Here's my take - condos are like day traded stocks in 1999.. houses are like bonds...

People actually LIVE in houses - thus they're more difficult to day-trade. Condo though are like pieces of paper - that can be bought and sold very quickly, and mass produced very quickly too, as you stack 'em on top each other vs. one per parcel of land like a house

So.. what goes up must come down, and condos will be first to fall. It happened 20 years ago in Florida, and it's happening now

Call it "condo-mania" uncontrolled condominium construction and high prices. It hit the Tampa Bay area in the early 1980s. The area is just beginning to recover from that condo glut . . . If you're shopping for a condo, the best deals are to be found in foreclosures or resales by investors.

This history lesson is from a 1987 story in the St. Petersburg Times.

I bring it up as I drive around Orlando, looking at the increasing number of "For Sale" signs in front yards, taking note of those that have had their "Price reduced."

The number of homes on the market is at an eight-year high. We are shifting from a seller's market to a buyer's market. The speed at which this is happening is remarkable, given that interest rates remain low.

November 30, 2005

Condo craze is headed for crash and burn

Check this ponzi out - borrowers doing refi in order to take cash out to pay their mortgage

Oh, man, this is trouble if it's happening on a big scale - but hey, it makes sense. You get that $700,000 condo, can't afford the payments, what are you gonna do?

I love the Another F'd Borrower blog... good anecdotal from an insider

And I'm starting to think that rushed-through new bankruptcy law is just 'cause banks and lenders know that this type of stuff is happening, and that the bills REALLY come due real soon - when property values decline more...

Here's the case:

"I need to do a refi cash-out to get money to pay my mortgage."

Yes, you heard me correctly. I am seeing more borrowers that are refinancing to get cash out so they can pay their mortgage and "stay afloat". Yes, it seems that the mathmatically challenged "buy-now pay-later" American home buyers don't seem to understand that taking out a bigger loan to pay off a smaller loan is NOT a good long term financial strategy

Classic bubble article - from 2004

I'd like to say great minds think alike, but in this case, you'll see that even back in 2004, some smart folks were already predicting what we're not seeing today - and hey, even a future great name for a blog (coincidence I swear - but great name eh?)

Bottom line - there are some classic bubble/mania books, like Manias, Panics & Crashes which I recommended last week. And there's classic bubble predictor articles like this one, or ones from 1999 about the NASDAQ.

The only problem with bubble articles and books though is predicting the exact date of the POP! Documenting the reasons, exploring the fundamentals, describing the behavior - all easy. But when does irrational exuberance peak? When does froth spill out of the cup? That's tough. I'm gonna say this housing bubble peaked the day I launched HousingPanic - around November 1, 2005

Here's a stanza from the article.. Enjoy the read.. Thanks to a HP reader for the link...

It's not just the discipline of banks that keeps people from buying more than they can afford, but also the buyers' own fear and guilt. But in an environment where home prices continue to spiral up, fear and guilt are replaced by a sense that you're a fool not to buy the most house you can possibly get away with.

A particular kind of speculative frenzy ensues, captured in a recent story in The Washington Post which detailed a new phenomenon: home buyers camping out overnight for the chance to be the first in the next morning's open house, ready to buy $700,000 houses in built-out, lush-lawned suburbs like Arlington. The phenomenon has created temporary, yuppie tent cities. The story's authors interviewed several buyers in the tented line who planned to sell their purchases back into a steadily rising market, and concluded, dryly: "There is an element of speculation to the lines."

November 29, 2005

Pop! Miami housing market collapsing as inventory explodes

I'm just amazed by these numbers from Miami... Huge increases in inventory, and the slippery slope of declining values.. even though builders are trying to hide those numbers by offering big incentives (FREE CAR!) instead of dropping price

Trend 11/28/2005 1 month 2 month 3 month

Median Price $400,000 -2.4% -3.6% -4.8%

Inventory 18,660 +13.6% +27.3% +44.9%

Historical Data

Date Inventory 25th % 50th % 75th %

11/28/2005 18,660 $282,900 $400,000 $659,000

11/21/2005 18,261 $284,900 $405,000 $662,000

11/14/2005 17,601 $284,000 $405,000 $662,000

11/07/2005 16,952 $284,900 $405,000 $660,000

11/01/2005 16,424 $285,000 $410,000 $675,000

10/28/2005 16,425 $285,000 $410,000 $675,000

10/21/2005 16,977 $285,000 $409,900 $675,000

10/14/2005 15,894 $285,000 $409,000 $674,900

10/07/2005 15,296 $287,000 $412,000 $680,000

10/01/2005 14,953 $288,000 $415,000 $685,000

09/28/2005 14,655 $289,000 $415,000 $690,000

09/21/2005 14,251 $289,000 $417,900 $695,000

09/14/2005 13,604 $289,900 $420,000 $699,000

09/07/2005 13,064 $289,000 $423,900 $701,000

09/01/2005 12,800 $289,000 $422,900 $714,000

08/28/2005 12,882 $286,990 $420,000 $709,000

08/21/2005 12,606 $289,000 $424,900 $719,000

08/14/2005 12,361 $289,000 $425,000 $700,000

Classic end of bubble scenario - tightening of credit - Banks tighten lending to build condominiums

But is it too late? I predict massive numbers of condos that were "purchased" by investors will never be bought - as investors walk away from deposits, leaving developers on the hook - and then in bankruptcy court - as the condo project gets mothballed...

Some of the nation's largest lenders are cutting back on financing and are tightening standards for condominium projects, a sign that banks, which helped to fuel the run-up in real-estate prices with cheap debt, may be growing more skeptical about the prospects for residential properties.

In recent months, lenders have been requiring developers to put more of their own money into projects, sell units faster, and prove that they have experience completing these condos. Many banks have cut back on loans in markets where there has been the most building and investors already have bought up a large number of new condominiums.

"Lenders are looking toward more worst-case scenarios," says Dwight Dunton, president of Bonaventure Realty Group LLC, a real-estate developer based in Arlington, Va.

Housing sector could become a rough neighborhood

Shorting the housing sector is the gift that keeps on giving - builders, mortgage companies, Freddie, Fannie.. enjoy

I don't know what's going to happen to home prices. Certainly, there are many factors to prop them up, including immigration and population growth. Given how many smart people have been so wrong about the future of housing prices, I don't want to even guess.

