuberance, coincidentally the title of his 2000 book about the stock market.

He argues that many first-time buyers pay inflated prices simply because they fear they'll be left behind.

Bush & Fox having a little chat about housing bubbles and immigration today

Wonder if they'll talk about what to do with the thank-you-housing-bubble-bursting, millions of soon-to-be-unemployed Mexican immigrants?

Instead of quotes from today's article on the summit, a quote from Teddy Roosevelt. Was he racist to discuss the issue in 1919? I don't think so.

"In the first place we should insist that if the immigrant who comes here in good faith becomes an American and assimilates himself to us, he shall be treated on an exact equality with everyone else, for it is an outrage to discriminate against any such man because of creed, or birthplace, or origin. But this is predicated upon the man's becoming in very fact an American, and nothing but an American...

There can be no divided allegiance here. Any man who says he is an American, but something else also, isn't an American at all. We have room for but one flag, the American flag, and this excludes the red flag, which symbolizes all wars against liberty and civilization, just as much as it excludes any foreign flag of a nation to which we are hostile...We have room for but one language here, and that is the English language...and we have room for but one sole loyalty and that is a loyalty to the American people."

--Theodore Roosevelt, 1919

UCLA Report: More than 200,000 housing jobs to be lost in California alone

I believe the 200,000 number is understated by 1 Million or more - as the ripple will be huge. Realtors, mortgage bankers, construction workers, etc are obvious. But add in Home Depot workers, Lexus dealers, beauty salon workers (someone had to primp the realtors) - and the number is big. Really big. And worldwide.

I believe the 200,000 number is understated by 1 Million or more - as the ripple will be huge. Realtors, mortgage bankers, construction workers, etc are obvious. But add in Home Depot workers, Lexus dealers, beauty salon workers (someone had to primp the realtors) - and the number is big. Really big. And worldwide.

Declines in home-building could cause as many as 200,000 construction workers to lose their jobs, as well as cause layoffs of real estate agents and mortgage brokers.

Over the past three years, the Anderson team, one of the nation's most respected group of regional economists, has issued repeated warnings about potential weaknesses in the housing market.

“The trend is clear,” Thornberg said. “The only debate now is how hard a landing there will be and what it will mean for the general economy.”

Nationwide, the UCLA economists predict that new housing starts will decline to 175 million units per quarter by the end of 2007, a 25 percent decline from the peak last fall.

“Make no mistake,” economist David Shulman said. “This is a soft landing. Typically, peak-to-trough declines amount to 50 percent.”

The "danger years" for homeowners

Tick. Tick. Tick.

Delinquencies peak the third and fourth years of mortgages. Will risky terms add to the problem?

Millions of mortgage borrowers are entering their "danger years," when delinquencies peak and owners risk losing their homes.

The number of Americans affected by the coming danger years could be huge.

In addition, many of these transactions involved risky loans, such as interest-only ARMs and no-down payment loans. "The problem is that few people recognize it for the gamble that it is," says Baker.

March 29, 2006

A note to any reader who uses foul language, racist language, sexual content or is closed minded

I'm sure Fox News, the KKK or the flat earth society have blogs too

Keep it clean, be logical with your arguments, be civil toward each other, and let's work together to expose the truth

And for the record, wanting every illegal immigrant forcibly removed from the country isn't racist. It's the law.

Cheers

Here they come... the first (of many) housing bubble jokes (WARNING - DON'T READ REPLIES UNLESS YOU HAVE A SICK AND TWISTED SENSE OF HUMOR)

Make up or post your best. Here's the first, from an HPer:

brokersleaveyoubroke said...

Question: Which of the following items does not belong with the rest?

AIDS

Herpies

Syphilis

A condo in Miami

Answer: Syphilis, it's the only one you can get rid of.

Falling Phoenix: "Cancellations rampant"

We're soaring past 40,000 unsold homes (officially) on the market, up from 5,000 a year ago. Now here come the reports of soaring cancellations and falling sales. Or, as some realtor hacks will continue to say to ignorant unchallenging reporters, a "more normal market".

We're soaring past 40,000 unsold homes (officially) on the market, up from 5,000 a year ago. Now here come the reports of soaring cancellations and falling sales. Or, as some realtor hacks will continue to say to ignorant unchallenging reporters, a "more normal market".

The latest numbers show consumers have had it with high home prices. According to the Phoenix Housing Market Letter, permits for new homes fell more than 20 percent in February compared with the same month in 2005.

“The drop was considerably more than most observers had anticipated and the industry hoped for,” the newsletter’s authors wrote. “The 3,729 permits issued was the lowest total in the last 24 months. Cancellations were rampant.” Homes that were resold also dipped more than 11 percent from 8,722 in February 2005 to 7,774 during the same month this year, the newsletter said.

The Double Bubble - Dot-Com to Dot-Condo

It's becoming more and more obvious to HP'ers that the .com crash, which really was a credit bubble, never really stopped - the mess was just postponed a bit with a second bubble (still a credit bubble) - the housing bubble. Some pretty smart (and rich) folks have identified this and are positioning themselves correctly. Some really stupid people, let's just say ones who have never read an econ book, wouldn't know a financial bubble if it hit 'em in the face, are doing the opposite and charging full speed ahead.

It's becoming more and more obvious to HP'ers that the .com crash, which really was a credit bubble, never really stopped - the mess was just postponed a bit with a second bubble (still a credit bubble) - the housing bubble. Some pretty smart (and rich) folks have identified this and are positioning themselves correctly. Some really stupid people, let's just say ones who have never read an econ book, wouldn't know a financial bubble if it hit 'em in the face, are doing the opposite and charging full speed ahead.

The leverage used by day traders and housewives back in 1999 - 2000, where $5000 would get you $10,000 in margin, was replaced by absolutely MASSIVE leverage used by condo flippers (and housewives, and strip club managers, and 21 year old unemployed kids, and ...), where $5,000 would get you a $500,000 mortgage - an INCREDIBLE amount of leverage never before seen, never before available to humanity, used by an INCREDIBLE number of people.

This mother of all credit bubbles, represented by the double bubble of .com and now .house, is now coming to an end, but too late to stave off the carnage to come. Now we'll see the ramifications, which we were supposed to see in 2001, but were delayed 60 short months, with 2007 being D-day.

Get ready. Get ready. It's here.

