Every now and then I like to read about past financial bubbles in human history - always puts the current one into such sharp focus, as every criteria is met, behavior is the same, and yes, they all end the same too. It's never different this time.

Every now and then I like to read about past financial bubbles in human history - always puts the current one into such sharp focus, as every criteria is met, behavior is the same, and yes, they all end the same too. It's never different this time.

Well, I'll take that back. This bubble is the biggest in human history, thus different in scale but not structure, mainly because of the incredible amount of leverage and debt (margin) used via mortgages, and also the participation rate.

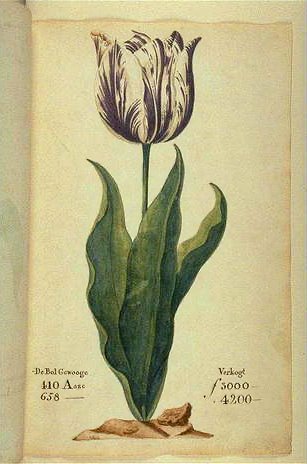

From the tulip bubble, I enjoyed this 'Dialogue between Waermondt and Gaergoedt on the Rise and Decline of Flora (1637)' via U of Chicago.

400 years later, how many others felt "why should I work for a living, or invest rationally, when I can just earn tax-free crazy money in housing and do nothing?". Well, a generation will now see the answer to that question. Hopefully the stench is so bad it ensures we won't see this stupidy for another 400 years.

Waermondt (True Mouth): You offer me a lot and I do not know whether I dare accept. I fear once I start, I will want to go on with it, again and again. And as one wave drives on another, so one deal would bring forth the other, and so, methinks, it is better I stay with my poor business and my own profession. I make no great profit and suffer no great loss.

Gaergoedt (Greedy Goods): That's well said. But could you not venture a little? You give no money till it's summer and then you have sold all your stuff; or if you have any on hand you plant it and it brings still more profit.

Waermondt: It is well for those who have enough money, but for me I do not find it good advice. For if I have a penny, I must put it into my business.

Gaergoedt: You can barely earn ten per cent on the money that is in your business, and even then only by giving a caution, but with Flora it is cent for cent. Yes, ten for one, a hundred for one, and sometimes a thousand.

Waermondt: Vainly have I done such hard labor, and have many parents slaved and toiled. What need is there for merchants to have any style, or to risk their goods overseas, for the children to learn a trade, for the peasants to sow and to work so hard on the soil, for the skipper to sail on the terrible and dangerous seas, for the solider to risk his life for so little gain, if one can make profits of this sort?

August 08, 2006

Ah, the lesson of tulips

![]()

![]()

Subscribe to:

Post Comments (Atom)

11 comments:

What an interesting posting! Loved the flora conversation.

How come you don't come out and plainly state why this bubble bothers you so much? Is it a disgust with greed? A dislike of get-rich-quick schemes?

Just curious.

Ironically, houses on Herengracht (where a house was famously traded for a tulip bulb) has returned 0.2% PA after stripping out inflation.

Of course, the numbers are only based upon 350 years of recorded data and it is different this time.

If one is to believe the UK press, the current prices are to double by 2010 raising the current price/income ratio of over 6X to something like 12X.

Which would then require 100% of the average buyers income for debt servicing. Which is OK if you don't think they should pay tax, buy food or clothe themselves.

No - the real nub of the debate is why people are so innumerate that they actually believe housing is a can't-lose, throw-out-the-fundamentals, double digit 'investment'.

Cheers, Haggis

While the Federal Reserve and most Wall Street economists continue to predict a soft landing scenario in housing, the increasingly worrisome economic data tell another story. In fact, if one were to compare shopping for a house today with shopping for a house in January, one would see some noticeable differences.

Are you worried about having someone outbid you? Don't worry. Houses are on the market a lot longer (approximately 6 months) and inventory is at a multi-year high. The National Association of Realtors reported this past week that the number of homes for sale is at their highest point since 1997. The Commerce Department also reported today that new home sales dropped by 3% last month.