What we do know is that many of the publicly traded companies associated with the housing boom are already getting hurt. The latest example came in early November when high-end home builder Toll Brothers (TOL) stunned investors with the news that it wouldn't build as many homes in fiscal 2006 as it had earlier forecast. That day, Nov. 8, the stock dropped 14%. It has since recovered some of that loss. But that was just a blip. From its 52-week high in August, Toll Brothers stock has suffered a drop of around 40%, wiping out billions in shareholder wealth.

November 28, 2005

Financial Ruin: First of many articles on homebuyers losing their shirts before moving in - Here's one from D.C.

Can you imagine losing $100,000 on an investment in a matter of months? Financial ruin because all you did was sign your name on a purchase contract? Oh, boy, there are going to be so many of these articles - on people who bought at the top...

Lynn Edmonds and his wife, Sebnem, could barely wait to sign on the dotted line back in May when they committed themselves to pay $796,000 for a three-floor townhouse under construction in Alexandria's Cameron Station.

But since May, the sales prices for the development have fallen -- and units like the one the Edmonds bought are now being sold for $699,900. The Edmonds are facing the prospect of a $100,000 loss in value before they even walk through the front door.

"We blithely stepped into the contract, thinking it would hold its value -- but that's not the case," said Edmonds, 46, a program analyst and Air Force veteran. "I feel so stupid putting myself into it. It's real estate -- I knew on a theoretical basis that it might go up and it might go down, but now I know it on a practical level."

What realtors really mean when they say they expect housing prices to stabilize

Hat-tip to HP reader Jeff for this article today from up-state NY.

My question is, when the realtors and builders are continually having to justify prices, and tell people not to panic, why? Are they sensing prices are too high? And that panic is in the air?

We'll see more and more of these in the coming days - where realtors give their "expert opinion" and say things like "don't panic" and "we're seeing the market come back to reality" when what they're truly saying is "holy crap - we're in major trouble here" and "there are no more suckers left - the market's crashing". Lots more fun quotes in this read, including these gems...

After defying economics and reason for several years, the housing market in New York's northern suburbs is coming back to reality (translation: house prices are going to crash - the only way to get back to the mean)

"The market is in transition," said Kevin Joyce, president of Joyce Realty and a former president of the Rockland County Board of Realtors. "It is regaining some balance, and returning to more normal conditions." (translation: to get to normal, we need to crash)

However, they insist there is no reason for panic and stress the market remains healthy. The consensus is that sales and price increases have slowed, but the market is in no danger of collapse (translation: it's time to panic, the market is post-peak, the last suckers in are getting killed, and there is a 100% danger of collapse)

Unfortunately, due to interest rates, higher gas prices and projected higher home heating costs, buyers are becoming more cautious and wary. We are already seeing many price reductions across the board in all price ranges (translation: the only way to move a house now is to dramatically drop the price, cause there ain't any more buyers)

"If we have a correction or a return to more classic times, it will be a positive move for the market. It will entice buyers back to take another look," Lindsey said. (translation: a home price crash is a good thing - really!)

HousingPanic Buy Recommendation: SRPIX - ProFunds Short Real Estate Fund

So many stocks to short, so little time. But now ProFunds has wisely introduced a fund that allows you to short the US Real Estate Index (DJUSRE)

So... you can short the DJUSRE, or go long the SRPIX... Or you can short the individual plays, but I like having a basket

If you believe that the real estate index will follow the trend of the .com or NASDAQ bubbles, this is your best play.

Best of luck. Today's news will undoubtedly start the decline again

Ponzi Scheme Alert - Prices are being artificially kept high by builders increasing incentives, vs. cutting price

Maybe they're thinking we're not watching? Meanwhile, this report, balanced against today's housing numbers, is very illuminating. Explosion in unsold houses, drop in sales volume, but prices "holding steady". Yeah, right they are...

New-home builders in Greater Sacramento are offering incentives worth up to $50,000 to bolster sales in a slowing market without cutting prices.

The most dramatic deals have come within the last month, says one local housing analyst, and range from paying closing costs to offers of free cars, vacations and swimming pools

Holding the line on official prices lets builders escape resentment from recent buyers who paid the full tab. It also lets builders keep the advertised prices in place in hopes of a better market next year

FLASH: U.S. Existing Home Sales Fall More Than Expected - Unsold Homes at 20-Year High

Data starting to catch up with the realities from the street... This should freak out the housing stocks again - Toll Brothers, Pulte, Lennar, Standard Pacific, Fannie, Freddie, etc

Rising mortgage rates and skyrocketing prices put home-buying out of reach for more Americans in October, a new report showed.

Sales of previously owned U.S. homes fell a greater-than- expected 2.7 percent last month to a 7.09 million annual rate, the slowest since March, the National Association of Realtors said today in Washington. The number of unsold homes was the highest since April 1986

November 27, 2005

Mass. housing boom over, homeowners, agents say

Thanks to Boston reader Katy for this article today... I feel sorry for those poor buyers who bought at the top - they must be in such pain to read this stuff every Sunday...

Massachusetts' five-year housing boom, which lifted the average home price by 71 percent and bolstered the local economy, is over, according to homeowners and real estate agents.

Rising mortgage costs, an outgrowth of 12 consecutive interest-rate increases by the Federal Reserve since June 2004, have cooled demand, they said. Prices have dipped, and sellers are rushing into the market even as open houses attract few prospective buyers.

''It's definitely a buyer's market, and it's likely to stay that way at least through the first half of next year," said Alan Kosinski, 49, of Stoughton, an investor who has bought and sold about 800 properties over 20 years. ''People who have to move are going to be selling at a discount or a loss."

Phoenix, Arizona: New-home lull shifts the rules - Sellers, buyers see tables turn

Boy, did this market sure turn on a dime..

Next will be the horror stories of people buying $800,000 tract homes from builders who then cut the price of the same home next door in order to move it - giving the first buyer a nice $50,000 loss before they move in.

Oh, man, is Phoenix getting ugly! And for those of you who don't live here - you'd be amazed how many $800,000 2-bed condos are still going up - those developers and would-be flippers must be freaking at this point

Real estate agent Neil Brooks was a little surprised when a home builder called him to say that one of his clients was a lucky winner in a lottery used to dole out coveted lots.