March 28, 2006

Add "house prices never go down" illusion to the dustbin of history

I used to love the trolls (i.e. realtors) who'd post on this site the historical US Median home price numbers, and shout "home prices NEVER have gone down - so thus they'll NEVER go down in the future."

I used to love the trolls (i.e. realtors) who'd post on this site the historical US Median home price numbers, and shout "home prices NEVER have gone down - so thus they'll NEVER go down in the future."

And HPers would respond correctly "past performance does not dictate future returns"

But, their argument was a very important part of the illusion. Buy at any price, your investment can ONLY go up. The housing ladder ONLY allows you to climb upward.

Not.

I love a good illusion too. Your eyes tell you something your mind tells you the opposite. But it just feels soooooo reaaalllll.

FYI - the grey bar is the same color throughout...

The median price of a new home sold last month dropped to $230,400, down by 1.6 percent from January and off 2.9 percent from February 2005.

“The housing market is in a downturn, there’s no doubt about it,” said Scott J. Brown, chief economist at Raymond James & Associates. “It’s just a question of how severe.”

We are living through the biggest financial bubble in history

Ponzi Scheme over. Financial collapse imminent. Bloom off the rose. Incompetence exposed.

You know what's coming, now what are you to do? How do you best protect yourself, your family, your financial well being and your future? Duck and cover?

Preparing for an Uncertain Future – Economy of Illusion

According to estimates by The Economist, the total value of residential property in developed economies rose by more than $30 trillion over the past five years. Not only does this dwarf any previous house-price boom, it is larger than the global stock market bubble in the late 1990s or that of the late 1920s.

San Diego County resale house prices fell in December by the largest monthly amount in 18 years. The median resale price for existing single-family homes dropped $15,000 from November to December to stand at $550,000, the largest month-to-month decline since Data Quick began keeping records in 1988.

The 42% of recent buyers who put no money down when buying their homes have no equity. What will happen to them if the value of their real estate falls? If these homebuyers have been using interest-only loans, they will have no protection against any kind of adverse move. Many people in this situation will have no choice other than to walk away from their property and mail the unwanted keys back to the lender.

Speculation has been increasing along with home prices. The history of markets shows us that asset markets become ever more treacherous as the number of leveraged participants increases. Leveraged participants possess no capacity to withstand adverse trends. They become forced sellers into a falling market, which pressures prices even more. This forces more speculators to sell.

Anyone else rooting for the Fed to raise rates to the moon?

It's a matter of perspective I guess. All my life I cringed when I read "Fed raises rates again". That meant houses were going to get more expensive (to pay for), credit card bills would get higher, new car loans would be higher, all my stocks would go lower, and I didn't have a savings account, cash or CDs so couldn't care less about higher return there.

Now? Like many of you - the exact opposite. No debt, foreign stocks, cash in 4.75% savings (about to be 5%!), no ARM, no desire to buy a home, no car loan. And a big desire to have the dollar strong (living in Europe and all).

And one heck of a strong desire to get this bubble deflated sooner rather than later.

So to the moon Mr. Ben! 5%! 6%! 7%! 8%! go go go!!!

OK, I'm a sick mutha f*cka. But I guarantee I'm not alone on this one, eh?

March 27, 2006

This Hispanic thing is starting to feel like a dormant computer virus timed to go off at a certain time and date

Where did this come from? And it seems to be spreading nation-wide. Parisians will get jealous if they don't knock it off!

Boy, add this to HP's list of troubles befalling America. Didn't even see this one coming. Anyone else feel like we're on a slippery slope getting more slippery every day? Just waiting for the next plague?

And YES, HELL YES this is connected to the housing bubble. The housing bubble actually was the #1 cause of illegal immigration during the past five years. Who the hell do you think built all those damn houses, and now who do you think is gonna be most pissed when their jobs go away? You got it.

(Oh, sorry, photos not working in blogger today... I'll put up something funny tomorrow!)

From C&L: "We have been sitting in class for the last hour and a half in full lockdown. I was able to go to the restroom and heard the thousands of marching teens from LA High converging on Hollywood and Highland. The din was unbelievable! The walkouts are spreading throughout all of Los Angeles, including the valley. We are fine here, but this is expected to go on for several more days. It is all unorganized, impromptu and is getting a life of it's own. Absolutely amazing!

From CNN: LOS ANGELES, California (AP) -- Tens of thousands of students walked out of school in California and other states Monday, waving flags and chanting slogans in a second week of protests against legislation to crack down on illegal immigrants.

The dot-condo crash is here...

Ah, we all saw this coming. People live in homes. Homes are tough to sell. But condos? Easy to get rid of.

The easy money of condo flipping is over. Many people didn't buy condos to live in - just to flip. And it's easier to sell the home you don't live in (2nd homes, investment condos) than the one you hang your hat in.

These units shot straight up to the moon. Now they are re-entering the atmosphere of reality, and buring up on re-entry.

We'll see some amazing $ and % drops over the next 24 - 36 months. Pennies on the dollar.

After several years of gung-ho development in south Florida, San Diego, Las Vegas and other major markets, the once-hot condo market is headed for a slump.

There hasn’t been a condo boom like this one, economists say, since the late 1980s when rising home prices and out-of-sight interest rates spurred developers to begin churning out a flood of condominiums. Many of these properties wound up back on the market, pushing prices down further.

Economists are concerned that this same pattern is repeating itself in markets such as Las Vegas, San Diego and Miami, where investors, rather than residents have bought many of the units.

The national median price for existing condos rang in at $228,200 in the fourth quarter of 2005 -- a healthy 12.3% increase from a year ago, according to the National Association of Realtors. But in some of the most robust markets, where prices had soared in the past few years, appreciation slowed to a trickle

Agents and economists say they expect to see further erosion this year, as the housing market continues to cool. "There is reason to be concerned about the condo market right now," said Susan Wachter, professor of real estate and finance at the University of Pennsylvania's Wharton School. "There is an all-time high of inventory right now and it is disproportional to condo markets," she said.

There hasn’t been a condo boom like this one, economists say, since the late 1980s when rising home prices and out-of-sight interest rates spurred developers to begin churning out a flood of condominiums. Many of these properties wound up back on the market, pushing prices down further.

Economists are concerned that this same pattern is repeating itself in markets such as Las Vegas, San Diego and Miami, where investors, rather than residents have bought many of the units.