Is your Real Estate agent telling you that you better buy now before prices go even higher? Don't believe it. Housing prices have already started their decline. Take a look at the recent decline in San Diego County Media Home Prices.

The sharp decline over the last couple of months does not look anything like a soft landing scenario.

Did you plan on paying for your closing costs? No need. Sellers are paying for closing costs and even offering new washer and dryers to boot! Home builders are even offering incentives for upgrades and even leases on luxury cars.

It is clear to me that we are well on our way towards the housing burst that I predicted in January. Anecdotes about housing incentives will only multiply; supply of homes on the markets will increase, and prices will continue falling.

Foreclosures

According to Foreclosure.com, foreclosures are up 2.6% throughout the country. While this number does not seem staggering, it does reaffirm a change in the trend. In fact, some areas of the country are already showing a dramatic increase in foreclosures. In Dallas, for example, foreclosure rates are up 26%. As interest rates continue rising and the overextended homeowner is faced with the reality of higher mortgage payments, I expect that we will see these numbers exponentially rise.

Going Forward

At the center of the housing burst, is the continual and inevitable rise in interest rates. While most Wall Street economists firmly believe that the interest rate hike is over, I contend that this outlook is undeniably shortsighted. In fact, most of these economists that are predicting a pause or a stop in rates have had this outlook for the last several rate hikes. Generally speaking, their argument is centered on the fact that they feel that inflation is not a problem.

Inflation, however, is a problem. Over the last several years we have seen the price of oil triple and raw material costs reach multiyear highs. While manufacturers and producers have been eating up these costs for the last several years, this trend is not likely to continue. In fact, we are already starting to see companies pass through the high energy costs to the consumers. Companies like FedEx have raised their prices due to higher energy costs. Even some restaurants are beginning to pass through the higher transportation costs to the consumer. The end result of the pass through of costs is a higher core CPI number.

The significance of higher core inflation is that the Fed will finally be forced to acknowledge inflation. Ben Bernanke has clearly stated that they will rely on data to determine their actions. Rising inflation would force the Fed to continue moving rates higher. The last several months have resulted in higher than anticipated core CPI numbers. In March, the core CPI jumped up 0.3%. Wall Street economists had expected a 0.2% increase. In April, the core CPI jumped up another 0.3%. This number again came in above Wall Street expectations of 0.2%. May once again showed another 0.3% increase in the core CPI numbers. Not surprisingly, Wall Street had expected an increase of .2%. Finally, the June CPI numbers also came in at a 0.3% increase, higher than the expected 0.2% increase. The Fed continues to argue that inflation is contained, yet I believe that the cat is already out of the bag. Going forward, I expect further spikes in the core CPI numbers to translate into higher interest rates.

The rising interest rate environment will have a negative impact on homeowners who have interest only or adjustable rate mortgages. In the next 18 months, there will be approximately 2 trillion dollars worth of adjustable rate mortgages that will have to adjust to a fixed rate. Overextended homeowners who were paying a certain amount on their mortgage will be forced to pay a higher rate. Unfortunately, a good number of these homeowners do not have the means (see negative savings article) to afford the higher mortgage payments. With rising interest rates, we will see a rise in foreclosures, which lead to additional supply of homes on the market. The additional homes on the markets coupled with slowing demand will translate into a continued burst in the Real Estate Market.

Recession

Recessionary concerns have also intensified over the last six months. Whereas several months ago few people were arguing the recession scenario, there are now more people that are at least acknowledging a slight probability of an upcoming recession. In truth, there is more than just a slight probability of an upcoming recession. If you subscribe to a burst (or even slowdown) in housing, you should expect a recession to unfold.

As real estate prices have climbed in the last several years, we have seen consumer spending go through the roof. In turn, this has led to strong corporate profits and a false sense that we have a strong economy. However, borrowed money does not translate into a strong economy. It only translates into an eventual recession. Take a look at the below chart. It tracks consumer spending versus housing.