Brooks, a Century 21 agent in Scottsdale, figured it was a long shot that the client's name would be pulled with so many people shopping for new homes. Many builders instituted lotteries or waiting lists when rampant demand outstripped the supply of lots they wanted to release to buyers.

But Brooks certainly wasn't expecting another call a week later from the same builder asking if he had any more customers looking for a new home. advertisement

"The builder calls and says: 'Hey, guess what? We had another lottery. . . . Do you want to bring somebody by?' People showed up and instead of snapping them up like they have been, they said, "I'll take a pass.' That freaked out the builders."

Hate Big Oil? Hate home-builders, too

The time will come when we'll see that the home builders, the realtors, Freddie, Fannie, appraisers and mortgage lenders deserve our wrath much more than the oil companies.

But not until homeowners feel the pain of lost equity. Which is soooo much more substantial than a few pennies at the pump.

Consumers are fuming over outsized oil company profits. But by the same logic, shouldn't home-builders and real-estate brokers be on the hot seat for soaring prices?

Americans outraged over the price of gasoline and the sensational profits of oil companies of late should stop a moment and look inward. Not at their souls, but at their homes -- which have appreciated in value at least as much as gasoline, and in many cases much more.

Instead of flipping condos, you could be flipping burgers -- and I don't think the Fed cares.

Good article on our favorite - the Fed.

My take is they'll keep hiking way beyond what Wall Street is thinking. Heck, look at what the New Zealand central bank is having to do to get control of their housing bubble...

Who’s afraid of the Federal Reserve?

Some experts say the fate of the economy next year will hinge on how high rates are raised

The mighty Federal Reserve. It's more powerful than a ballooning housing market, able to stop inflation in a single bound. And, if it slips, if it uses its super powers unwisely, if it goes too far, it could push the economy into recession with just a nudge of its pinkie.

That's one way of looking at the nation's central bank. Under outgoing Federal Reserve Chairman Alan Greenspan, it has become the main way. The Fed is seen as the arbiter of all things economic, the capital of Moneyland, with Greenspan as its ruler and resident hard-to-understand genius.

With the chairman's seat at the central bank expected to turn over to Ben Bernanke in January, it's time for a reality check. Just how powerful is the Fed?

Phoenix, we have a problem - check out meltdown going on in Arizona

Check out the

A) Rapidly increasing inventory the past 12 weeks as investors (flippers) rush their properties to market in a desperate attempt to get out

B) Rapidly decreasing median asking prices in all pricing percentiles - note the 50% percential is the median price for the market

C) Note the lower bracket is holding better than the others - especially the high end which is seeing a complete meltdown. But then again, $850,000 for a two bedroom condo seemed a bit high, didn't it? Didn't it?!

Date Inventory 25th % 50th % 75th %

11/21/2005 13,782 $265,000 $355,000 $559,900

11/14/2005 13,295 $267,000 $359,000 $569,000

11/07/2005 12,813 $269,000 $359,900 $574,999

11/01/2005 12,275 $268,000 $360,000 $575,000

10/28/2005 11,959 $269,000 $364,500 $579,000

10/21/2005 11,287 $269,000 $368,800 $589,900

10/14/2005 10,845 $269,000 $370,000 $597,000

10/07/2005 10,169 $269,900 $374,990 $599,000

10/01/2005 9,264 $268,900 $369,900 $585,000

09/28/2005 9,118 $269,000 $369,900 $585,950

09/21/2005 9,352 $269,000 $375,000 $599,900

09/14/2005 8,907 $269,900 $379,000 $600,000

09/07/2005 8,319 $269,900 $380,000 $625,000

09/01/2005 8,030 $269,000 $380,000 $630,000

08/28/2005 7,979 $267,000 $379,900 $626,834

08/21/2005 7,769 $265,950 $379,900 $629,999

08/14/2005 7,447 $264,867 $379,900 $629,900

November 26, 2005

Uh-oh... Las Vegas housing prices slip

Another market that is gonna get real ugly real fast.. The land of the dreamer, Las Vegas, has seen a crazy real estate ride as investors bid up properties that have no potential future residents - there are simply no people to live in these units.

But now they're getting out. But there's so many units going up. So what happens to them - do they stop construction half-way up? Do they complete and go bankrupt, leading the bank to auction off units? What a mess in the making...

The median price of existing homes sold in October declined for the first time in six months, an indication that some of the air is being released from the resale pricing bubble, a local housing expert said Wednesday.

The median resale price in October was $285,000, down $5,000 from the previous month, said Dennis Smith, president of Home Builders Research. It's still an 11.1 percent increase from $252,000 a year ago.

"We don't give a lot of importance to a one-month change, but it is something to monitor during the next quarter," he said. "It could be that the supply of resales is high enough that the resale prices are entering an adjustment mode. But not to worry. It is not a long-term trend that will alter the overall Las Vegas market demand."

Smith said the resale price in Las Vegas was static until January 2004, when it began a steady climb from about $175,000 to $251,000 at the beginning of this year.

"This might be a good argument for those who believe our housing market was undervalued and was just catching up with West Coast prices," he said. "Maybe."

David Ehlers, chairman of Las Vegas Investment Advisors, suggests that Las Vegas residential real estate in general and high-rises in particular may be "on the verge of a major upheaval."

Realtors' bullish housing outlook questioned

Nice to see the mainstream press catching up with the bloggers in calling a spade a spade.. especially since one of the #1 advertisers in newspapers is the real estate industrial complex - builders, realtors, lenders, etc... Talk about biting the hand that feeds you.

But between the National Association of Realtors, and also local Realtors themselves, what a bunch of corrupt, and biased, wrong-headed and at the end of the day evil people. To knowingly spread lies, while leading the uneducated masses to sure financial ruin, is evil. How do they sleep at night?

When real estate agents try to sell a home, they often zero in on the positives -- big closets, great space for entertaining, lots of potential to expand.

It's the same tactic that the trade group representing many home sales agents, the National Association of Realtors, appears to be using right now: It asserts in a new report that a healthy housing market is here to stay and prices aren't likely to decline.

But that sounds awfully upbeat given recent data showing that home-builder sentiment has plunged and that price inflation in certain markets, including California and Florida, has started to slow. At the same time, inventories are up, mortgage applications are down and real-estate lending, particularly home-equity loans, remains soft.