HP salutes Don Knotts: 1924 - 2006

An HP'er on the Immigration protest thread reminded us of a very important point:

An HP'er on the Immigration protest thread reminded us of a very important point:

"Jesus, Don Knotts died last week and you guys are talking about THIS garbage! "- HP'er Anon

Yes folks, there are things more important than the implosion of the housing bubble, the meltdown of the US financial system, and the corruption of our elected officials.

Don Knotts died.

A moment of silence for this TV and film pioneer. And this immortal Barney Fife gem - might be of use to Bob Toll one day:

"Boys, when that steel door slams shut, that's the end of the happy days. No more fishin', no more ball playin', no more peanut butter sandwiches" - B. Fife, as played by D. Knotts, circa 1960

The Fed is going to raise rates (again) tomorrow. Home sales and prices will continue to plunge. A Blame the Fed movement starts?

Here in the UK, there seems to be this incredible pressure on the central bank to take rates down, as housing prices have been declining to flat for a couple of years.

Those on the Ponzi Scheme, oops, I mean Housing Ladder, are irate that they're not getting appreciation anymore, and blame it squarely on the Bank of England. I'm waiting for the protests in the street demanding lower rates. And the BoE feels the pressure, expected to drop the key rate 1/4 point coming up, after doing the same last year.

So, the same fate in the US? Won't homeowners who see declining prices and declining paper net worth rebel against the rookie Bernanke, and the Fed? Won't they demand a halt to the raising of rates? This is especially interesting given Fed governor Kohn's remarks the other day about not being interested in protecting homeowners' gains these past few years.

I think Ben doesn't stop here, and 5.5% is a no-brainer. Any guesses?

NAR book cookin? Did you know the corrupt and/or incompetent David Lereah is responsible for these numbers?

That February NAR report of +5.2% in sales sure looks suspect against the new home sales -10.5% number reported by the Commerce Department or the same month. So dig into the NAR number and methodology a bit more, HP'ers, and report back.

Why we would trust the NAR with ANYTHING at this point is beside me. Given all they have to lose, I don't think their reporting should be given much credence or attention.

Here's some verbiage from the NAR methodology page

The methodology in calculating existing-home sales statistics is really quite simple. The monthly EHS economic indicator is based on a representative sample of 160 Boards/MLSs. The home sales data (raw data) is divided into the four census regions: Northeast, South, Midwest and West. The raw sales volume from the participating Boards/MLSs is carefully evaluated by NAR economists to ensure accuracy. Some of the possible problems with the data could be caused by:

Changes in association/board/MLS physical jurisdiction

Changes in MLS vendors and /or staff

Lack of response by associations/boards

Erroneous data

Once the “problematic data” have been extricated from the sample, the aggregated raw volume figures are weighted to accurately represent sales activity for each region of the country. This is also called the non-seasonally-adjusted volume. The weights are benchmarked every 10 years to reflect shifts in regional demand (For more information on NAR’s weighting system refer to rebechmarking procedures at NAR.realtor.com/research). The non-seasonally adjusted volume is then converted into seasonally-adjusted annualized rates. (See section on Seasonal Adjustments)

March 26, 2006

The finest government money can buy - the NAR knows how to pick a winner (woof, woof, woof)

For all you Democrats and Republicans out there, just know that your leaders are bought, purchased and delivered by the NAR among others.

For all you Democrats and Republicans out there, just know that your leaders are bought, purchased and delivered by the NAR among others.

Keep supporting this corrupt system. Keep up your partisan, mean, course way of living. And your corrupt leaders will keep taking you for the suckers you are.

We deserve better. Until we get it, until people demand better, we're screwed.

The NAR, which says it donated $4.2 million in hard money directly to candidates and committees, had an overall success rate of 96 percent. And the National Association of Home Builders, which handed over $2.1 million in campaign contributions, did equally as well.

Money "gets you in the playoffs," an NAR spokesman remarked.

In the Senate, NAR, the nation's largest trade association with some 840,000 members, was active in 31 races and picked 29 winners. In the House, 405 of the 422 candidates it favored carried the day.

The builders' group scorecard reads almost the same. It won in 25 of the 28 Senate races in which it bet money, and it picked 323 out of 334 winners in the House.

Cashed in your house and renting. Have job mobility. Now where should you wait it out?

It's called geo-arbitrage - where you cash out of your overpriced home in your overpriced town, leave behind your over-hectic, over-consumption lifestyle, leave for the beautiful countryside of America (or beyond) and simplify.

So, where to go?

Take a look at the book above - The Best Small Towns in America, and also Life 2.0.

With the internet and wireless phones, many of us (who are early retirees, consultants, or small business owners, or have skills desired everywhere like accounting etc) can live where we want, as long as we have broadband!

Europe's great, but so flipping expensive and only going to get worse with the dollar's collapse. Iowa, Nebraska, Idaho - sound lovely, but probably too boring.

Colorado? Too expensive.

Looking for some great ideas. Outside the USA is fine too (especially these days).

Have at it.

Merced, California: The Land of the Open House - "Where did everyone go?"

Classic. This is what it looks like when the Ponzi scheme is over and the suckers are holding the (worthless) bags, wondering where everyone went... There's a sucker born every minute, but we've run out of suckers...

MERCED, Calif. — Where did everyone go?

Merced, once the state's hottest housing market, is headed back to being, well, Merced again.

Real estate agent Mark R. Gregory is holding an open house to sell a nearly new three-bedroom on a corner lot, and it's as if the Earth had been emptied.Last year, this Central Valley city enjoyed the state's hottest real estate market. Sure, things have slowed since then, but Gregory possesses a salesman's indestructible optimism.

He put a sign on the lawn, a note on the Internet, an ad in the paper. He's hoping for investors from the coast marveling at how much house you can buy here for $359,000. Or local couples looking to move up into something nicer. Or Bay Area workers willing to make the long commute.

Three hours quietly pass. At 4 p.m., the agent pulls up the sign and locks the door. Total visitors: zero."It's like everyone got together and said, 'Let's not buy for a while,' " Gregory says.

The good times have already ended here, in the same way slamming into a wall reduces your speed. A house will fetch 20% less today than it did last summer, brokers say, assuming it finds a buyer at all. Just a little while ago, Merced was an investor's dream.

The Office of Federal Housing Enterprise Oversight reported this month that prices in the city and surrounding area increased 31% in 2005. The housing agency ranked Merced first in price appreciation in California and ninth in the nation

San Diego: $100,000 off sales, 32% cancel rate, 7 month supply, median price down $71,000, not "horrible territory" yet. Yet.