As you can see when housing slows, the consumer stops spending. Of course, this makes sense. Consumers will no longer be able to tap into their home equity and withdraw cash for frivolous expenditures. In addition, those that will be able to remain in their homes will be forced to pay more on their home mortgage. It is important to note, that if we were a manufacturing economy, this would not hold as great of significance. However, we are a consumer led economy. As a result, a slowdown in consumer spending will be put a screeching halt to this pseudo-economic growth we have experienced in the last several years.

A housing burst will also contribute to a higher unemployment rate. While it is true that the current unemployment rate is pretty low, I do not expect this trend to continue.

Mortgage companies, real estate firms, construction companies, and other real estate driven industries will be forced to lay off workers as the real estate bubble comes to an end. Additionally, industries that rely heavily on discretionary consumer spending will also lay off workers. Already, we are starting to see signs of a slowdown in consumer confidence and spending.

Are We Watching Re-runs of That 70's Show?

While the upcoming real estate and economic outlooks are far from rosy, you can position yourself to weather out this storm. Fortunately, we can look at the past as a point of reference of what might happen in the future. During the 1970's, Americans experienced high inflation, a recession, and rising interest rates. Sound familiar? The 1970's also provided investors with an opportunity to profit in commodity markets.

Gold, for example, moved up 19.5 times in value. At the end of 1971, Gold prices were trading at just about $43/ounce. Before the bull market was over, Gold prices had reached a high of $850 an ounce. In comparison, the present bull market in gold has only appreciated 2.5 times in value. Although there were some 1970-specific factors (such as the end of the gold standard and the oil embargo) that are absent from today's market, the main factors that were present during the 1970's are clearly present today. One can also argue that there could potentially be a greater demand for gold during this bull market. Population growth and wealth creation in Asia, central bank buying, and a declining interest in fiat currencies are just a few reasons why this could be the case.

Besides gold, there were other commodities that experienced appreciation during the 1970's. Sugar went up 9 times in value. Coffee went up approximately 6 times in value. All in all, commodities were in a bull market.

At the present, there is speculation that a rising rate environment could put an end to rising commodity markets. Some pundits argue that higher interest rates will slow down economies, which will in turn slowdown demand for commodities. This logic, however, is flawed. First, we have had 17 consecutive rate hikes. During the rate hikes we have seen commodity prices continue to soar. Second, the 1970's clearly showed us that commodity prices can still rise as interest rates rise.

I grew up in Texas in the 80's. The tulip story reminds me when there was a similar (obviously smaller) bubble in the sale of Emus and Emu eggs when I was a kid. It started with people talking about how Emu meat could replace beef. People started raising Emus and selling their eggs to each other for more and more money. Nobody actually sold an Emu for its meat, people only sold the eggs and chicks to each other hoping to get rich from Emu ranching. In a couple of years, tons of people had Emus. In the end, lots of people lost money and many Emus were put down or left starving. I haven't seen an Emu since then.

Ah yes, the Emu. What a ponzi scheme that was. There are 2 places around here that have (had?) Emus. I will check and see if they still do.

I have never seen Emu in the meat section at the market.

I saw emu farms in colorado in the early 90s. asked some people about them and same story - said they were making a killing in emu meat

oopsie.

Emu oil will replace fossil fuels by 2010. You can easily grow them in your backyard, they fertilize while eating snails and bugs, plus they make a plesant sound as you "juice" them for their light sweet crude.

Sure.

The US uses 300 billion gallons of oil, 1 billion tons of coal, and 22 trillion cubic feet of natural gas. Per year.

Alot of emus, wouldn't you say?

I used to live in the Netherlands and always love the spring time there. If you want to see beautiful tulip fields of every color imagineable, travel to Noord-Holland, Netherlands in mid April, early May. While you're visiting the Netherlands make sure you visit Keukenhof: http://www.keukenhof.nl/

Tulip mania reached $76K (in today's dollar) for a single tulip.

Doesn't that sound like the trailer homes in Malibu (sans land) going for over a million?

http://www.usatoday.com/money/perfi/housing/2005-07-05-million-dollar-trailers_x.htm

No, you can't live in a tulip, it won't protect you from th elements, it is larger, tulips can rot in the ground.

Post a Comment