Good read on manias - we've been here before folks

It's fun to read posts that deny we're in the bubble, or that the market has turned. It's one thing to argue against the #s. It's another thing to not have the understanding of financial markets and basic human behavior, and to not be able to see it in this obvious current situation

Here's a recap with some commentary:

Kindleberger's book provides massive historical evidence to support his assessment of the boom-bust nature of financial markets.

Basically,speculative excesses,financed in large part by margin account loans (mortgages) and easy bank credit (the Fed),leads to a pattern where the debt load of many market participants is overleveraged(no money down interest only loans).

Like the straw that breaks the camel's back,all it takes is an exogenous(or endogenous) shock to pop the speculative bubble (rising interest rates).

The value of the underlying assets of the overleveraged market participants collapses (here we go).

These individuals go bankrupt,causing a chain reaction (watch the panic as everyone tries to get out at once - see it in listing #s) as other participants are impacted by the bankruptcies and up bankrupt themselves.

The problem here is not necessarily irrational decision makers,but rational decision makers who lack sufficient relevant information (because of corrupt appraisers, biased realtors, financial press, and even greenspan's lies to apply the standard neoclassical decision techniques.

These decision makers KNOW that they don't know. They then decide to follow those whom they believe are better informed (if everyone is making money in real estate - so can I - it's easy!)

This leads to crowd,herd,and cascade effects that both creates the bubble and the crash (it's so obvious folks - the only question is when, not if).

November 25, 2005

US Housing Bubble - The Leak Is Growing Bigger

Good article, brings it all together... Highlights:

I ran into an old neighbor a few days ago. This fellow owns 250 units in San Diego. His oldest son manages 1,500 units. I asked him what was going on in real estate. He told me that we're past the peak, that prices are softening, and that it's taking longer to sell property in La Jolla and throughout San Diego. He added that all his real estate friends agree with that appraisal.

and

As the CA housing mania ends and the concept of risk returns to its rightful place, there is going to be a rush for the exit doors. Speculators are going to find out -- and many for the first time ever -- that as demand continues to soften, liquidity in real estate investments is far lower than they envisioned when they went in."

There will be great opportunities to buy houses at discounts during the down phase of the cycle. Be patient

A wise article, and a word of advice - patience. I like that. Things work in cycles. I think we all see where we are in this current housing cycle. The tippy tippy top - and just turned down the hill.

So that doesn't mean buy a house at a 10% discount - and get a "good deal". It means be patient. Really patient.

Remember whent the NASDAQ fell 10%? Didn't you just salivate, and buy more QQQ's? Then 20%. Then 30%. Then 40%. Then 50%. Then 60%. Then oh my god 70%! Then you paniced and sold! Right at the time it bottomed out and you should've been buying!

So.. Learn from that cycle, that bubble, that bust.

Horde cash. Don't buy housing. Stay out. Wait for a plateau. Heck, wait for houses to start going up agagin - say 6 months. No need to catch the very bottom. Most important, wait for rents to generate postive cash flow.

Your patience will be rewarded. Buy everything in site at that point. And retire on your cash flow and increasing asset base. Enjoy

"Surreal estate." I wish I were the originator of this phrase. I am merely an appropriator. It is the title of a column in the November 20th Sunday supplement on real estate in the San Francisco Chronicle, written by Carol Lloyd.

I have returned from the edge of the San Andreas fault. What I saw was not comforting.

You may think that you are immune. You are not. What you are about to read will affect you. Why? Because of the banking system. I learned something from a banker at a conference I attended that has forced me to reconsider my own plans.

Since 1996, bankers have built the banking system along an economic San Andreas fault.

6 Degrees of Housing Bubble at the Thanksgiving Table?

Let's hear some stories... Bubble talk dominate your table conversation too?

Those $300 laptops at Wal-Mart got some play too... as well as the working conditions in China that got us $300 laptops. Which then led to the trade imbalance caused by $300 laptops, which led to China buying up our bonds, which led to interest rates being artificially low, which led to.. the housing bubble!

It's like 6 degrees of Kevin Bacon - now substitute Housing Bubble

November 24, 2005

Check out these nasty listing and depreciation values from Miami - OUCH!

From the home of speculative condo flipper hell, welcome to bubble panic:

Date / Inventory / 25th Percentile / 50th Percentile / 75th Percentile

11/21/2005 18,261 $284,900 $405,000 $662,000

11/14/2005 17,601 $284,000 $405,000 $662,000

11/07/2005 16,952 $284,900 $405,000 $660,000

11/01/2005 16,424 $285,000 $410,000 $675,000

10/28/2005 16,425 $285,000 $410,000 $675,000

10/21/2005 16,977 $285,000 $409,900 $675,000

10/14/2005 15,894 $285,000 $409,000 $674,900

10/07/2005 15,296 $287,000 $412,000 $680,000

10/01/2005 14,953 $288,000 $415,000 $685,000

09/28/2005 14,655 $289,000 $415,000 $690,000

09/21/2005 14,251 $289,000 $417,900 $695,000

09/14/2005 13,604 $289,900 $420,000 $699,000

09/07/2005 13,064 $289,000 $423,900 $701,000

09/01/2005 12,800 $289,000 $422,900 $714,000

08/28/2005 12,882 $286,990 $420,000 $709,000

08/21/2005 12,606 $289,000 $424,900 $719,000

08/14/2005 12,361 $289,000 $425,000 $700,000

The Ugly Truth About Tax Reform and Home Values

Oh, those realtors at National Association of Realtors. Always worried about themselves... I'll sure miss 'em:

While tax reform and tax simplification may seem like a good thing at first glance, a look at the fine print of a recently released report by the President's Advisory Tax Reform Panel reveals some ugly truths for housing. Changing the mortgage interest deduction to a tax credit, eliminating the local property tax deduction and boosting capital gains taxes are just a few details that that could spell bad news for the American Dream of homeownership.

The reduction in home prices will not be an instant event. But over time, incentives for existing homeowners to continue owning would likely decline. Potential homeowners would no longer be able to include the property tax deduction in their home purchase cost calculations before buying a home.