If this isn't "Horrible Territory" I wonder what is? 'Cause that's reallllly gonna be bad..

In San Diego County, the median price for newly built homes in February was $468,500, reported DataQuick Information Systems. In December, the median for newly built homes in the county set a record of $539,500.

As for potential buyer traffic visiting local housing tracts, the numbers were down 23.5 percent to 15,487, according to Hanley's report for the week ended Feb. 26. There were 99 sales cancellations that week out of 306 transactions, a 32.4 percent rate. The normal rate is about 20 percent.

“I don't see it being in horrible territory,” she said. “It's something I'm watching. Any builder should.”

To combat the market's apparent lethargy, owners have cut prices and builders have begun offering extra upgrades and financing incentives.

Centex Homes reduced prices late last year by 20 percent – $100,000 off the $500,000 models – at its 65-unit Element project in downtown San Diego at 15th and Market streets.

Well, at least the Mexicans in Phoenix have plenty of homes to choose from... Inventory up 50% this year, will hit 40,000 this week

Good god these Phoenix numbers continue to astound... I wonder if a market in the history of the US has ever seen such a rapid rise in inventory? Perhaps Love Canal, or maybe Three Mile Island...

1/2: 26,715

1/10: 28,790

1/20: 31,457

1/30: 32,545

2/20: 35,455

2/28: 36,176

3/10: 37,680

3/20: 38,968

3/23: 39,043

3/24: 39,271

Waaaaayyy more illegal Mexican immigrants here than we thought? 500,000 protest immigrant legislation

Uh, what the heck is going on back there? Talk about backfiring - these protests are going to finally wake up America to the problem it's politicians have refused to address.

Good god folks, 500,000 of 'em in LA alone? I'm starting to think that 8 Million number the government quotes is probably short by another 20 million or so? Well, I'll give them a break, as it's hard to count illegals - especially when you don't want anyone to know.

But alas, the bursting of the bubble. That's gonna cause a bit of trouble with this little angry beehive we now have on our shores. You think they're pissed now, wait until their jobs are all gone. Roofers? Dry Wallers? Foundation Pourers? Remodelers? Fence Builders? Goodbye. Not needed anymore.

Now will they go back home (probably not) or will they stay in the US and find money any way they can? (yup, you got it - see last week's posting on the crime rate about to soar)

Call me racist, that's the easy thing people do for anyone who brings this subject up or calls it like it is. But folks, we're (or used to be) a nation of laws. And millions of illegals from Mexico have broken our laws, yet our government has looked the other way, so that we could outsource our manual labor for cheap prices, businesses make more money (Republicans love) and the Hispanic vote turns out (Democrats love).

My solution? You got it, get tough. Immigration raids (hell, golden opportunity missed at that rally - should've cordoned them off and asked for papers right there). Send them home now. $100,000 fine for any business who hires an illegal, per instance. No US citizenship granted for anyone born to an illegal. And then encourage LEGAL, documented and orderly immigration from Mexico. Want to come here? Then get your documentation, pay our taxes, and enjoy. Until then, stay out or go home.

Los Angeles -- In a mobilization that far exceeded the expectations of organizers, hundreds of thousands of people rallied in downtown Los Angeles on Saturday to protest legislation in Congress that would tighten enforcement against undocumented immigrants and erect more walls along the southern border.

The Los Angeles Police Department said an estimated 500,000 people joined the peaceful demonstration, which culminated at City Hall just before noon. Organizers said they believe more than 1 million participated, showing the measure of opposition to legislation that would toughen criminal laws against illegal immigrants and the people who employ them.

March 25, 2006

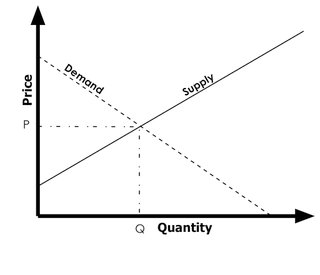

Posting for NAR Economist David Lereah on supply and demand (he obviously missed this class)

We're in an oversupply stage now, as demand quickly contracts, and prices haven't fallen (enough) as homeowners and developers remain stubborn - hoping against hope to find an ignorant buyer at an unjustified price. In addition, builders are pumping out homes into the oversupply situation, at exactly the wrong time - they're not needed.

We're in an oversupply stage now, as demand quickly contracts, and prices haven't fallen (enough) as homeowners and developers remain stubborn - hoping against hope to find an ignorant buyer at an unjustified price. In addition, builders are pumping out homes into the oversupply situation, at exactly the wrong time - they're not needed.

So guess what, David Lereah? You got it big guy - prices will contract, and new supply will either contract, or prices will subside even faster.

Supply and Demand: Effects of being away from the equilibrium point

Now assume that individual firms have the ability to alter the quantities supplied and the price they are willing to accept, and consumers have the ability to alter the quantities that they demand and the amount they are willing to pay. Businesses and consumers will respond by adjusting their price (and quantity) levels and this will eventually restore the quantity and the price to the equilibrium.

In the case of too high a price and oversupply (seen in the diagram at the left), the profit-maximizing businesses will soon have too much excess inventory, so they will lower prices (from P1 to P) to reduce this. Quantity supplied will be reduced from Qs to Q and the oversupply will be eliminated.

Leverage, Liquidated Wealth and False Income: FDIC Housing Risks Detailed

From their 3/23 Banking Issues / Recession Risks report. One thing you'll note in all historic bubbles is the use of leverage. With this Worldwide Housing Ponzi Scheme, humanity figured out a way to take leverage to a whole new level, and by a massive percentage of society, not just a small group of speculators, but the majority of the population.

Does anyone realize that maybe 10,000 people in the world probably read this report? I assume this is basic stuff to a lot of people, but in the end, consider yourself among the uber-informed. Now what will you do with the knowledge?

The risk of a housing slowdown is another area of concern going forward. The recent housing boom has been unprecedented in modern U.S. history.

It has been suggested by many analysts that the housing boom has been a significant contributor to gains in consumer spending in recent years. Indeed, a number of the FDIC roundtable panelists pointed to the apparent connection between rising real estate wealth during the past four years and the sustained strength in consumer spending during that period.

Because consumer spending accounts for over two-thirds of U.S. economic activity, any shock to consumer spending, such as that which might be caused by a housing slowdown, is a concern to overall economic growth.

It is estimated that anywhere from $444 billion to $600 billion was liquidated from housing wealth during 2005. Whichever estimate one uses, the total almost surely eclipses the $375 billion gain in after-tax income for the year.

