As advocated in Life 2.0 (good book - read it last year - on sidebar now) - the idea is to cash in on your house in over-valuedburgh, and buy low (or rent) near cornfields. Small town America. Where $100,000 gets you a great house. I'd suggest foreign countries too for this idea. Central America, Mexico, Eastern Europe, etc.

Cash in. Don't stress about $. Raise your kids right. Retire early. Slow down.

Anyone doing it? It is tempting...

On Geographic Arbitrage and Corn Fields

Thank you Rich Karlgaard http://www.life2where.com/ for helping me finally pull the trigger on the big move from the "skyrocketing coastal markets" to the flyover country. Reading Karlgaard's book "Life 2.0" and Po Bronson's "What Should I Do With My Life", have really helped me to grasp what it means to exit the California race for AM freeway position and enjoy a fuller life. Now, I'm taking my CA income and job to Des Moines Iowa.

We were able to spend some time there and my business travels keep me in the Midwest quite often and I've come to enjoy it. I realize that living there, snow, cold, etc. will be a shock for a while. But, as I frequently say to friends and family, "I don't know about you...but I tend to drive 2 hours a day to work inside an office after exiting a climate controlled car and then it's too jammed on the freeway all weekend long to actually go anywhere without popping a vein and I have 2 kids under 3....so what am I missing by moving to a different climate???"

As discussed in Life 2.0, we'll probably find a very nice house of roughly 2.5 X the size for about $250k. Yes, you can write a check for houses like that coming from CA. I wont but the thought of saying, "I'll write you a check right now if you take $25k off so I can go buy the Volvo instead of the Hyundai" feels nice.

The most important aspect of this move is obviously my family since money in the bank and a great house doesn't mean jack if things aren't good at home. My wife is a native Californian with relatives all over with frequent interaction. I'm an only child with parents in Ohio and have a very small family who doesn't get together. This has been a long road for her and to hear her say to our friends and family that, "This is the right thing for our family and for our future" makes me beam with joy.

I plan to chronicle the move and plan to write essays/articles on my "transition" to that Midwest lifestyle...and I can't WAIT for "The Iowa Caucuses" :).

My friend who just moved from CA to Utah told me, "You know Doug, on Sunday, you just want to put a bullet in your head". After laughing for about 5 minutes and joking about "Knowing who isn't Mormon by looking outside on Sunday at 11AM and watching smoke rising from the backyard BBQ and listening for the roar of NASCAR on the idiot box"...my friend admitted that he's actually starting to wind down a bit and is enjoying the slower pace.

I look forward to that.

February 28, 2006

Anybody practicing Geo-Arbitrage yet?

Can't sell your home? Get on ABC News and tell your story

![]()

Of course, let 'em know that HousingPanic sent ya!

Seriously, these kinds of stories in mainstream press are only going to make the bubble pop harder and faster as panic sets in. You can blame the media, but the media is just a mirror in the end. They didn't cause the bubble and they didn't cause it to collapse. We did.

Real estate. At times it seems that's all people want to talk about!

As the previously booming housing market shows signs of slowing down, ABC News wants to hear your real estate stories.

For example: Did you wade in to the speculator's market and buy a condo that now you can't sell?

Some home developers have offered deals like $100,000 off a new home or $10,000 gift cards at electronic stores. Did you buy a home because of these promotions? Are you thinking of selling your home now out of fear that prices will drop? Are you holding off on buying hoping prices will drop?

If this sounds like your experience and you'd like to share your story, please fill out the form below and let us know whether an ABC News producer may contact you to possibly include you in one of our reports. Make sure to include a phone number where you can be reached, and we may give you a call.

Bogus inflated appraisals? SHOCKED! Shocked I am!

The congressional hearings will have to address this big-time. Appraisers everyone knows are the puppies of the realtors (who spiff them) and the mortgage bankers (who get them their business)

The system was cooked to force these guys to "hit the number". Well, who got screwed? Not the realtor, not the banker, and not the appraiser.

The homeowner. Big time. Even if he doesn't know it (yet). He's still out buying Hummers with his new refi wealth (oops!)

A go-go real estate market is partly responsible for the inflated appraisal epidemic that gives consumers a false sense of their home’s worth. One disastrous result: mortgages and refinanced loans that exceed the value of a home and create crushing debts that can take years to pay off or lead to foreclosures.

Annie Lewis knows what that feels like.

“It’s a very sick feeling,” said the Lee’s Summit woman, who fears losing the recently built condo she bought in 2003 for $94,000.

In 2004, she responded to an Ameriquest TV ad to consolidate her debts by refinancing her home. She was delighted when an appraiser sent by the company valued her condo for $129,000 — a 37 percent leap in value in little more than a year. She paid off bills and settled for a 7.7 percent adjustable rate mortgage.

But it was too good to be true. This past year, six lenders rejected her efforts to get a new, fixed-rate loan to keep her interest rate from rising. All said her condo was overvalued and is only worth $108,000.

Appraisers said the problem began to grow with the housing boom and low-interest rates that spurred aggressive loan brokers to encourage consumers to refinance their loans. The carrot dangled in front of consumers — in thousands of direct-mail campaigns, TV commercials and Internet ads — is freed-up cash to consolidate debts.

But to make such high-dollar loans pass muster with underwriters, unscrupulous loan brokers chasing big commissions pressure appraisers to meet predetermined values. In other words, artificially inflate the value of the homes to justify the costlier loans.

Countrywide's Mozilo and Yale's Shiller predicting 30%+ meltdowns

Sorry, no link - from BusinessWeek. However, here's the killer quotes from Mozilo and Shiller. And don't forget, Mozilo has already cashed in bigtime, dumping his Countrywide shares.

Run. When the insider fat cat who made the loans is telling you it's about to fall apart (and in the media - not drunk at a cocktail party), trust him, it's about to fall apart. Amazing.

How severe are the price declines you are expecting?

MOZILO: I would expect a general decline of 5% to 10% throughout the country, some areas 20%. And in areas where you have had heavy speculation, you could have 30%. We will see…sellers back off from the prices they have been demanding. A year or a year and half from now, you will have seen a slow deterioration of home values and a substantial deterioration in those areas where there has been speculative excess.”

“SHILLER: In Los Angeles in the last cycle, prices peaked in 1989 and bottomed out in 1997. In that interval, L.A. lost 40% of its real value. I can see that happening there again or in any of the cities that have had tremendous price increases, and there are quite a number of them in this country. I think a pullback of as much as 40% is plausible in many places.”

Where are the most vulnerable areas?

MOZILO: Miami and Fort Lauderdale. Las Vegas is another area where there is heavy speculation. That means people were buying three, four, five condos at a time and thinking they can flip them. Those are the spots we have identified where… we will only make loans when we know the person will live [in the housing].”

“SHILLER: The most spectacular cases are Phoenix and Las Vegas. They soared so suddenly. But others [are vulnerable, too,] such as San Francisco, San Diego, L.A., really much of California.”

Wonk alert: Pimco's Gross spells it out

I'd trust this guy with my net worth and the keys to my house. Brilliant economist, always spot-on in my experience. And this March 2006 report is one of his best:

A copy of the annual Economic Report of the President arrived at my desk the other day, replete with a giant bald eagle on the cover and formatted, incredibly enough in OVERSIZED print – fit for an aging boomer population. My compliments to the chef, at least for the exterior garnishments. The verbiage however, was another story.