Thus, it could appear to inflate the upfront purchase cost of a home. This has the potential for “scaring away” homebuyers. Therefore, a steadily declining demand will reduce home sales. Fewer sales mean less business for REALTORS

Slowing home appreciation in some markets bodes well for buyers

A report from San Diego (who can't seem to say to itself "declining home values" - still using "slowing appreciation"), including this gem:

Vaughan, 44, a manager at a Costco store, must sell his 2,885-square-foot house before he and his family can close escrow on a new home being built for them.

He first listed the house at $1.59 million and over time has cut his asking price as low as $979,000. That would still be a healthy return on the $461,000 he paid for it four years ago. Vaughan said he's reluctant to go any lower.

"I'm not out to kill anybody, I just want to get a fair price," he said.

So, a couple of thoughts:

1) This Costco manager, if he had sold his house a the $1.6 Million asking, would have made more in one house transaction than he would IN HIS ENTIRE CAREER

2) He didn't get his price, but you know people in San Diego were dumb enough to pay similar - but not anymore

3) This mentality will be what we see for a bit. Housing prices won't fall 50% next year. What will happen is people will post their homes for what they think they DESERVE (funny word). Not what the market will bear. Then they will over time keep reducing until they do get to that painful new level. This takes time.

Experts: Housing Bubble Burst is Imminent

The best line from this Cincinnati Post article sums it up:

A final nightmare scenario: A federal bailout of the mortgage market is likely if housing crashes, the center predicts. So, if corporate pension funds continue to falter and this dire prediction does come true, the Feds could conceivably be holding your mortgage and your pension.

However, we're all assuming the government to rush in and save everything. But has anyone seen our checking account lately?

Isn't George Bush an MBA? If so, any MBA (who went to class) would see that it's about time to start considering a bankruptcy filing. Especially to wipe the pension obligation from the books.

November 23, 2005

Housing inventory balloons in Orlando

Remember (just a few months ago) bidding wars? Remember "if you don't get in now you may get priced out of the market" panic? Remember splashy condo opening parties? Remember lines and lotteries? Oh, boy, isn't all of that seeming silly today?

The number of homes for sale in the Orlando area ballooned by more than 2,200 properties last month to hit an eight-year high -- the clearest sign yet that the region's red-hot housing market might be about to cool off.

Orlando's existing-home sales remained strong in October, a local trade group reported Tuesday. Completed deals in the four-county metro area were up more than 27 percent from October 2004, and the median price of those sold in the market's core crept up for the first time in three months to set another record.

But the bidding wars are subsiding, and the inventory of available homes jumped from 6,786 at the end of September to 8,992 at the end of October, according to the Orlando Regional Realtor Association. That's the largest inventory since 9,129 homes were for sale in May 1997.

Get your cash ready - Post-Bubble Real Estate Plays

Here's a write-up from Forbes. What I would suggest as the best plays for the next two years are:

1) Sell all of your personal real estate. Period.

2) Short homebuilders, lenders, Fannie and Freddie, home furnishing retailers and mortgage insurance companies

3) Raise cash and put into 4%+ savings (HSBC, Emmigrant Direct)

4) Wait

Then in 2008, swoop in like the vulture you are and buy distressed real estate, with positive cash flow as rental property.

Then grow rich. Period.

Here's Forbes:

If the housing market crashes, watch for apartment REITs to hit new highs.

Real estate remains an investment category with more emotional baggage than most. We have intimate daily contact with our own real estate, and it can be hard to separate what that means to us from what is happening in the vast and varied real estate marketplace.

While the industry continues to become ever more transparent, largely because of the increasing weight of institutional capital in the mix, there is still plenty of confusion and even obfuscation. There is also a continuing disconnect between the way investors may understand their personal real estate holdings and their perceptions of the public securities market for real estate.

With more buzz than ever about real estate, especially when it comes to talk of a housing bubble, it can be equally tough to separate what's really important from what marketers--and even your neighbors--might like you to think

Confidence in UK Housing Market Falls (Again)

I spent most of the summer in London, and will be living there next year (and renting!). A 1000 sq. ft. flat is about $1.2 Million in central London. And rents for $2000 a month.

Guess what. That doesn't compute. But the ponzi scheme went into full effect there, out of control, and it's been slightly declining last year as owners refused to sell at the correct price, thus listings up. Now you'll see the full pop in 2006. Good market to consider for what you'll see here - we're about 8 months behind. Joy - Jubilation - Concern - Worry - Denial - Panic - Capitulation. They're in Denial, moving to Panic in 2006. We're in Worry.

Despite strong returns from equities so far this year, and an apparent ‘soft landing’ for the UK housing market, the latest investor confidence index from the Association of Investment Trust Companies (AITC) is a gloomy read.

The research suggests that the UK’s love affair with property investment is on the wane, whilst this year’s stock market rally seems to have made active investors jittery rather than jubilant.

Whilst 30% of the general population said they still thought the housing market would produce better returns than the stock market over the next year, this represents a sharp drop on the 40% who said this last February and 53% who said this in January 2003. In contrast just 9% of active investors agree the housing market will outperform

Buy a condo and get a free car?! Wonder why it's not a GM!

The end of the world is here for condo developers. Watch the desperation as they try to unload.

You'll also start to see half-build complexes come to a halt... as investors bail, there are no buyers for $800,000 1000 sq. ft. apartments, and the developer's funding gets cut off

Desperation produces very interesting results. And promotions.

Denver gets worse? Amazing. Home cost, sales go down - Median price falls to $248,250; unsold inventory still large

I was in this market for a few weeks last month, and stopped to look at some lofts downtown and also homes in Boulder. For a market with ZERO appreciation the past five years (i.e. not playing in the bubble trouble) it was still WAAAYYYY over priced - $700,000 for a 2 bedroom house in Boulder, and $600,000 for a 1200 sq. ft. condo in Denver.

But boy were there listings - soooooooooooooo many listings. And they're STILL building lofts by the thousands - with no buyers.

So, duh, prices are coming down. In a market with no appreciation for five years. Ouch.

While November hasn't exactly been a turkey for Denver-area home sales, there's little to be thankful for if you're trying to sell your house in this mostly flat market.

Two reports released on Tuesday tracking the previously owned home market show that sales and prices are down and the supply of unsold homes didn't fall as much as expected.

In addition, rising mortgage rates and foreclosures are expected to continue to hammer the first-time housing market, experts said.