In addition, the degree of effective leverage in home-purchase loans has risen in recent years with the advent of so-called “piggy-back” mortgage structures that substitute a second-lien mortgage for some or all of the traditional down payment.

The NAR is responsible the existing home sales report. The Fed is responsible for the inflation report... Are we really this dumb and gullible?

Main Entry: gull·ibleVariant(s): also gull·able /'g&-l&-b&l/Function: adjectiveDate: 1818: easily duped or cheated

Isn't this like Katherine Harris being responsible for the Florida vote?

Bottom line, it's all lies folks. The ones cooking the books aren't the ones who should be responsible for reading us the books

The NAR number on Thursday is looking reallllllllyyyy suspect given Friday's horrific new home numbers. And the Fed benign inflation numbers are realllllllyyyyy suspect given your pocketbook, eh?

"Statistical Corruption"

Thornburg, echoing Pimco bond guru William Gross, believes one reason the official inflation number is held down is a statistical corruption in putting the CPI together called "hedonic adjustments." Say a new computer with extra power and memory costs $100 more than last year's model. That computer nevertheless might, for CPI purposes, show a price decline, since the add-on goodies supposedly are worth much more than the retail increase.

Nonsense, Thornburg says: "It still just does what a computer is supposed to, and if you're paying more for it, that's inflation."

Equally bogus, says Thornburg, is the notion of excluding food and energy prices from the so-called core CPI, the one everyone looks at. "Yeah, they're volatile, but so what?" Thornburg says of energy and food. "People need to drive to work, and they need to eat."

Thornburg also finds that housing costs, which make up 22% of the CPI, are undercounted in the index. They are based on how much a homeowner supposedly would pay to rent his house if he were a tenant. While U.S. home prices surged 13% in 2004, the CPI housing component went up just 2.4%.

March 24, 2006

FLASH: New home sales fall 10.5%, median price falls 4th straight month, inventory swells, sales fall 30% in West

Good god, this is what a housingpanic looks like!

Run for the hills! We've got ourselves an absolute Bob Toll Meltdown! How's that builder upgrade looking now Merill Lynch? How's that healthy market and 10% price increase for 2006 looking now NAR?

Sales in February drop more than expected, as median price falls and supply grows. Is the real estate bubble bursting?

New home sales fell more sharply than expected in February -- and along with them, the price of a new house -- in the latest signs of a slowdown in what had been a white-hot housing market.

Sales sank 10.5 percent to an annual rate of 1.08 million homes in February, from the revised rate of 1.21 million in January, the Census Bureau reported.

Robert Brusca of FAO Economics said it's not too soon to wonder if there has been a bursting of the so-called "housing bubble" of recent years, when prices and sales kept rising.

"How can you look at these data and ignore the question?" he asked rhetorically. "We had such a dramatic fall in the West," he added, where sales fell almost 30 percent.

"If there's a bubblicious market, that's the one, the one that had the highest prices. And while you can say all housing markets are local, but it's clear there have been factors that helped all the different markets, so it would be folly to say that couldn't reverse."

Forbes: The Last Speculators. The perfect article illuminating the Housing Ponzi scheme

Important article, so here's the whole thing. Take the time to read it. Everything we've talked and joked about:

Important article, so here's the whole thing. Take the time to read it. Everything we've talked and joked about:

Strip club managers becoming flippers, Miami being ground zero, and this massive game of musical chairs ending, yet some didn't hear the music stop

Condo flippers in south Florida will tell you that they are sure, real sure, that they will sell out at a profit.

Robert Jenkins, 30, found religion, quit his job as a disc jockey at a strip club and, in 2003, began speculating on real estate in hot-hot south Florida. He borrowed heavily and flipped 19 houses in Fort Lauderdale, reaping profits of $750 to $71,000 on each property and plowing two-thirds of his $300,000 in profits into still more homes. He now owns seven, worth $2.5 million and doubts a crash will happen. He vows to keep flipping, even if it does.

Donna Franklin, a 52-year-old former direct-mail publisher, owns five homes. Last year she and a partner borrowed against a Miami apartment they own and rent out to make down payments on three $400,000-plus “preconstruction” condos in Fort Lauderdale. They are confident they can flip the three condos at a nice markup soon--well before construction ends, at which point they must take mortgages for the $1 million they owe developers.

That could be wishful thinking. The number of unsold condos for sale in and near Miami has more than doubled from a year ago to 2,232, says Miami Realtor David Dweck. Foreclosures nationally are up 45% in a year and in Miami now occur at twice the national rate of one per 1,117 homes, according to RealtyTrac. Some 25,000 condos are under construction in the Miami-Dade area--more than the total number of purchases in the last nine years combined.

Three-fourths of those are in the hands of speculators, says Jack F. McCabe, a Deerfield Beach, Fla. consultant to developers. “The demand is artificial. Most south Florida speculators have been selling to other speculators,” he says. “It works fine--until you’re the greater fool and nobody else comes along to pay that higher price.”

Neither Jenkins nor Franklin paid much attention when the Commerce Department, on Feb. 27, said the supply of unsold, newly constructed homes across the country had ballooned to 528,000 in January, up 60% from the average from 1995 to 2004.

Brisk sales of new homes have helped prices stay aloft, for now; sales are running at 1.2 million houses a year, 40% more than normal. But if rising mortgage rates cause sales to tumble to a normal pace, the effect on prices would be shattering. And in some parts of the country the last speculators--people like Jenkins and Franklin--would be in deep quicksand.

A correction may already be under way. The number of half-million-dollar-plus condos up for sale in Miami is twice the number in Los Angeles, whose population is four times as large. In New York prices reportedly slipped 13% last summer. In Las Vegas several developers have canceled projects amid soaring construction costs, spurring suits.

Condo prices in Florida have gone up 63% since 2002, and most speculators credit the state’s population growth--a thousand newcomers per day. Others credit the speculators themselves: Encino, Calif. real estate firm Marcus & Millichap says more than half the mortgages in Florida are high-spec in nature. The firm compared price appreciation to income growth in markets across the U.S. and fingered West Palm Beach, Fort Lauderdale and Miami as three of the five most vulnerable to a price correction.