It’s not so much that the report was a compilation of untruths or even half-truths. It’s just that it failed to tell the truth, the whole truth, and most definitely nothing but the truth. Although submitted by ex-CEA Chairman and newly christened Fed Chairman Ben Bernanke, it was as if it had been written by Dick Cheney, a man who not only cannot shoot straight but seems to have difficulty talking straight as well.

If there were WMD in our economic future, you’d be hard pressed to find them here. Mild innuendos about global and demographic challenges yes, but nothing that couldn’t or wouldn’t be overcome with good old American ingenuity, hard work, and a fawning foreign investment public nearly trampling each other to get their hands on attractive U.S. "investments."

Nowhere to be found was the catchy phrase à la Tennessee Williams referring to the "kindness of strangers" or a suggestion of "living on borrowed time." Our 700 billion dollar current account deficit, in fact, could and might continue "indefinitely" as long as we use the capital inflows in ways that promote future growth, the report intoned.

Ah, but that, it seems to me, was the critical rub. Have we, can we, will we use capital to foster future growth or must we earmark it for future liabilities that have been under-reserved? Have we borrowed from the future to pay for today’s party and will our future creditors allow us to pay it back on our own terms with low yields and a strong dollar? While the gang that couldn’t shoot (or talk) straight expressed few doubts, I as you can probably tell, have mine. Let me summarize a few of the pertinent chapters of this year’s report to help you make up your own mind

Here's his conclusion. Run folks. Run for the hills. And get your money out of dollars and out of the US market. Tilt.

Instead, our solutions more likely will pursue an easier trail, characterized by currency devaluation, the inflating away of long-term pension liabilities, and the payment of rising healthcare expenses via higher personal and corporate taxes. Investment markets in the United States will not ultimately prosper under such an increasingly odorous environment. It is only sensible, therefore, to diversify globally. Sorry for the straight talk folks, but don’t you think it’s about time?

February 27, 2006

Beazer homes paying Virginia buyer agents 7% (not 3%) commission for any sucker (i.e. buyer)

Shouldn't this be illegal? It's at least immoral. But then again, realtors are the cesspool of humanity...

The congressional hearings will address this one... like paying Henry Blodgett to pump pets.com

Desperate home builder ups commission to 7%

New home builder Beazer Homes is offering a 7% commission to agents that can convice a buyer to purchase one of their pricey, unsold Virginia homes.

The ad was in Saturday's Washington Post (page F-16). The 7% is not split between two agents. No, the entire 7% goes to the buyer's agent.

This is more than double the standard 3% commission on new homes. This is the latest red flag showing the increasing desperation by home builders who are anxious to sell their stock of unsold homes before prices deteriorate further. It seems to me that the benefit of a price reduction (that extra 4%) should go to the buyer of the home rather than to their agent.

But instead of passing the savings on the buyer, Beazer has decided to double to ransom for agents who manage to lure in a buyer.

Number of Unsold Homes Hits Record High

So many homes - old ones and new ones - coming on market - at the EXACT wrong time

Number of Unsold Homes Hits Record High in January, Shows That Market May Be Cooling

The backlog of unsold new homes reached a record level last month, as sales slipped despite the warmest January in more than 100 years.

The Commerce Department reported Monday that sales of new single-family homes dropped by 5 percent to a seasonally adjusted annual rate of 1.233 million units last month. That was the slowest pace since January 2005 and left the number of unsold homes at a record high of 528,000.

Analysts viewed the new data as further evidence that the nation's red-hot housing market, which hit record sales levels for five straight years, has definitely started to cool.

"The decline in new home sales in January makes it clear that there is some real softening in the housing market, said Joel Naroff, chief economist at Naroff Economic Advisors.

The 5 percent decline was bigger than expected, dashing hopes that the milder-than-normal January would help to bolster demand. The warm weather had pushed up the level of construction starts last month by 14.5 percent, the fastest rate in three decades.

But the new report showed that with sales lagging, the increase in building activity left a total of 528,000 new homes still for sale at the end of the month, a nine-year high.

Ian Shepherdson, chief U.S. economist at High Frequency Economics, predicted "real downward pressure on prices over the next few months."

Home sales data out - it's a long, long way down (and here we go)

No surprises... except the absolute devastation in the Northeast numbers...

Bigger-Than-Expected Drop in New Home Sales Indicates Five-Year Housing Boom Is Slowing

WASHINGTON (AP) -- Sales of new homes fell for the second time in three months in January, providing further evidence that the nation's five-year housing boom is slowing.

The Commerce Department reported Monday that sales of new single-family homes dropped by 5 percent to a seasonally adjusted annual rate of 1.233 million units last month.

That was a bigger drop than analysts had been expecting and provided support to the view that the housing market, after setting sales records for five straight years, is slowing under the impact of rising mortgage rates.

The biggest decline was a 14.9 percent decrease in sales in the Northeast, which followed an even bigger 23 percent plunge in sales in December. Sales in the Midwest were down 10.8 percent after having risen by 21.2 percent in December. Sales fell by 10.3 percent in the South in January following a 1.2 percent gain in December. Bucking the national trend, sales in the West posted an 11.3 percent increase in January after a 6.3 percent gain in December.

Some economists have expressed concerns that once home sales start to slow, the big price increases of recent years could turn into sharp declines in a similar pattern to how the speculative bubble in stocks burst in 2000.

House prices doubled. Gas prices doubled. Real estate taxes doubled. Health insurance costs doubled. Yet no inflation?

Another scam to add to the list (thanks 41 caddy for starting the discussion) is the way your government calculates inflation - rigged so that they don't have to increase the payouts on social security or pensions

But you can't kid a kidder. We all see prices skyrocketing, and people on fixed incomes falling behind - way behind. Especially when they get their new property tax bills. They could sell their home, cash out, and rent, but if they don't they gotta come up with the new cash. Refi?

Thanks to China (oh, wait, I mean WalMart) inflation on corn and beans is deflation. But we'll need a lot of corn and beans to make up for healthcare, or oil, or electricity, or taxes.

Statistics lie on the true cost of living

Take inflation. It's true that measured inflation is very low, but look at all that's left out.

In the case of health care, the government's consumer price index tracks the cost of medical services. But it is less precise about tracking who pays for them. If your employer's health plan is increasing your share of premiums and cutting the company's contribution or if the plan is increasing out-of-pocket charges or reducing what drugs it will cover, this shift is accounted for indirectly, after a lag of two years. But it hits your pocketbook immediately. And if rising medical costs deter you from seeing the doctor, that doesn't show up in the index at all.

Or consider housing. There are parts of the country where housing prices have been declining for a decade because few people want to move there. Statistically, these declines get averaged with astronomical housing costs in major metropolitan areas to show only modest average housing inflation. Around big cities, prices have plateaued at very high levels that are plainly outstripping incomes.

Try telling a young person in Greater Boston or New York or LA that there's no serious housing inflation or that rents have not increased faster than earnings.

The inflation numbers also fail to capture pocketbook realities for retired Americans. A low official inflation rate plays a cruel trick on seniors. For starters, it means that cost-of-living adjustments in Security Security checks are mere pocket change. One new prescription can more than eat up this year's Social Security increase

February 26, 2006

Housing bomb

tick... tick... tick...

Starting this year and picking up speed in 2007, as much as $2.5 trillion of non-conventional mortgage debt is scheduled to be repriced. Millions of Americans will soon face significantly higher mortgage payments. Unfortunately, many can barely afford their current payment.