November 22, 2005

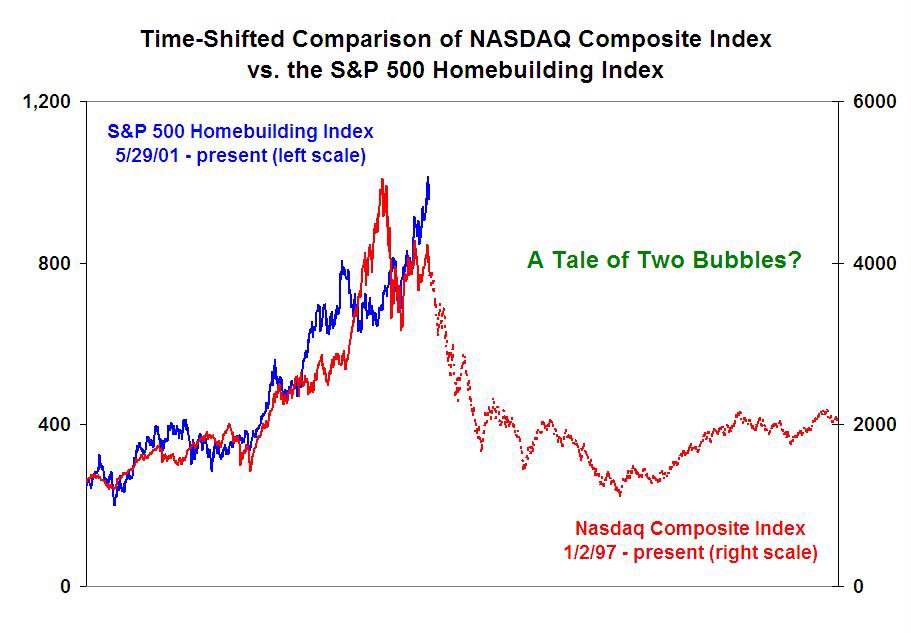

Feeling a bit 2001 lately? The housing bubble = the NASDAQ bubble

I'm really seeing erie similarities between the nasdaq bubble pop and our current housing bubble pop.

The Top 10 List:

1) "new economy" now "migration trends", "demographic demands" and "the country is filling up"

2) "day traders" now "speculators" or "real estate investors" or "flippers"

3) "pump and dump stock manipulators" now "realtors"

4) "margin accounts" and "leverage" now "mortgages"

5) "Henry Blodgett" now "National Association of Realtors"

6) "Worldcom" and "Enron" now "Toll Brothers" and "Fannie Mae"

7) "analysts" working for "investment houses" now "appraisers" working for "realtors"

8) "penny stock" now "Miami condo"

9) "the stock market will always be your best investment" now "housing never goes down historically"

10) "irrational exuberance" now "froth"

How's that?

A bubble is a bubble is a bubble - generation after generation after generation. It's just humans being humans. The surprising thing about this one is that it was just so damn soon after the last one. Are we that stupid that we don't learn or that we selectively forget - so soon?

Real-Estate Speculators, Pulling Back, Help Fed Remove `Froth'

Boy, we sure went from panic buying (June - July) to panic selling (NOW!) quick didn't we?

I'm starting to think the only speculators left in the market are those who weren't lucky enough to unload this summer... but the question in on those hundreds of thousands of units currently under construction (Phoenix, Vegas, Miami for starters) - speculators put $5000 or so down to hold 'em, but what happens in 2006 when they walk away from their deposits - and the builders have no buyers?

Timber.

Lisa Tershak is offering to pay $5,500 in cash to anyone who buys her three-bedroom house in Leesburg, Virginia, near Washington.

She's reduced the investment property's asking price five times since July to $464,900, not far from the $450,000 she paid for it in March. ``There's too much inventory,'' says Tershak, 35. ``Everyone felt the bust coming and decided to dump their properties at the same time.''

Investors who helped fuel the U.S. housing boom by bidding up prices are now so desperate for buyers that some are offering cash bonuses in such markets as Washington. That's a sign the Federal Reserve is succeeding in removing some of what Chairman Alan Greenspan called ``froth'' from the market. Inventories of unsold single-family homes are near a 17-year high as demand from speculators wanes and mortgage rates have risen more than a percentage point from a four-decade low reached in 2003.

November 21, 2005

Hillary running away with housingpanic poll

32% of the vote today - McCain at 18%

So, will Hillary win? Is that good or bad for housing?

Day Late & Dollar Short: Homebuilder ETFs launch into softening market

New housing ETFs, new creative loans, and hundreds of thousands of condos about to come on the market

After the bubble has popped, and values are declining.

Timing is everything.

Boy, does it feel like 2001 all over again...

Wall Street often tries to cash in on investors' tendency to chase the latest hot trend, as evidenced by the technology and Internet funds launched in the run-up to the 2000 dot-com crash.

However, in the case of exchange-traded funds concentrated on the home-construction industry, asset managers may be behind the curve.

The first ETF focused on homebuilders recently began trading and another is in the works. The timing of the launches seems dubious, however, with the housing market losing strength after a prolonged bull run.

"We're seeing early signs of a softening housing market," said Brad Sorensen, senior sector analyst at the Schwab Center for Investment Research. "This housing boom was longer-lasting and more inflatable than previous ones, but the cycles are similar."

Vulture Alert (but can you blame them?)

You know, Warren Buffet said is his last report to shareholders that he's sitting on his billions in cash at Berkshire, waiting for the bubble to pop so that he can swoop in and buy real estate at distressed prices too...

Here's what Freepers are saying about the housing bubble and folks taking on unsustainable debt:

It is time for the greedy and the stupid to suffer. I'll be right their to cash them out of their debt and take their property for a HUGE discount.

Bankruptcy laws were changed just on time!

Exactly. Now people will have to pay what they owe.

I have a friend that did just that when property prices collapsed in the late 80's here in Austin. Bought Condo's with his credit cards.

He's a rich man

The pain of buying at the top

And there's never been a top like this one

Oh, the pain to come...

But then again, didn't $700,000 for a one bedroom condo seem a bit high?

Mia Muratori knows the lasting sting of buying at the top of the market.