Terrance and Jennifer Trott, both 26, describe themselves as “regular folks” who happen to own two homes. They grew up in New York’s Hudson River Valley and moved to Florida after Terrance finished active service in the U.S. Marine Corps in 2004. Last July they borrowed on their four-bedroom house near Tampa to pay $200,000 for a two-story condo in a development near downtown Tampa. They listed it at $235,000 in December. Two months later they dropped the price to $217,000 and are getting some bites.

The Trotts together earn about $85,000 a year, and the extra $22,000 a year it costs to carry their condo is a severe drain. “I drive a Kia that I’ve had since 1999 and it’s paid off, and we only go out to eat on the weekends, and it’s not every weekend,” Terrance Trott says. If the condo doesn’t sell, they may try to rent it out--just like everyone else; but even at $1,000 a month they would be pouring cash into the property.

In the aftermath of every crash come a few fearless souls, intent on making money on the misery of others. Jack McCabe, the Miami consultant, is raising a $250 million vulture fund to buy condos. He aims to pick up $1 billion of south Florida apartments on the cheap. Lenders are already offering him blocks of condos repossessed from distressed homeowners. “We’ll focus on buying million-dollar properties at 2003 prices-- at 70 cents on the dollar,” he says.

March 23, 2006 - The Fed's M3 Money Supply report dies. And nobody cares?

I sure wish Americans would put down the remote control and care about something. Anything. And one thing they (and the world) should care about seems so trivial, but actually is so important.

Yet nobody, no major media of any type, issued an article or report today (google news it - nothing at all).

The Fed as of today is free to oil up the printing presses and print as many dollars as they would like. And you know they will, and you know they have to. M3 is dead. Read this to understand the reporting if it's been awhile since Econ 101. Why did they, after all these years, suddenly stop issuing M3? Because they have to, because they can, and because they thought they could get away with it.

So, with the dollar about to start its long march to worthlessness, today is Day 1, Year 1. And away we go. Your savings, your wealth, your benefits, our deficit, our debt, our ability to pay our debt, bonds, stocks, our trade imbalance, your everyday low prices at Wal-Mart, and your home's value - all are impacted by this.

Discontinuance of M3

On March 23, 2006, the Board of Governors of the Federal Reserve System will cease publication of the M3 monetary aggregate. The Board will also cease publishing the following components: large-denomination time deposits, repurchase agreements (RPs), and Eurodollars. The Board will continue to publish institutional money market mutual funds as a memorandum item in this release.

Measures of large-denomination time deposits will continue to be published by the Board in the Flow of Funds Accounts (Z.1 release) on a quarterly basis and in the H.8 release on a weekly basis (for commercial banks).

M3 does not appear to convey any additional information about economic activity that is not already embodied in M2 and has not played a role in the monetary policy process for many years. Consequently, the Board judged that the costs of collecting the underlying data and publishing M3 outweigh the benefits.

March 23, 2006

I know this blog is about the housing bubble, but I have to post on Abdul Rahman

It's 2006. We've been at this human race thing for more than a few thousand years.

And we still live in a world where we get this.

Solution? We need to destroy the Islamist movement, and anyone associated with it. This doesn't mean Islam, it doesn't mean Iraq. It means the Islamist cult and their members.

And to think we created this government. Not one penny more, not one more troop, should go there until they get this fixed. And if they kill this guy, we should go in and level the place with vengeance, to ensure their gene pool never breeds again.

Write your Senators folks. Do what you can on this one. Demand outrage.

Now back to the housing bubble.

Ah, you have to love that classic moment in any Ponzi or Pyramid scheme, when the music stops...

And the bag holders look around and say "hey, what happened! We were all supposed to get rich! Come on back! Don't let me stay holding this damn bag!"

And the bag holders look around and say "hey, what happened! We were all supposed to get rich! Come on back! Don't let me stay holding this damn bag!"

That moment is here, and Tucson Arizona is holding a really, really, really big worthless bag of cowtown sh*t, with nobody to buy it from them...

"Tucson real estate has risen much faster than household income growth," Stiff said. "As a consequence, we predict a significant slowdown in home appreciation in Tucson."

Stiff said California real estate speculators fueled much of the growth in property values in Tucson, Phoenix, Las Vegas and other Southwestern markets over the past couple of years.

A wave of speculation that has radiated eastward from California is responsible for the unprecedented price jumps," he said. "Mortgage payments are already above what many people can afford, which has to eventually put the brakes on the market."

Anyone want to buy a home for 200% more than it's worth? Great! One's available in West Phoenix.

Anyone been to the West side of Phoenix? Generally an awful area. And location, location, location. Here's a sucker who must've bought a home to flip during the ponzi scheme and lo and behold, the music stopped. A few years ago, $230k would've got you the mansion (the only one) in West Phoenix. Now? 1,300 sq. ft.

Anyone been to the West side of Phoenix? Generally an awful area. And location, location, location. Here's a sucker who must've bought a home to flip during the ponzi scheme and lo and behold, the music stopped. A few years ago, $230k would've got you the mansion (the only one) in West Phoenix. Now? 1,300 sq. ft.

I'd make an offer of $65,000. Tops. Probably could rent it out for $600 a month. Seriously, you couldn't pay me to live there. Not $5000 a month.

$230 - Buy My Investment Rental Home

Reply to: weshawk1@hotmail.com

Date: 2006-03-23, 9:19AM MST

I am looking to sell my rental property. It is a very nice newer (2002) 1300 sq ft single family home in a very quiet neighborhood. The home comes with very reliable tenants who have lived there for 3.5 years. Unfortunately I am in desperate need to sell, and will transfer the property for what I owe on it. No realtors, no hidden fees... Comparable homes are selling for $235k-$255k, so you will be walking in with a bit of equity on a turn key investment.

No insurance? No worries! Big daddy government is here to bail you out

Do you realize Katrina homeowners can get up to $150,000 of your tax dollars for their house? Guess there's no need for insurance these days when the mother of all gift horses is in the corral

Does that also mean big daddy government will bail out bubble homeowners who get foreclosed on? After all, they were just following government's advice - get a home and get an ARM.

Is anyone else incensed with how the government is spending like drunk sailors these days?

Gov. Kathleen Blanco's administration outlined a $7.5 billion rebuilding, relocation and buyout plan for Louisiana residents with hurricane-damaged homes - the first comprehensive plan the state has offered for thousands whose homes remain ruined in neighborhoods paralyzed with uncertainty.

Homeowner assistance would be capped at a maximum $150,000 per homeowner under the draft recommendations unveiled Monday

Overvalued.blogspot points out this San Mateo gem. Guess how much?