Why is this happening? What will be the consequences?

In a bid to keep business booming, banks and mortgage lenders in recent years have found “creative” ways to make home loans more affordable—even to people with spotty credit histories or weak credit. By issuing “hybrid” mortgages that typically have low interest rates in the first two years, lenders have been able to entice otherwise unqualified buyers into buying a home. However, the initial low “teaser” rates must eventually be adjusted to the fully indexed level of whatever index is specified in the loan agreement. These adjustments are coming due in a big way, this year and next. That means mortgage payments are set to climb hundreds of dollars a month for a substantial number of Americans!

Phoenix collapsing - but news to many

Up 50% one year (thank you speculators). Down 33% the next year (thank you speculators). Yet many of the dolts in Phoenix have no idea what hit 'em... Guess they're still playing three card monty or reading their Herbalife brochure...

Bad news for the many homeowners trying to sell: It's likely only going to get tougher. The number of home listings in metro Phoenix is at an all-time high. In January, there were 30,113 houses for sale across the Valley. A year ago, there were 3,402.

Some sellers still don't realize the housing market has deflated from last year's peak. Not only are the bidding wars gone but so, too, are many of the buyers. Most of the speculators who sparked multiple offers on homes early last year are long gone, and there aren't as many regular buyers because fewer can afford today's higher home prices.

The typical house costs 50 percent more, and the typical income climbed less than 5 percent in the past year.

HP readers - post your local conditions here

Sea of for sale signs or still hot?

Realtors scrambling for new employement or shopping for new Lexuses?

Neighbors starting to freak out, or bragging about huge gains still?

Someone tell us how what happened to housing wasn't just a classic Ponzi scheme

Ah, they're so obvious when they're over. What were we thinking?

A Ponzi scheme is a fraudulent investment operation that involves paying abnormally high returns ("profits") to investors out of the money paid in by subsequent investors, rather than from net revenues generated by any real business. In fact, a Ponzi scheme must have abnormally high short-term returns in order to entice new investors. The high returns that a Ponzi scheme advertises (and pays) require an ever-increasing flow of money from investors in order to keep the scheme going.

The system is doomed to collapse because there are little or no underlying earnings from the money received by the promoter. However, the scheme is often interrupted by legal authorities before it collapses, because a Ponzi scheme is suspected and/or because the promoter is selling unregistered securities. (As more and more investors become involved, the likelihood of the scheme coming to the attention of authorities will continue to increase.)

The scheme is named after Charles Ponzi, who became notorious for using the technique after immigrating to the United States from Italy in 1903. Today's schemes are often considerably more sophisticated than Ponzi's (though the underlying formula is quite similar), but the principle behind every Ponzi scheme is to exploit a lack of judgment based on greed.

I'm seeing a lot of ads for pre-construction condos in Dubai... you know what that means!

Amazing how similar these things are no matter where I look - Dubai, Miami, Ireland, Phoenix, ...

same stock-art photography (I swear every 21 year old kid must be a millionaire - and like wine)

Dubai.. heard it gets to 130F in the summer. Nice place for a $1 Million 1000 sq. foot condo...

Here's a good article - and good warning:

On Sunday, I took a tour of the Blue Mountains here in Australia. (The kids loved part of this trip… where they got to feed and play with kangaroos freely walking around, and pet koalas, etc.)

My wife and I struck up a conversation with a couple sitting next to us on the bus…

“Where are you from?” we asked.

“The kids are in California, but we’ve now moved to Dubai,” they answered.

“How’d you end up in Dubai?” I asked. They lit up…

“He’s a pilot for Emirates airlines. We absolutely love it!”

“Isn’t there a real estate bubble underway there?”

“Oh, well, we’re hoping for another double…”

No joke… that’s what they said. And then the husband said the secret phrase… “you know, the National Bird of Dubai is the construction crane.”

“Say no more,” I said.

Shanghai's hot housing market has fizzled after a run-up fed by speculators, threatening a significant part of China's economy.

Thought we'd go around the world for a bit and peek in on collapsing real estate markets. First up... Shanghai! A bubble is a bubble is a bubble. Just change the names... Phoenix for Shanghai

American homeowners wondering what follows a housing bubble can look to China's largest city. Once one of the hottest markets in the world, sales of homes have virtually halted in some areas of Shanghai, prompting developers to slash prices and real estate brokerages to shutter thousands of offices.

For the first time, homeowners here are learning what it means to have an upside-down mortgage — when the value of a home falls below the amount of debt on the property. Recent home buyers are suing to get their money back.

Banks are fretting about a wave of default loans."The entire industry is scaling back," said Mu Wijie, a regional manager at Century 21 China, who estimated that 3,000 brokerage offices had closed since spring.

Real estate agents, whose phones wouldn't stop ringing a year ago, say their incomes have plunged by two-thirds.Shanghai's housing slump is only going to worsen and imperil a significant part of the Chinese economy, says Andy Xie, Morgan Stanley's chief Asia economist in Hong Kong.

Although the city's 20 million residents represent less than 2% of China's population of 1.3 billion, Xie says, Shanghai accounts for an astounding 20% of the country's property value. About 1 million homes in Shanghai alone — about half the number of housing starts for the entire United States in 2004 — are under construction."They'll remain empty for years," Xie said, adding that a jolting comedown also was in store for other Chinese cities with building booms — including Beijing, Chongqing and Chengdu — though other analysts say the problem is largely confined to Shanghai.

February 25, 2006

Cancelled home orders: Latest bubble prick?

And to think we're just getting started.... Boy this feels like what happened to Cisco in 2000.. build all this capacity and then poof! The orders dry up and the cancellations pour in.

Home builders are growing concerned about an increasing number of cancelled new home orders, which experts say could be a sign of an underlying weakness in the recent run in home prices.

Specifically, the cancelled orders could be the latest warning sign that buyers who were turning to real estate as an investment, rather than for their own housing needs, are shifting out of real estate. And that could mean that in many hot markets, the air is about to come out of over-inflated real home prices overall.

The flight of investor-buyers from the housing market and the increased cancellations could therefore push real estate prices lower in different markets.

"If you've overbuilt the market and sales get cancelled, you have to do something with the homes," said Seiders. "The incentives we're seeing builders offering are clearly designed to support prices and stop cancellations."

Wonk alert: Start getting your heads around the issues with the Dollar. It will have an enormous impact on your lives

In the short run, the issuer of a fiat reserve currency can accrue great economic benefits. In the long run, it poses a threat to the country issuing the world currency. In this case that’s the United States. As long as foreign countries take our dollars in return for real goods, we come out ahead. This is a benefit many in Congress fail to recognize, as they bash China for maintaining a positive trade balance with us. But this leads to a loss of manufacturing jobs to overseas markets, as we become more dependent on others and less self-sufficient. Foreign countries accumulate our dollars due to their high savings rates, and graciously loan them back to us at low interest rates to finance our excessive consumption.

It sounds like a great deal for everyone, except the time will come when our dollars-- due to their depreciation-- will be received less enthusiastically or even be rejected by foreign countries. That could create a whole new ballgame and force us to pay a price for living beyond our means and our production. The shift in sentiment regarding the dollar has already started, but the worst is yet to come.

The artificial demand for our dollar, along with our military might, places us in the unique position to “rule” the world without productive work or savings, and without limits on consumer spending or deficits. The problem is, it can’t last.

