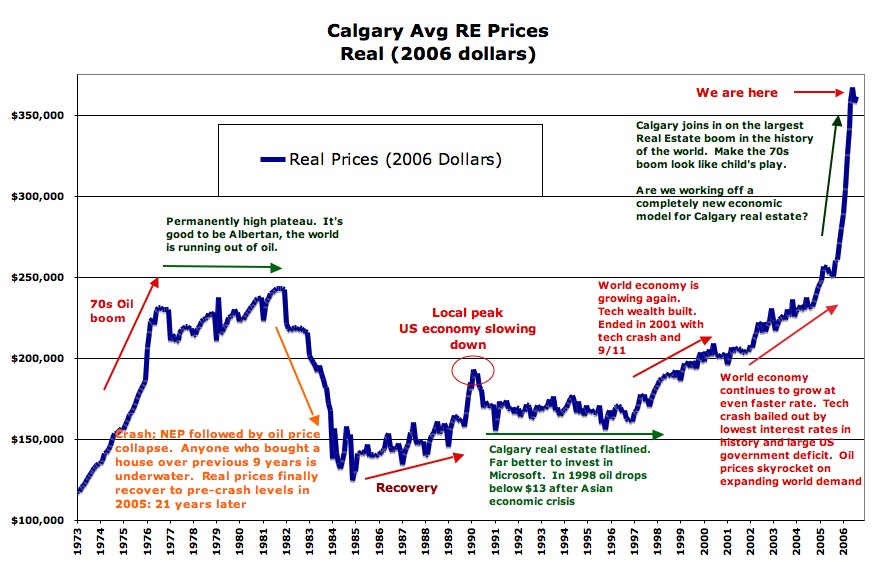

Sure, we've still got some corrupt fools out there cheerleading, or saying we'll get right back to party-on in just a couple of months (Lereah, Appleton-Young, the corrupt idiot at Harvard, Bernanke, etc).

But you can't hide from reality, and the reality is that the greatest Ponzi scheme of all time is over, only an ignorant fool would be out buying a home today, and prices will now drop right back to (or below) the historic mean.

Here's the view from LA, of a meltdown that has now spread nationwide, soon to be worldwide.

So I guess it's official: The real estate market is tanking. On Monday, the National Assn. of Realtors reported that, for the first time in a decade, the average price of a U.S. home actually declined. In California, sales of existing homes in August were down 30.1% from August 2005, which is the steepest year-over-year drop in almost 25 years.

But like children, houses are highly efficient delivery systems for denial. Just as no parent would admit that his or her offspring — no matter how costly, ill-behaved or intimately acquainted with the juvenile justice system — is anything other than a source of unmitigated joy, people who own their homes will tell you that the market is just fine. Best to listen to National Assn. of Realtors chief economist David Lereah, who said in a quote in this paper Monday: "This is the price correction we've been expecting — with sales stabilizing, we should go back to positive price growth early next year."

Hey, great! Problem is, that same article also quoted another economist who said that "the speed of the collapse has been astonishing" and predicted "no chance of any short-term relief." Translation: If you're a renter, you now have permission to be as self-satisfied as the homeowners who once taunted you with their dizzying appreciation rates. As for us owners, we can just cover our ears and sing "Correction! Correction! I can't hear you!" until things start looking up again.

Call it a correction or call it a crash. Either way, the party's over.

September 30, 2006

It's getting a bit surreal, reporting on the housing devastation underway. Who'd of thunk it'd happen so fast?

FLASH: Motley Fool picks up HP's fatwa against Nicolas P. Retsinas, the corrupt director of Harvard's Joint Center for Housing Studies

This, HP'ers, is our finest hour. Motley Fool has picked up our post from Wednesday, HousingPanic calls for the immediate firing of Nicolas Retsinas, Director of the Joint Center for Housing Studies at Harvard University

HP I believe is doing good work. The HP community (and eyes and ears) is having an impact. David (HP and the bubble blogs) can beat Goliath (the evil and corrupt REIC).

And maybe one day this madness will end, and houses will again be places people live in, and young kids out of college can save 10% down and get a 30-year fixed mortgage, a house they can enjoy, appreciation at the rate of inflation, and a payment they can live with.

Cheers to all of you. And please email this post to Harvard's President Derrick Bok (derek_bok@harvard.edu).

Here's Seth's article. Big hat-tip for picking up the ball and running with it.

More "impartial" commentary on the housing bubble I owe another hat-tip to my buddies at the Housing Panic Blog. These folks are even more up in arms about the funny doin's transpiring in the real-estate industry than I am, and I don't share all their views, but I do think they've got an interesting point today. Let's set the stage.

Harvard. Ivy League, home to Biff, Buffy, and Chet. Warm scarves and deep thoughts. A place where we can trust the research as the work of independent-minded eggheads, right?

I wouldn't be so sure. Today, we see a strange article by one Nicolas P. Retsinas, director of Harvard's Joint Center for Housing Studies (JCHS). In it, he seeks to reassure a nervous and gullible public that all is well with housing. Prices won't drop too much, he claims, and the overall economy is not at risk.