I grew up in a small town in Michigan, where $50,000 was a really nice house, $100,000 was a near mansion.

So I'll always be shocked to see a dump like this house going for what it's going for today. It would've been worth about $10,000 from my 1980's Michigan memory, and the people living in would be unemployed, uneducated and unwashed...

Plus, should anyone have to pay $5000 a month plus to live in such a hellhole?

Yup, this gem is listed at $725,000

When does the madness end?

2008. Someone's gonna have a mess on their hands.

Why, I ask, would ANYONE want to be president in 2008? Think of the unbelievable mess they're going to have on their hands:

Why, I ask, would ANYONE want to be president in 2008? Think of the unbelievable mess they're going to have on their hands:

1) The housing bubble will have popped, big time, and the Housing ATM is out of order, devastating the economy, with millions unemployed as a result

2) Iran, Iraq, N. Korea, Syria, etc

3) We will have lost our manufacturing base, with millions more unemployed, as China continues its rise, WalMart wreaks havoc, and jobs pay less and less

4) Incredible annual deficits, a soaring national debt, state government bubble built tax bases declining with the declining bubble, and no end in sight to the red ink

5) A declining dollar, high interest rates, high inflation, negative GDP

6) More baby boomers retiring, with no solution to medicare, medicaid or social security enacted by Bush/Congress

7) A negative national mood

8) Bird flu

9) Partisanship, the religionization of government and partisan media turning American against American in a nasty, caustic society

10) A lousy $165,000 a year salary, 14 hour days, 7 days a week

Why then, does Hillary want it so bad? Perhaps she doesn't, and we're all wrong about her. We'll see.

By the way, I like Evan Bayh on the Dem side to win, and George Allen, Mr. Evil, on the Republican side.

McCain can't get through the Republican primaries, Rudy will flame out with skeletons, Frist is a joke, Newt will overachieve, Feingold is too lib, Biden will lie again, Mitt is a Mormon, Mark Warner will bore us, Gore will rise fast then peter out, Kerry will get no support, Draft Condi will fail, Colin again won't run, Harold Ford and Barack will consider, then say no, and a businessman will run as an independent getting 10%.

For fun, I'd like to see someone young (35 - 45) get in the race to start the intergenerational war. Barack, Harold, JD? I'd also like to see a celebrity, or media star, consider it. Trump? O'Reilley? Stern? Franken? Hannity? Brokaw? Someone's gonna surprise us.

But again, I think they're doomed to failure. No money to spend, tough decisions to make, no fun.

It's no fun to clean up after a party. But hopefully a hero will emerge, who'll do the right things for America, regardless of party and politics. An FDR, a Lincoln. Or we just get another Bush or Clinton and go down the crapper.

ABC News video: Homeowners who can no longer afford their homes (thank you ARMs)

Click the link - this is an excellent, excellent report. Too bad the media didn't report this stuff when it was happening - or when Greenspan was recommending folks get an ARM and Bush was recommending everyone buy a house.

It's too late now. People are in too deep. Foreclosures will soar (and are soaring). Lives are being ruined.

Yes, nobody made these folks buy a house. Noboday made them sign a no-down, interest only teaser rate loan. Nobody made them buy a wildly overpriced bubble home. They made their beds, now they don't get to sleep in 'em.

hat-tip to bpl for the link. Oh, Sam D. doesn't do the report - I just liked the picture.

March 22, 2006

boom, bust, boom, bust, boom, bust, boom, ...

3p

We are such optimists, we Americans - it's how we got to where we are. Yet we have such short memories. When times are good, unemployment is low, tax receipts are up, housing values are through the roof, business profits are pouring in, we assume there'll never be another recession again in the history of the United States.

Then, it happens.

What will this next recession look like? Will it be worse than most others, or even the last? When will it start, and when will it end?

From a fellow blogger, Thomas Palley:

After having been wrong once, it’s either brave or foolish to make a second prediction that the next recession will be deep and difficult to escape. But the facts point to it being just that—despite the optimism of the Federal Reserve. This is because the economic factors that helped escape the last recession have been largely exhausted, and will not be available to fight the next recession.

Homeowners have already significantly refinanced so that the stock of high interest rate mortgages available for refinancing has been depleted. Consumers are borrowed to the hilt, leaving less access for further borrowing. House prices are already at all-time highs by every measure—so lower interest rates are unlikely to spur another price boom, with all its expansionary effects. Instead, house prices could actually start falling as new supply continues to come on to the market, and this effect could be amplified by recession-induced job losses that trigger mortgage defaults by workers losing their jobs. Taken together, these factors point to future interest rate reductions likely being akin to pushing on a string.

Will Housingbubble2, patrick.net and housingpanic be blamed in part for popping the bubble

In other words, once America wakes up, notices 12 straight months of sales declines, exploding inventory, and falling prices, will they actually take out some of their anger (for their declining "wealth") on the housing bubble blogs?

Here's Patrick's take:

It is also the power that opens up this community to criticism. This past week we saw Patrick.net blogged about in other forums as being “irresponsible media”. Although this was a small, more or less isolated event, it likely foreshadows events to come as the housing bubble correction enters the mass public consciousness.

Without sounding alarmist, we should probably begin to thicken our collective skins, at least just a bit, as those who stand to lose the most from the correction begin to lash out at communities like ours.

Any HPers in the UK see the BBC undercover report last night on corrupt estate agents?

The best piece of television journalism I've ever seen. Ever.

The best piece of television journalism I've ever seen. Ever.

I couldn't believe what I was seeing with the BBC reporter's hidden camera - forged contracts, forged passports, fake bids, non-stop lies, fake buyers, made up stories, you name it - anything to do the deal, make your numbers and get that commission.

Especially the omni-present Foxton's - the boiler room operation of the UK real estate bubble. Anyone who watched this report won't ever think of using Foxton's ever again. They're toast. What a slimy, unethical, pathetic collection of human scum, led my other human scum.

One word - disintermediation.

Folks in the US (and elsewhere) - click on this post's link and watch the recap video. You just know crap like this happens (or worse) every day in the states.

The lure of the almighty dollar (or pound) and people's morals and ethics go right out the window. People should go to jail. And so they will, once someone starts investigating this sleazy business called real estate.

Housing bubble burst effect #4531: DIY home improvement stores will get slaughtered

It's already happened here in the UK with B&Q (they're the Home Depot of the UK) - with results.