Price inflation is raising its ugly head, and the NASDAQ bubble-- generated by easy money-- has burst. The housing bubble likewise created is deflating. Gold prices have doubled, and federal spending is out of sight with zero political will to rein it in. The trade deficit last year was over $728 billion. A $2 trillion war is raging, and plans are being laid to expand the war into Iran and possibly Syria. The only restraining force will be the world’s rejection of the dollar. It’s bound to come and create conditions worse than 1979-1980, which required 21% interest rates to correct. But everything possible will be done to protect the dollar in the meantime. We have a shared interest with those who hold our dollars to keep the whole charade going.

No trolls = bubble has burst. So what do we do now?

I kinda miss the little guys.

Banker - where are ya?

When there are no trolls, or no arguments anymore that we're all just a bunch of nay-sayers, dumb-renters and pessimists, I guess that means that indeed, the bubble has burst, and indeed, we're just sliding down the hill now.

Remember the early days of this blog, when we felt like a little clique who knew something the rest of the world didn't know, and we were making our theoretical arguments (in the face of data that showed record prices and increases, and PR from the NAR and Bob Toll) that this housing miracle was just another bubble that was gonna blow?

And like Paul Revere, we felt our cause was to warn people of what was to come, before it was too late.

Sure seems like a long long time ago now. And I kind of miss it - going against the crowd, realizing something that nobody else got, arguing with the trolls. And warning people, doing good. Now it's too late.

Now everyone knows. Now we're the majority. Now there is no secret. Now the listings have exploded and prices are coming down. And now it's too late to sell.

So what do we do now? Just report on the carnage? That's not as fun as discussing this bubble in it's historical bubble context. Not as fun as predicting what would come. Now it's just reporting.

The carnage will be fascinating to watch - like driving past a bad traffic accident. You can't help but look. But it's gonna be a bit depressing.

Thoughts? Why do you all still come every day to HousingPanic? What do you want to focus on from here on out, now that theory is fact, and this bubble has blown?

HP recommended class project: Is housing in a bubble that will burst?

I'm hoping there are some teachers amongst us. Fifth grade through eighth grade, perhaps a high school home ec, economics or general business teacher out there?

If so, let us know. We'll help you craft a lesson plan or group project where you students (unbiased) can do their research on this market, historical bubbles, and current data, and come up with their conclusions.

I think it'd be fascinating for sixth graders to report on what we all know.

This baby is gonna blow. Or is blowing.

Wonder what their parents will do when Johnny brings home his report.

(oh, I was gonna put up a picture of a schoolhouse, but went with Bill 'cause he changed my life - made me want to be a polysci major at age 12. You can learn some pretty valuable things in fifth grade. I think kids after working on this project won't make the mistakes of their parents so easily. Johnny will understand the faults with no-doc, no-down negative am mortgages pretty quick, wouldn't ya say?)

February 24, 2006

Required project for all HP readers - visit this site now and add your comments

Now I've seen it all... http://thereisnohousingbubble.blogspot.com/

But then again, I know some folks who don't believe in evolution, or the big bang, or global warming, so I guess utter complete ignorance is possible to achieve in this lifetime...

This blog is spot on as they would say

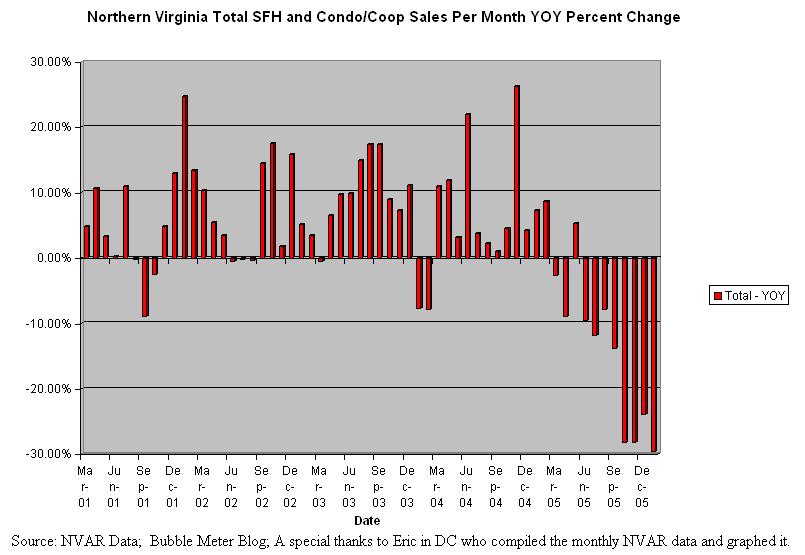

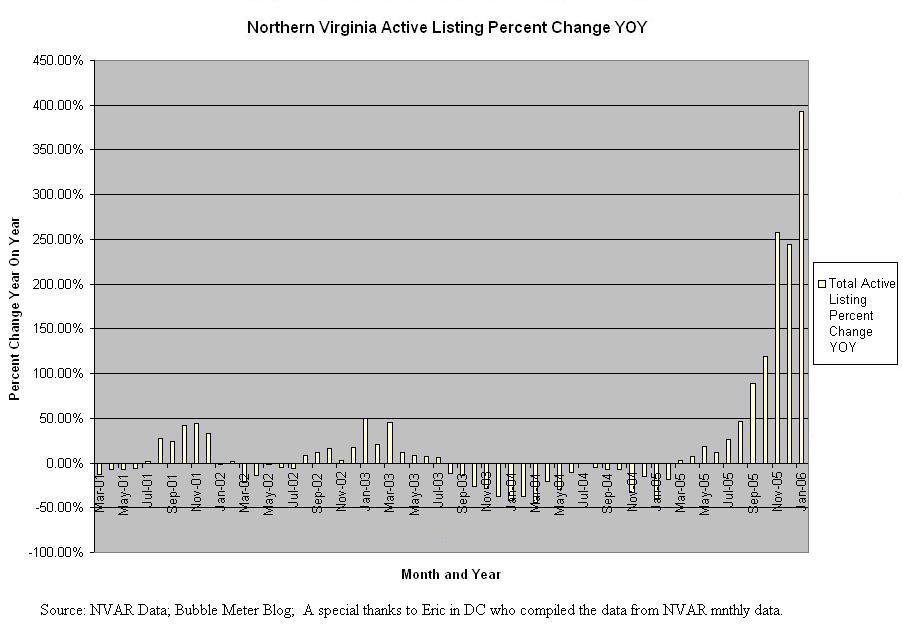

Look at these amazing numbers coming out of DC

Thanks to bubblemeter for the charts. And Eric B for these posts in Bubbletalk for pointing out these terribly amazing numbers.

I think Northern Virginia is now speeding up and closing in on Miami and Phoenix for the messiest market award:

Here's Eric's posts:

To answer the questions about seasonal effects. It is not seasonal. Generally Jan and Feb are the months with the FEWEST listings. The Northern Virginia Association of Realtors (www.nvar.com) recently released the ACTIVE LISTINGS numbers for Jan 06.

If we compare them to Jan 05 we show an increase of 392.54% for all listings.Jan 06 - 5876 up 392.54%Jan 05 - 1193 down 40.47%Jan 04 - 2004 down 41.33%Jan 03 - 3416 up 49.50%Jan 02 - 2285 down 1.42%Jan 01 - 2318 If you think that 392% up in a year is normal then have I got a condo for you!