In 1988, she bought a house in the Midtown Brandywine section of Wilmington after relocating with her husband from New York City. Soon after, the red-hot real estate market weakened with the savings-and-loan crisis, a softening economy and DuPont Co. job cuts. In the end, it took more than a decade for Muratori to see significant price appreciation. "Not a fun experience," she said.

"We were just off the turnip truck from Manhattan," said Muratori, who is an artist. "All I can say is, you never want to do it again. I never enjoy losing money."

November 20, 2005

Open thread - let's hear some stories about people buying at the top

Seems the stories about people buying this summer with zero down interest only negative ammortization loans, combined with an explosion in listings, combined with two straight months of median home price decline, isn't quite enough for some of the real estate agents and investors out there to understand that it's over, it's coming down and the ponzi scheme has ended...

Again, I'm not disputing that MASSIVE money was made during the ride up. Anyone can argue that point. The point now is that we're going down.

So... let's hear some stories about people panic buying this summer at the top. Here's one:

I have a friend in San Diego who purchased a new build 1200 sq. ft. loft downtown in June for $700,000. Usual story - interest only, 5% down, financed on credit card, etc...

He reports now that

1) He doesn't seem to have any neighbors - all the units were bought by flippers and are now for sale, with no buyers

2) He's worried if it's already droppped 10%, he's $70k in the hole

3) He figured he could've rented one for about 30% of his monthly total cost

4) He thought it was a sure thing - that real estate only goes up - and can't believe how quick things changed

November 19, 2005

Housing Bubble Q&A with UCLA Forecast

The #1 reason I know we're in a bubble is the cost of rent vs. the cost of ownership, or the PE ratio of housing - which is completely and totally out of whack (as I sit here in a $700,000 condo renting it for $2000 a month, vs. the $5000 cost of owning it)

This economist from UCLA, who is much smarter than me, does a good job walking through the reason and proof of the pubble. And what will happen. VERY important read - enjoy

A real estate bubble, or any asset bubble is not a situation where you hear a pop. Everyone always associates bubble with a pop. They think, gee, if there's a bubble, there must be a pop! coming at the end. That's not what a bubble is. A bubble is when the price of an asset becomes misaligned with the fundamentals that truly determine the price of that asset.

Let me give you an example of what I'm talking about here. Amazon dot-com -- let's go back to the NASDAQ days. At one point in time, Amazon was worth $180, $190 a share. The big question is: was that stock worth $180, $190 a share? Well, what determines the price of a stock? It's the net present value of the profits that accrue to that stock in the future. That's what we teach our MBA students. When they buy that stock, you're buying a share of the profit stream that comes from that company today and in the future. Some bright economist at one point in time, sat down and said, "Well, gee. What if Amazon dot-com captured 100 percent of the DVD, book and CD market in the U.S.? Would they ever make enough profits today or in the future to justify a share price or the market capitalization implied by the share price of $180, $190 a share?" And the answer was no way.

So, when you're talking about a house, and when I say we have a housing bubble, what I'm talking about is that the price of a house is determined by the stream of profits that accrue to that property today and in the future. And that of course is determined by the rental value of that property today and in the future.

Now, the reason I go through all this is, because you have to ask yourself the question, are we in a bubble market or not right now? And the answer is, as I firmly believe, is we are in a bubble market. And the reason I believe that is, there is no justification, there's no underlying fundamental that would make me think that a house in California today is worth 40 or 50 percent more than it was two or three years ago

From the belly of the beast - realtor talking points on the bubble

Here they are folks - National Association of Realtors' (NAR) talking points used to calm freaked out buyers and sellers. Aren't they great? The nice thing is after it bursts, we'll have this smoking gun to shove back in their face

There is virtually no risk of a national housing price bubble, based on the fundamental demand for housing and predictable economic factors. It is possible for local bubbles to surface under the right circumstances, but that also is unlikely in the current environment. There are tight supplies of homes available for sale in most of the country, and labor markets have been improving. In other words, the two conditions necessary for price softness do not exist in most of the country.

The first 1,500 of millions - Ameriquest Mortgage to Cut 1,500 Workers

So many jobs that won't be needed anymore

* realtors

* mortgage bankers

* appraisers

* new home builders

* developers

* investors

* title agents

* home depot clerks

but, then there are the new ones that will be needed

* bankruptcy lawyers

* credit counselors

* psychiatrist

* auctioneers

* foreclosure specialists

* prison guards

* real estate bloggers

The corporate parent of Orange-based Ameriquest Mortgage today said it would lay off 10% of its workforce — about 1,500 employees — as the long-running housing boom and demand for home loans cools off.

ACC Capital Holdings, which also owns AMC Mortgage Services and Argent Mortgage, would not identify where it would cut jobs or provide other details about the layoffs.

"The mortgage industry is entering a more challenging phase of rising interest rates," the company said in a statement. "In cyclical industries such as mortgage lending, periodic workforce reductions are not uncommon."

After benefiting for years from a booming housing market, mortgage lenders now face an industrywide slowdown as a rise in interest rates has dampened demand for refinancings and new loans.

FLASH: San Diego has one honest realtor - writes today that market deflating

I can't believe I'm reading this. Just when I thought there were no honest realtors and that realty times wouldn't let one publish anything honest, BOOM - a realtor in San Diego writes the obvious - that the market has turned, that a 20%+ drop is coming and that the ponzi scheme is over

Wow.

Enjoy.

San Diego Real Estate -- A Trend to Go National?

Just this summer, it was almost impossible to find a new San Diego real estate development that cooperated with real estate brokers. If you could find a developer co-opting, it was most likely way below the traditional 3 percent rate.

Well, just a few short months have passed and a current read of the Sunday homes section of the San Diego Union Tribune shows that though the real estate market does not make discernible moves in a day like the stock market, a couple of months can easily define the local real estate trends

With Real Estate, This Time it Really is Different

A well layed out case - with all the guilty parties listed.

Anyone want to guess when the FREAK OUT headlines will start appearing, like

"Housing values plummet"

"Trading curbs put into effect as market meltdown continues"

"No buyers, too many sellers - and a reversion to the mean"

The housing mania, like all manias that have preceded it, is finally coming to a long overdue end. Time tested principles of prudent mortgage lending will inevitability return, and houses will once again be regarded merely as places to live. However, the country will be a lot poorer as a result of the unprecedented dissipation of wealth and accumulation of consumer and mortgage debt which occurred during the bubble years. Before real estate prices can return to normal levels, they will first have to get dirt cheep. It has been a wild party, but in the end all that will remain is a giant hang-over.