When your bubble bursts, no more contractors stocking up on supplies. No more DIY'ers buying equipement to refurb for a quick flip. No more no more.

Stores will close. People will get layed off. Items will be discontinued. And their stocks will plummet.

Take it to the bank, Banker.

Kingfisher paints dismal picture of B&Q's prospects

Analysts warned forecasts for this year looked vulnerable after the group said the home improvement market had deteriorated since the start of the year.

Gerry Murphy, the chief executive, said a "dramatic downturn" in the UK do-it-yourself market, which was the weakest in 10 years, was behind the collapse in profits at B&Q.

In the 12 months to 28 January, retail profit at B&Q fell 52 per cent to £208.5m.

Analysts at CSFB, the company's broker, said: "We believe the UK business has not yet bottomed out and talk of a recovery is very premature."

Blacks and Immigrants to get hardest by real estate bust due to percent of income paid towards housing

Right after the post yesterday on my prediction of an increase in the crime rate, addressing the socio-economic issues of our black, white and Hispanic classes with the housing meltdown, this report from Boston.

Right after the post yesterday on my prediction of an increase in the crime rate, addressing the socio-economic issues of our black, white and Hispanic classes with the housing meltdown, this report from Boston.

Economics folks are destiny. Not genetics. Not skin color. Simple personal economics.

And when you heard Bush, among others of course, pumping home ownership as the American Dream a year ago with the "ownership society", thus encouraging the houseless to get housed (or hosed), it was the last sucker in, and unfortunately, cruely, that was disproportionately the lowest socioeconomic rung - made up disproportionately of minorities.

The rich white guy telling the poor Blacks and Hispanics to buy at the top. Maybe Kanye West had a point there..

Homeowners stretched perilously - More than a quarter in Boston spend at least half their pay on housing. Blacks are hit hard.

If the nation's real estate boom collapses, its first victims may well be low-income minorities and immigrants in a big US city like Boston.

That is the picture emerging here as foreclosures rise and the housing prices falter. More than one-quarter of Boston's mortgage-holders appear to be stretched thin financially, spending at least half their income on housing, according to an analysis of census figures. That's more than twice the national average and the highest of any major city except Miami.

The trend is especially worrisome, the analysis shows, because these vulnerable homeowners tend to be minorities and immigrants who, experts say, often hold the riskiest mortgage loans.

The threat has implications not only for Boston, whose population would have shrunk without an influx of immigrants, but for the US.

The pressure appears greatest for minorities and immigrants, says Dr. Sum, who conducted the census analysis. Statewide, 33 percent of blacks with mortgages were paying half or more of their gross income toward monthly housing costs, and 29 percent of Hispanics were, more than double the average, he says. And 22 percent of foreign-born fell into the category. Such factors could not be broken down for Boston because the census data are limited.

And they're off - pick the first bubble market to hit 1-year worth of supply glut

From bubbletracking - months of inventory tracking by bubble market. Wonder what the first market to hit 1 year of glut will be? I'm betting on good 'ol Phoenix, closing fast, but Sac Town is coming 'round the bend...

From bubbletracking - months of inventory tracking by bubble market. Wonder what the first market to hit 1 year of glut will be? I'm betting on good 'ol Phoenix, closing fast, but Sac Town is coming 'round the bend...

Riverside County

9/05: 2.1 months

2/06: 4.4 months

Las Vegas/Clark County

7/05: 3.4 months

2/06: 7.5 months

Phoenix Metro

7/05: 1.1 months

2/06: 6.6 months

Sacramento Metro

2/05: 1.9 months

2/06: 8.4 months

San Diego County

7/05: 3.0 months

2/06: 6.0 months

Orange County

7/05: 1.5 months

2/06: 3.9 months

Los Angeles County

8/05: 1.7 months

2/06: 4.6 months

Imfamous NAR economist Lereah predicts housing boom and skyrocketing prices

This hack tells 'em what they want to hear, I'll give him that. It would be tough to stand up in front of 250 realtors and tell them "housing is collapsing, the Ponzi scheme is over, and you all better look for new work quick!"

This hack tells 'em what they want to hear, I'll give him that. It would be tough to stand up in front of 250 realtors and tell them "housing is collapsing, the Ponzi scheme is over, and you all better look for new work quick!"

Funny how "Lereah" is very close to "Leach"

The chief economist for the National Association of Realtors and the head of the Federal Reserve Bank of Boston said the economy's fundamentals remain strong enough that recently flat housing prices should rise again, starting next year - although at a slower rate than in the past few years.

"The air is coming out of the balloon," said Lereah, who argues that a balloon is a better metaphor than a bubble to describe a market he characterized as going through a temporary price correction rather than a collapse.

"The bubble is not bursting. The solid fundamentals in our economy will keep the real estate expansion alive," Lereah told about 250 real estate agents at the New England Realtors Conference.

Lereah predicted that housing prices nationally will grow about 6 percent this year, compared with 12.5 percent last year.

Gee, brilliant conclusion: Fed 'could be wrong' about housing bubble

Watching these dolts think their way through the housing collapse (and their role in it) is like watching a monkey contemplate a banana. The wheels are turning, slowly, slowly...

Watching these dolts think their way through the housing collapse (and their role in it) is like watching a monkey contemplate a banana. The wheels are turning, slowly, slowly...

One of the greatest risks to the U.S. economy is a possible sharp slowdown in the housing market, said Boston Federal Reserve President Cathy Minehan.

"The resulting rising stock of unsold new homes will likely bring about a modest decline in construction, probably accompanied by a gradual flattening of house prices," Minehan said. "As construction of new homes slows and the pace of growth in housing wealth eases, economic activity will be restrained. The question is 'How much?'"

The Fed's forecast assumes a flattening of home prices and a decline in construction, leading to a slight softening in economic growth. The Fed sees economic growth of 3.5% this year.

"Clearly, however, we could be wrong on the magnitudes," she said'. "Real estate prices could actually decline."

March 21, 2006

HPers - read any good books lately? Make your recommendations here

I'd start with the one shown here - Life 2.0. I think the bubble burst will cause many folks to rethink their position in the rat race. And get out. Life's too short to spend it sitting in traffic in New Jersey on the way home to your $800,000 two-bedroom condo.

My other favorite reads are to the right from amazon.com

I also just finished for fun the Christ Clone Trilogy series by Beauseigneur.

Subscribe to:

Posts (Atom)

{kind=link}

{kind=link}

{kind=link}