For you all watching condos in Northern Virginia the inventory on condos/coops went up 540% YOY! see www.nvar.com for more information

Eric in DC

I just wonder what it's gonna look like when those tens of thousands of Miami condos hit the market

What do they say - adding fuel to the fire? Think of all those condos in Miami (and Phoenix, and San Diego, and DC, and Boston, and ...) that were started a couple years ago, all "purchased" by speculators, that are going to be hitting this poisoned market in just the next few months.

Oh, man, it's gonna get ugly(ier). I hope many of you went to higher ground. It's too late really to do anything - those days were last year. Now it's time to grin and bear it. It's hitting the fan right now.

Homes hit the market in record numbers

When Taffie Prince placed her Apopka home on the market last fall, she figured it would be snapped up within weeks. Four months later, she's still waiting. And the asking price has been lowered by $5,000 in the past 90 days to $154,900.

"I was told the quarter-acre of land would sell the house. But it's still for sale. I don't know what else to do," Prince, 32, said Monday. Part of the problem: The inventory of Orlando-area homes for sale has ballooned again. Suddenly, for-sale signs are everywhere.

The Orlando Regional Realtor Association reported Monday that the record 12,015 existing homes for sale in January in the core Orlando market was nearly four times the number available a year earlier.

And most of those homes hit the market in January, when members entered 6,172 homes with the Mid-Florida Regional Multiple Listing Service, compared with 2,970 in January 2005.

"It's getting a little scary," said Franco Ferrari, co-owner of Ample Realty in Orlando, the agency listing Prince's three-bedroom home.

SE Phoenix: 11,521 homes for sale: Slow SE Valley market puts listings highest in years

Ya know, starting last January (2005) or so, I started doing my own research on bubbles, manias, panics, meltdowns, etc. I owned a home in Arizona, and was thinking things were getting a bit nuts.

So I did the charts, I read my history books. I looked at days on market, the cost of renting vs. owning, the PE of housing. I looked at human behaviour during other asset bubbles. And hey, it wasn't hard, I listened to the stories from bartenders, taxi drivers, etc about flipping condos and pre-construction bonanzas. Heck, I even thought of playing that game myself - seemed soooo easy.

And I realized then that I was not only living smack dab in the middle of the biggest asset bubble in human history, that I was coincidently living IN the asset being bubbled.

So I hired a realtor, put my loft out at a ridiculous price (previous high on my floorplan was $200k a few months before, so I put it out at $340k for giggles)

And lo and behold, 12 weeks later, had a buyer.

Well, that was the top. July 2005. I tried to tell all my friends and neighbors what was happening, but most chose to ignore that advice. So I started a blog, to do what I could.

And now, folks, it can be said.

I told you so.

Here's the latest from my 'hood. This is going to end badly for Phoenix. Badly as in nuclear war bad. As in Tonya Harding bad. As in Screech from Saved by the Bell bad.

The number of single-family homes for sale in the Southeast Valley reached 11,521 last month, which, if not a record, is at least the highest number in recent years. The last time the Southeast Valley had listings in the 10,000 range was in late 2002 and early 2003, according to the Arizona Regional Multiple Listing Service Inc.

Realtors and housing analysts believe the number of listings is high because investors have begun dumping houses, home sales are usually slow in the beginning of the year and people who wanted to move held off because it was so difficult to buy another home for about a year.

And the average time on the market lengthened to 47 days, compared with four days in January 2005 and 68 in January 2004.

February 23, 2006

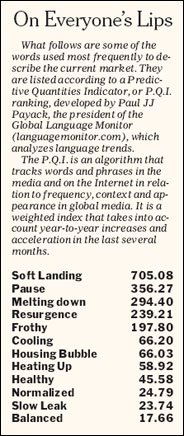

HP readers - predict the next hot buzzword to describe the meltdown (aka "soft landing"

I'm liking "meltdown" as you all know. But "panic" will be used, as well as "stampede"

Except the NAR of course. We could be down 50% and it'd still be a "healthy adjustment"

Tucson's housing sizzle now fizzling

Ever been to Tucson? What happened to this sleepy little cow town's housing market was an absolute joke. There are no jobs in Tucson folks. Except the usual suspect - people selling houses to other people.

Not anymore.

Side comment - one day I'd love the media to write a housing story and not immediately call the head of the local realtor board, or the president of the MLS. Call a freaking homeseller. Call an economist. Call someone who can speak the truth without getting fired for gods sake.

After a year of Tucsonans rushing to sell their homes to take advantage of soaring profits, it's now a buyers' market. More Tucson-area homes were on the market last month than at any time in the past nine years, new numbers show.

There were 6,499 homes listed for sale on the Tucson Association of Realtors Multiple Listing Service in January, an 87.3 percent increase over January 2005. And the number is going up fast: January's figure represents an increase of 1,042 homes over December, according to MLS statistics.

The jump in the number of homes listed even surprised Paul Olson, president of the Multiple Listing Service and owner of Vantage Point Realty.

"We knew it was going to increase, but we had no idea it was going to double," Olson said. "Sellers are getting a little more anxious."

There's no clear explanation for the jump, Olson said. Last year's real estate boom lured hundreds of new agents into the market. Individual homeowners may be trying — only too late — to cash in on a heated market.

The high inventory may be caused by investors dumping their inventory, said John Strobeck, a Tucson housing analyst who reviews sales transactions from the Pima County Recorder's Office.

So, will the Iraq civil war have any impact on consmer psyche?

Muhammed cartoons. Iran's leader preparing the world for the hidden mullah. Hamas coming into power. Syria ready to go. Venezuela's Chavez threatening to pull his oil. And a collapsing American presidency.

Muhammed cartoons. Iran's leader preparing the world for the hidden mullah. Hamas coming into power. Syria ready to go. Venezuela's Chavez threatening to pull his oil. And a collapsing American presidency.

It's go time. Blowing up this shrine will have worldwide impact. Like blowing up the Wailing Wall (and better prepare yourselves for that day)

Unfortunately folks, Bush & Co have led us down a road that of course the smart folks in the room could see before we started the trip. The dolts - "they'll greet us as liberators" crowd - didn't see it coming. Didn't read their history. Didn't understand the country, or the people. Probably the same folks who predicted a "housing bubble soft landing".

Remember, HP is not Dem or Rep. Just a realist. And to keep this in the context of this blog, bottom line - people don' t shop for houses when the world spins out of control.

Iraq took a lethal step closer to disintegration and civil war yesterday after a devastating attack on one of the country's holiest sites. The destruction of the golden-domed Shia shrine in Samarra sparked a round of bloody sectarian retaliation in which up to 60 Sunni mosques were attacked and scores of people were killed or injured

Here come the firesales. And you know who gets burned.

You know, the builders will be OK - worst case instead of 40% profit margins they'll cut it down to 0%.

It's the little guy (the guys Bob Toll was selling houses to) that'll take it in the shorts as his house is instantly devalued - and significantly devalued. Meanwhile he's extracted the "equity" to buy a new Hummer H2.

Home builder reducing prices by $60,000

First it was Centex. Then it was Lennar/US Homes. Now it's Kimball Hill Homes that's offering massive savings on new homes at Lakewood Ranch.

Jonnie Dwyer, a Kimball Hill agent, sent the following e-mail message to Realtors on Jan. 25.

"I had to share with you what's going on and I can hardly believe it myself ... All homes in Greenbrook Banks have been REDUCED! The current sales prices are as follows: Lancaster II -- $364,990, Seaside -- $369,990, Amelia -- $399,990, Hartford II -- $434,990.