Updated Phoenix listing #s - Watch the fun as a market collapses under its own weight

Just saw a few listings - one a loft in Scottsdale selling for $1000 per square foot. That's right. $1000 per square foot. Another a new build in a bad neighborhood in Tempe selling a 2 bedroom for $750,000. On a busy road, next to crack den houses, with planes flying over.

Who's buying this stuff besides investors trying desperately to flip? The rent on that tempe unit would be $2000 or less (likely $1,400). But the cost of ownership would be $5000 or more a month.

Amazing.

Tracking Phoenix/Maricopa & Pinal Counties

Population 2005: 3.8 million

Listing per population ratio 7/20: 1:353

Listing per population ratio 11/10: 1:150

7/20: 10,748

7/30: 11,656

8/10: 13,099

8/20: 14,321

8/30: 15,042

9/10: 16,716

9/20: 17,516

9/30: 18,799

10/10: 20,073

10/20: 21,806

10/30: 23,770

11/10: 25,387

11/11: 25,700

11/15: 26,054

11/18: 26,261

An excellent series on what's coming - THE DAY AFTER TOMORROW

Sit down with a cup of coffee, and your finger on the "sell" button, and read this excellent "what if" series in Financial Sense. Here's a snippit

Adding to the bearish overall tone is the further collapse of Residential property markets where some area’s now report no bidders, and home values down over 60% from the 2005 all time highs. In many areas, homeowners with no equity have simply walked away their properties handing back the keys and filing personal bankruptcy

So... anyone out there holding a $500,000 mortgage? Sweating a bit?

Can you say "global economic meltdown?" - Dangers of a runaway mortgage market

The warning signs are everywhere. And conservative financial institutions -- insurers and pension funds -- are set dead in the path of the runaway train.

The long-awaited slowdown in the U.S. housing market is upon us. So far the deceleration is a long way from a car wreck. Housing sales and housing prices are still projected to climb in 2006, just not as fast as in 2005.

But over-revved markets generally crack up rather than slow down gracefully: They've built up too much momentum to handle a change in direction without at least a bang against the guardrail.

Adding to the odds of a crackup is the very peculiar nature of the investment market for mortgages. Right now, there's a huge disconnect between the folks who are making the mortgage loans and the investors who ultimately wind up owning the mortgages. The mortgage lenders who know individual mortgage borrowers the best -- and the risk they do or don't represent -- are selling their riskiest mortgages. The investors who buy them know nothing about individual borrowers and are relying upon the magic of the Wall Street derivative market for risk protection.

Sound like a car wreck waiting to happen?

November 18, 2005

Shouldn't this be illegal? The world’s worst mortgage

OK, consumers should have some responsibility in this mess.. nobody says you HAVE to buy a house. But come on folks, take a look at this potential mortgage disaster:

Here's a deal for you: Put no money down, pay only interest, or skip payments entirely. Mix too many of these features and you dig a hole you can't ever hope to escape.

I have tried to devise the absolute worst mortgage loan that I can imagine. Fortunately, this loan is nothing more than a figment of my imagination -- at least, as far as I know.

I made it hard on myself. Although I dreamed it up, the world's worst mortgage couldn't include anything that doesn't exist in the market today. So that disqualifies imaginary elements, such as mortgages written on acid-spraying exploding clay tablets. I just took the worst elements of all the existing mortgages and assembled them. Here's what I came up with:

Housing Experts Change Their Tune

So the question is, can people who bought a home this summer sue anyone - kind of like suing the analysts who were pumping the .com stocks at the same time they and the insiders were getting out?

Besides Greenspan, most evil on my list is Bob Toll.. who enriched himself and cashed out, at the same time denying any softening or bubble, even though he knew DAMN WELL what was happening because he had visibility.Shhh ... just listen ...

It was only a few weeks back that I suggested home shoppers not believe everything they hear from the oft-quoted, so-called Experts regarding the housing market. There was a pretty straightforward reason.

Despite much evidence to the contrary, the people with a vested interest in continuing to see prices rise -- like the outgoing Fed chief, Alan Greenspan -- kept telling the soundbite-seeking press that there was no "bubble." Regional bubblets, maybe. Well, not even bubblets. Areas of higher enthusiasm, really. Everything was just fine. Nothing to see here. Not then, anyway. Not way back in ... July

November 17, 2005

Outlook sours for real estate - Did homeowners who sold in September get out just in time?

I sold my over inflated condo in July... Think I'm sleeping well at night?

And more and more leading indicators are pointing to a slowdown.

In Boston, real-estate investor Matthew Martinez reports recently having spoken to five condo converters. "They all said the party was over," Martinez said.

In Florida, Elena Filipa, vice president of the Corcoron Group in West Palm, said "We've leveled off. I would say prices will go up this year, but not as fast as they have."

None of this surprises the many economists who have been waiting for a downturn.

Richard DeKaser, chief economist for mortgage banker National City, has been reluctant to call the top, but thinks it has finally passed.

"We're coming down the other side of the mountain," said DeKaser.

Housing boom past its peak? October starts, permits fall more than expected in latest sign of softening real estate market.

Readers - tell us about any stories you're hearing from the street - you, neighbors, etc... Nothing better than a good bubble story

The pace of home building slowed sharply in October as higher mortgage rates began to bite, a government report showed Thursday, in the latest sign that the housing boom may have peaked.

Housing starts fell to an annual rate of 2.01 million in October from a revised 2.13 million pace in September, the Commerce Department reported, while economists surveyed by Briefing.com had forecast a reading of 2.06 million.

Deflating the bubble: A good thing

Can you imagine the pain of buying a $500,000 1 bedroom condo four months ago that is now worth $480,000 (ouch - $20,000 loss in 120 days) and will be worth $300,000 in two years (ouch - $200,000 in debt and now I'm bankrupt!)

People are going to be mad - at the world, at realtors, at bankers. But in the end, the only one to blame will be themselves.

What goes up, must come down. All good things come to an end. Nothing lasts forever. The supply of clichés is endless and right now all of them fit the U.S. housing market: It had to happen sooner or later, the bubble had to start deflating or eventually it could have popped.