That's $60,000 -- yes, SIXTY THOUSAND DOLLARS! Save an additional $25,000 toward options and $10,000 toward closing costs if you use KH Financial for your loan and Enterprise Title Co. for your closing.

February 21, 2006

Are we doomed to repeat the sorry history of the 70s?

Inflation. Check.

Oil crisis. Check.

Recession. See inverted yield curve.

Incompetent Republican leadership. Check.

This says it all

The bubble has popped, and we are in full meltdown mode

Welcome to hell Sacramento

Thanks Trex

February 20, 2006

Some wisdom in Florida: The Summer of 2005 is over and isn't coming back

Some are seeing the light. It's pretty tough not to when it's shining blindingly right in your face...

The Summer of 2005 is over and isn't coming back. This is a painful lesson for sellers trying to base their asking price on comparable sales from August."Our members are telling us that owners are beginning to back off prices 10 to 15 percent because they're not getting people pressing contracts into their hands," says Belton Jennings of the Orlando Regional Realtor Association.

Only fools predict the housing market. So here I am, once again playing the fool. Your house won't be worth any more by the end of the year.

Inventory has quadrupled in a year. That generally is an omen of price drops to come. It allows potential buyers to say: "Well, if you won't give me that price, the guy down the street says he will."This is one reason why values dropped 4 percent in December.

But if you paid $350,000 for a house three months ago and the builder now is selling the same house for $350,000 but offering $40,000 in incentives, your house is worth less.Try selling a used condo when the developer offers to pay association fees for two years on new units.When prices settle down, and finally wind up where they really belong, then the appreciation cycle will begin again -- but at a sane pace.

Question for HP readers: So say you just bought a $700,000 condo in __________

What'll it be worth in 36 months in:

A: Phoenix

B: San Diego

C: Tampa

D: Boston

E: Miami

F: Las Vegas

G: LA/OC

Here's my guesses - list yours. (Oh, enjoy the pic of the NASDAQ bubble - a reminder that bubbles do happen, and they do burst)

A: $450,000

B: $430,000

C: $480,000

D: $480,000

E: $375,000

F: #410,000

G: $490,000

Phoenix housing meltdown to take local real-estate-based economy down with it

With over 40% of the ENTIRE Phoenix economy tied to housing and home-building, guess what happens now that the bubble has burst?

With over 40% of the ENTIRE Phoenix economy tied to housing and home-building, guess what happens now that the bubble has burst?

We lost an American city earlier this year with Katrina and New Orleans. I think another American city - Phoenix - is about to lose their economy. Well, the good news is at least the illegal Mexican immigrants who build the houses will go home now.

People used to ask me what people in Phoenix did for a living. I said they sold houses to each other.

Not anymore.

Las Vegas has gambling. Detroit had the auto industry. Phoenix has housing.

A recent forecast for home building from a prestigious panel of Phoenix builders is sending shock waves through the real estate industry. At an Urban Land Institute conference in January, developer Francis Najafi of the Pivotal Group called for as few as 35,000 new homes to go up Valley-wide this year. That would be an almost 45 percent drop from 2005's record 63,000.

Stand in line with 3,600 other dolts. "Win" lottery to buy a condo. Lose your shirt. Welcome to the new reality

Boy, those developers really made people feel lucky to snag a unit, with their waiting lists, the price increases, the pre-construction parties.

Must be a pretty tough pitch though these days.

The Dot-Condo collapse is here. And it gets ugly when everyone rushes to the exits at the exact same time.

Farewell, Condo Cash-Outs

When developers in Arlington, Va., threw a party 18 months ago to showcase plans for Clarendon 1021, a condominium development that had not yet been built, 3,600 prospective buyers stood in line just for the chance to book reservations to bid on the apartments.

Now, less than a year after the building opened, speculators in this and other buildings are putting dozens of units on the market at the same time, causing asking prices and profits to slip.

Of 23 investors who sold since Clarendon 1021 opened last summer, the three most recent sellers actually lost money, after paying all fees, and average profits in the building have declined since August, said Frank Borges LLosa, owner of FranklyRealty.com.

The Great Condo Gold Rush is fading from memory and the Great Sell-Off has begun. "Money Down! Motivated Seller, Want More? Just Ask!" screamed an investor's online advertisement last week for a one-bedroom apartment in Clarendon 1021 that had never been lived in.

This is not the first time that condo markets have been influenced by investors. In the late 1980's, developers converted thousands of condo units in the Northeast and many of them were bought by speculators, said Karl E. Case, an economist at Wellesley College. Many of those investors, he said, ended up losing money when they sold in the early 1990's. "It was ugly," he said.

February 19, 2006

Selling underwater has got to suck

But, I guess a $20,000 loss is a LOT better than a $200,000 loss. Even Cramer says sell your losers. It's just tougher when you live in your loser. Oh, watch for companies who'll be preying on these near-foreclosure situations (like "We Buy Ugly Houses" and this dolt pictured here...)

Rise In Short Sales Indicates Troubled Housing Market

More Cases Being Seen Where Sellers Must Bring Money To Table

CLEVELAND -- A lot of people rely on the value of their house to bail them out of some circumstances, such as losing a job, going through a divorce or suddenly taking ill.

However, a tough economy and a flat real estate market may leave you short when the deal is done. People are selling their homes for less than they owe, and in some cases, for less than they are worth.

"We are seeing a lot of people having to bring money to the table. They are doing it, they make the sale happen, but they walk away with nothing," said White.

Even mortgage banker Thom Rankin is closing short sales, which just a few years ago were considered rare.

"It concerns me that we are now seeing this happening, and I have been doing this for 30 years, and I have never seen short sales come as readily as these did," said Rankin.

Short sales indicate trouble with the economy and housing market, because people sell short to unload property they can no longer afford, or to avoid foreclosure.

Nobody keeps statistics on how many short sales close each month, but lenders and Realtors say they are increasing at an alarming rate.

Forty-three percent of homebuyers last year put no money down on their houses. That means they have little to no equity if they have to sell short, or worse.

HP reporting from Tampa Florida this weekend. One word: Hellhole

Just here for a few days for a conference. Trust me, this city would be far far down on my list of places to visit. Strip malls. Horrible zoning. Obese Americans. Chain restaurants. And yes, REALLY expensive condos ("from the low 600's!")

Read the paper today and lots of ads for condos with the same stock-art photography I used to see in Phoenix. Does anyone really believe that hot 20 year olds are buying these $900,000 condos - where they drink martinis or wine with their other hot 20 year old friends out on the porch? Then get dressed up in their black dresses and tuxes for a night out on the town?

My shuttle driver spent the 30 minutes to the hotel talking about the killing he was going to make in real estate here. He just got his bankruptcy done a year ago and he found a bank to get him a no-doc no-down loan on a $200,000 house here (at 8%). He said he's up at least $50k already, and wants to sell that one to put the money into some land.

Yup, the shuttle driver. Figure that pays about $8 an hour.

I didn't want to break the little guy's heart. He's screwed. And this was (another) shoe-shine-guy kinda moment. When the shuttle guy is flipping homes, RUN!

Then don't get me started on the hurricanes, and the humidity, and the bugs, and the lack of "there" there. Heck, even the beach was nasty.

Anyone else from the Tampa area want to comment on this market? Sure felt a bit like Phoenix.

February 18, 2006

Follow the vacancies... Good God, this is such obvious stuff

Rental Vacancies peaked at 8.1% in Q3 1987. Homeowner Vacancies peaked at 1.9% in Q3 1989. There was a huge stock market crash in 1987 but the economy didn't slow dramatically until the 1990 to 1992 period when the housing market slowed nationally.

Fast forward to the present situation. Rental Vacancies peaked at 10.4% in Q1 2004. Homeowner Vacancies set a record high of 2.0% in Q4 2005.There are many reasons to fear an even greater economic slowdown starting in 2006 based on a more dramatic rise in home prices and extreme private and national debt levels.

Vacancy data can be found here.

From Q4 2004 to Q5 2004 the number of vacant homes increased by 427,000, with vacant for sale up 191,000 and seasonal vacancies up 245,000.

With speculation by property flippers, vacation home buyers, and retirement home buyers driving demand for new homes, it is not surprising that the nation produced far more homes than were needed for habitation in 2005. All this is leading to a supply glut that finally is impacting prices. Median prices for new home sales were down 8.39% from September to December

It isn't surprising that if you build a house where there is already overcapacity you might have a hard time selling it.

NAR estimated inventory of 2,796,000 existing homes for sale, or a 5.1-month supply in December, which is up by 582,000 (26.3%) year over year. Distressed borrowers will have a very hard time unloading their homes in a hurry if they decide they can no longer afford high mortgage payments.

February 17, 2006

New Condos Are Everywhere And Their Prices Are Soaring. So, Who's Buying Them?

I can't for the life of me figure out how stupid someone would have to be to be buying a condo today - to live in, to rent, or to "invest". Anyone care to help HP figure this one out?

I can't for the life of me figure out how stupid someone would have to be to be buying a condo today - to live in, to rent, or to "invest". Anyone care to help HP figure this one out?

The question pops up all the time, just like the high-end condos that keep popping up near Metro stations across the Washington area: Who's buying all these expensive apartments?

Ballston resident Sonia Schmitt thinks she knows. A World Bank employee who has moved up to ever-bigger condos five times in the past nine years, Schmitt says it's a combination of buyer types.

She sees mid-thirties singles trading up from smaller condos and empty-nesters downsizing from bigger homes -- or even smallish homes that have appreciated so much that they can afford a $400,000-plus condo. More frequently, as prices jump ever higher, she sees buyer couples -- either married, cohabitating, same-sex or just acquaintances who are partnering simply to "get in the home-buying game." Most of them, she says, already live in the Washington area.

There is another big group that sometimes gets overlooked -- investors. According to a recent study by research firm Delta Associates, "investors represent 30 to 35 percent of the condo market" in the Washington area, chief executive Gregory H. Leisch said. That's higher than in all other condo markets in the nation except South Florida, Leisch said.

Investors represent about 25 percent of condo sales in San Francisco and New York and about 20 percent in Chicago, he said.

Leisch said two-thirds of Washington investors are in it for "the short term," to "flip" or assign the contract to another buyer before they sign, or to resell the unit soon after settlement, which is about 18 months after the original contract. Both maneuvers would let the original buyer get in on the huge price gains condos are showing, gains that can start when the building has been on the market for only a few weeks.

US 1929. Japan 1991. China 2006? Will the Chinese bubble economy collapse under it's own weight?

If it does, it brings the world down with it... Plus, does anyone trust communists to run a capitalist economy? Feels like trusting religious zealots with our own financial system (oh, wait, we're doing just that!)

Could China's red-hot economy collapse?

Fifteen years have passed since the collapse of Japan's asset-inflated economy.

Finally, though, structural reforms to overhaul the political, economic and social systems have begun to take effect and the economy is showing signs of recovery.

The crash of the Japanese economy in 1991 was triggered by sudden drops in land and stock prices. Six years later, in July 1997, similar bubbles popped throughout East Asia, setting off a regional financial crisis.

The Chinese economy has been steaming ahead for several years, fueled mainly by a construction boom and rapid growth in the auto industry. A lot of momentum is also coming from strong exports (especially to the United States) and two big upcoming national events: the 2008 Olympics in Beijing and the world exposition in Shanghai in 2010.

Observers have been warning for some time about the overheating of investment in the construction and auto sectors. Many point out that Chinese industry is awash in excess capacity, causing a large output gap between actual and potential production.

The current building boom is also troubling. Rare is the vacant lot in Beijing where a new building is not being put up.

In Shanghai, there are mounting concerns about land subsidence, stemming from a growing forest of high-rise buildings and excessive exploitation of underground water.

Assuming that the monthly pay of professors at Beijing or Tsinghua University is about 4,000 yuan, the 38-million yuan price of the average house in this district is equivalent to 800 years' worth of salary.

The Chinese government has been trying hard to curb the expansion of its own bubble economy, one driven by excessive capital investment and industrial production. The government has instituted restrictions on lending by banks and other financial institutions. It has also started taking steps to stem the rise of property prices.

So many of these debt debt debt stories, how can HP keep up?

I may have to outsource HP to India. Just can't keep up with all the sad stories...

A Warning for Condo SpeculatorsChicago Sun Times ^ 2/16/2005 Terry Savage

Posted on 02/16/2006 11:12:27 AM PST by ex-Texan

Q: My husband and I were on a great path to being financially stable. We both started saving for retirement early on, we both have great credit and we have always tried to live within our means and save for a rainy day.

Before we were married, we purchased a condo in the loop. After we were married for a year, we decided to buy a second condo for investment purposes -- and this is where the trouble starts. We used $20,000 that we had saved -- for a rainy day -- and took a second mortgage on our unit for $20,000 to make up our down payment for condo number two. The real estate developer was offering one full year of mortgage, assessments and taxes as an incentive to buy -- not to mention the unit was rented.

We thought this was a win/win situation. We would have two years minimum of no out of pocket costs, and at the end of that period or even before we can put the unit on the market and sell. We figured even if the value only increased by $5,000 it was still a good thing.

When we applied for a mortgage, the lender informed us that our credit score was good enough that they were going to approve us for a no doc loan. I now think this was a red flag for us to realize "this means you really can't afford this loan, but we're going to give it to you anyway."

Well, here we are two years later, and I fear of what is to come. We put the unit on the market in April 2005 with no luck thus far. We first started the price out high, but by the summer we had came down to our exact purchase price.

In November 2005, the tenants' lease was over, so they left. Now we are in the last stage of the two-year period with no out of pocket costs. We are hopeful that we will get a tenant in the spring, but the rent does not cover all of the costs of owning the unit. We pay our current bills no problem, but once we have to start covering the costs of our second condo on our own, there is going to be no way.

I know the bank will want us to blow off our current debt and pay them first. We've worked so hard to keep our credit scores looking A+, and now I'm afraid of what is going to happen.

I know you can't tell us what to do, but can you advise me on how to handle this? Should I start talking to attorneys or debt consolidators? I just want to be pro-active in taking care of this costly mistake.

A: I hope you don't mind that I'm going to print your letter -- with no names, of course -- because for sure you're not the only ones in this situation. About two years ago the speculative condo boom was at its peak. And now many speculators are about to find out that it doesn't take a "crash" or "breaking the bubble" to create your own personal speculative crisis. All it takes is being unable to cover the carrying costs.

NFL? MLB? Nah - new US sport is "WFGS" - or "watch flippers get screwed"

Oh, boy, there's gonna be so many of these stories the next couple of years. Dot-condo nightmares...

Check out this underwater flipper from "aren't we supposed to be still booming" Las Vegas (thanks to bubbletracking):

Flipper in Trouble (update)

Originally Posted 1/4/06Update I 1/18/06Update II 2/15/06No, this is not an EF (Extreme Flipper).

This is just a run-of-the-mill flipper with 4 properties, 2 of which are listed on the MLS below. I'll assume one of the other two is the principle residence and the other is rented. Check out the listing description...6xx9 SWEET PECAN STLas Vegas - Lone Mountain, NV 89149Listing Date: 1/4/06Listing Price: $295,000Last Sales Date: 11/2004Last Sales Price: $305,000"This home is being sold short and we will entertain all qualified offers, this offer will need to be acceptable to the lender. Make us an offer???????"

(Update 1/18/06: first reduced to $290,000, now the price is back up to $318,000... which proves the motto: if you can't sell it, raise the price!!!)(Update 2/15/06: no longer on the MLS, however, we do see it as a pre-foreclosure on RealtyTrac. Check out the pure stupidity: our flipper in trouble purchased this gem for $305,000, guess how much the prior owner bought it for? $190,000 in 7/2004!!! This is a good example of a flipper screwing another flipper for a $100,000 profit in 4 month!)

February 16, 2006

Now Phoenix sellers are praying to St. Joseph (and it's too late)

I've sold three houses in Phoenix over the past 10 years. All took over six months to sell. All had hardly any traffic and no offers. Then I did the St. Joseph trick (kudos to Mom). And within a week, an offer.

But, shows you what a crappy real estate town Phoenix was until the speculator craziness in 2005. Those days are over, never to be seen again. But trust me, wanna make some money, get into the St. Joseph statuette market now!

The couple got caught in the abrupt market swing that has drastically increased the number of houses for sale in metropolitan Phoenix. They've reduced the price twice - it now stands at $449,000 - yet there were no takers. So they resorted to an old home-selling trick that's supposed to bring luck: burying a statue of St. Joseph upside down by the For Sale sign in their yard.

"The four of us, we held hands, and my wife said a prayer to St. Joseph to put us in escrow," Andre Bilyk said. "We were having an open house the next day. You gotta do what you gotta do."

Listings are up and houses are taking more time to sell as buyers regain the upper hand in the Valley's volatile resale market. Six months ago, the Bilyks would have sold their house in a couple of days, if not a few hours. Now, the house is waiting for a buyer and competing with more new listings every day as suddenly picky shoppers browse the market and haggle more on price.

The number of houses for sale in metro Phoenix has nearly tripled in the past year, based on December data from the Arizona Regional Multiple Listing Service.

I'm depressed

Nobody's bought the new Barry Manilow album off of HousingPanic's link... I thought my readers had class, had style, had taste, had boo koo housing loot to spend on impulse purchases...

Why, God, do I try so hard? Why?

Oops - our bad. There is no housing bubble.

Oh, boy, this one's hilarious. My favorite blogger btw...

Since we were all wrong, let's all run out and get $0 down, neg-am, no-doc, interest only's and buy up every stucco hellhole in Phoenix. Party on!

No Bubble, My Bad :-(

Bay Area Bubble Bloggers Admit Defeat, Throw in the Towel

Copyright © 2006 Realty Times®. All Rights Reserved.

by Leslie Appleton-Young and David Lereah

The housing bubble blogosphere today was reeling from a shocking announcement made by an obscure but popular Bay Area Housing bubble blog, Patrick.net. The blog’s overall tone is as bearish as any on the web (”SF Bay Area Housing Crash Continues” staunchly declares the site’s link page).

Evidently, the site’s main contributors have completely reversed course and now claim there is no housing bubble. “After so many months of denying the obvious, we had no choice but to call it quits and Face Reality,” says Peter P, one of the blog’s earliest threadmasters. “Agreed,” says HARM, “it’s painfully clear that we were dead wrong and housing is going to keep appreciating 15% a year forever, just like Gary Watts says it will.”

It's interesting to watch how people price during this meltdown

It's human nature to expect, or "deserve" to get what your neighbor got just a few months ago. Pricing your home at $x just because home Y got $y 6 months ago is irrelevant. It's what the market will bear today. Good god this is basic stuff, isn't it? Isn't it?

Talk to folks who would've loved to sell their Pets.com at $500 a share when it was trading at $5, just because they bought it for $500 or that it was "worth" $500 at one time.

Interesting article from Florida on falling prices, and a tale of two homeowners:

Homeowner #1 (the ignorant one):

Jeanne Dobus of Indian Harbour Beach, who put her home on the market in October, said she has been disappointed so far in the response -- which has been slow.

"I've never seen such a glut of homes for sale in this area," Dobus said, noting the asking price of her four-bedroom home is $349,000.

"People are offering $250,000 to $260,000," Dobus said. "That's just not the right price."

Homeowner #2 (the realistic one):

Kathy Smith had a much-easier time selling her Port St. John home -- asking price $89,900.

Smith, who moved to Fort Pierce, put up a sign in her yard Friday, and had it sold that afternoon.

"It's because of the price," Smith said. "We probably could have asked for more, but we needed to move quickly."

"Slowdown?" I don't think so. This is more accurate: "It's looking more likely ... that we're going to get a sharp contraction,"

I still find it humourous when the "experts" in the face of data, hoping against hope, predict "soft landings" and "slowdown, not a burst".

Right.

"Sharp contraction" is more like it. And memo to NAR: It's already underway.

Home price surge may be leveling off

David Lereah, the NAR's chief economist, cautioned that the market is rapidly cooling

I don't want to say this is the last hurrah, but it certainly reflects the peak of the boom in terms of price appreciation," Lereah said. "It wasn't the highest quarter for price appreciation ... but it covered a big part of the country — 72 metros is enormous." Sales of existing homes are falling faster than Lereah had expected. Price appreciation could slow to single digits this quarter and will reach only 5% for the year, he predicts.

Mortgage applications last week slid 7.3%, on a seasonally adjusted basis, to the lowest in two years, the Mortgage Bankers Association said, lending support to market pessimists.

"It's looking more likely ... that we're going to get a sharp contraction," says Ian Shepherdson, chief U.S. economist at High Frequency Economics.

B&Q (the Home Depot of the UK) Sales fall again - quarter sales down 9%

Once the bubble pops and appreciation is a thing of the past (as it is here in the UK), home renovation dries up real fast. Why put $$$ (or £££) into a place that you know won't get a return on investment?

B&Q is getting hammered. And Home Depot will be too. I know some builders in Phoenix get all of the supplies for building a home at Home Depot (wood, etc) so it's not just improvement but actual home building too that'll kill HD

LONDON (Reuters) - Kingfisher, Europe's largest home improvement retailer, saw no let-up in the recent poor performance of its B&Q chain during the fourth quarter, the company said on Thursday.

For the 13 weeks to January 28, like-for-like sales at B&Q fell 9 percent compared with an 8.4 percent drop in the third quarter and a 7 percent drop in the first half.

Analysts were expecting a decline of 7 to 9 percent and are not anticipating a recovery at B&Q until well into the 2006/7 financial year.

"The UK home improvement market remains depressed and price competitive," said Chief Executive Gerry Murphy.

The DIY sector has been struggling to boost sales in a weak housing market and Kingfisher is suffering after opening too many big stores during the market's boom years.

{kind=link}

{kind=link}