Oh, really? Oddly enough, he doesn't cite any data to support these contentions. Well, maybe that's not so odd. Recent numbers from no less a home-selling partisan than the National Association of Realtors (NAR) show that prices are already dropping, not only in bubble-afflicted coastal areas, but in the previously believed-to-be-safe Midwest, as well.

But Retsinas shrugs past this. "Demand," he claims, was the reason for rising prices, and demand, he says, is still here.

Demand doesn't exist in a vacuum. Let me be blunt. I find this is a stupid argument. Dangerously, irresponsibly stupid.

Why would he pump out to the press a defense of the bubble without a single, salient data point to back it up? What's the motive?

I think the answer might be found in the cozy relationship between Harvard's JCHS and the home-building, -selling, and -supply industry.

I've got a message into Harvard to find out just how much dough is changing hands here. If it's much more than a pittance, I consider that an interesting -- and by interesting, I mean scandalous -- conflict of interest.

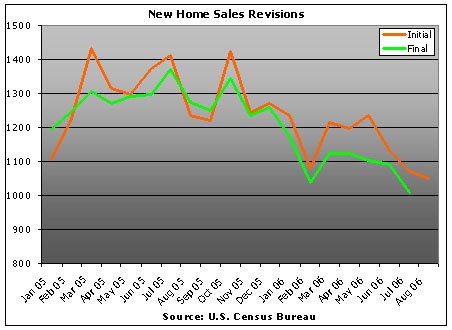

If you knew your number was wrong and overstated every month, wouldn't you try to fix it?

You know that new homes sales report that we mock every month, where they report houses sold and then revise the number downward every month? Here's how it looks charted - thanks to Mish

* Report the number - check

* US media run with it as fact - check

* Fool Americans into thinking it's not as bad as it is - check

* Revise to correct number - check

* MSM doesn't report the correction - check

* American's remain clueless as to what's really going on - check

* Let out a diabolical laugh - ba ha ha ha, bah ha haha - check

Ah, the financial stupidity of home sellers: Thinking their price has anything to do with what they paid or what they need

This widespread problem, where sellers think they "deserve" a price because that's what a neighbor got last year, or that they're at their "rock-bottom" price because that's their break-even number, well, got some bad news.

Pricing is a function of what the market will bear at any given time folks. Not what you "deserve", not what you "need to get". Here's a report from in-full-meltdown-mode Chicago:

It's pretty amazing how fast the reversal has occurred since last year," said David Stiff, chief economist at Fiserv CSW, a property-data analysis firm in Boston."There has never been such a quick deceleration in price appreciation," Stiff said. "I was looking at data from 1969 forward, and it's unprecedented."

Not so, said Tommy Gentile, who has been trying to sell his five-bedroom home in west suburban Montgomery for about six months. He has reduced the price by $20,000, to about $380,000, leaving little wiggle room.

"That price is pretty close to rock-bottom, as far as money we've put into it," he said of the house, bought two years ago. "We have to get our money back because we've bought another house, and we're remodeling that one. We have two mortgages.

"Few people are coming to take a look" Gentile said. Between competition from home builders offering incentives to close out developments and about 10 neighbors who also have their homes for sale, it's a struggle to attract interest.

Now they're starting to get it over here - Telegraph UK: US housing crash could bring UK down with it

Not sure what took 'em so long, but the UKMSM is now putting the pieces together. Next step is for the housing-ponzi-scheme-obsessed-real-estate-never-goes-down UK "investor" crowd to get it too. That subtle change in psychology where doubt and then fear enters their minds, and the realisation that they need to 1) stop investing and 2) get out at the peak.

My 1-bedroom London flat would list for $1.2 million. I'd say it's fair value is around $350,000. You know the drill.

Here's the Telegraph article, a good first step, but the writer still doesn't understand it's not just the slowing economy that'll crush the UK - it's the end of the UK housing ponzi scheme, bigger than the US bubble, combined with the slowing economy, that'll bring the country to its knees.

If you'd like to help the author get it, you can contact him here (edmund.conway@telegraph.co.uk)

US housing crash could bring UK down with it

By Edmund Conway, Economics Editor

Peter Warburton, who runs a small consultancy called Economic Perspectives, believes that the UK will slump into a full-blown recession next year, shrinking by some 0.3pc over the 12 months. This would be the worst economic performance since 1991, the last recession, which came amid Britain's ignominious ejection from the European Exchange Rate Mechanism.

Mr Warburton - a member of the Shadow Monetary Policy Committee - warns that the UK will be badly hit by a US housing market crash.

He says: "There is an increasingly large possibility of a scenario where, frankly, economic activity could fall quite materially. In short, I do not believe that the UK has become a more stable economy."

His thesis is that for the past decade, despite its stable growth rate and low inflation, the UK economy has been brewing up potential problems. These include the record level of debt taken on by the household sector, a similarly large jump in government borrowing and a fall in manufacturing output. If, as many experts predict, the US suffers a housing market collapse next year, this could trigger an even more dramatic downturn in the UK.

September 29, 2006

Iamfacingforeclosure.com kid's new defense: Everybody is doing it - just ask your mortgage broker!

![]()

His blog is the gift that keeps on giving and a great read. Casey, if you're reading this, keep on blogging. Your mindframe as you secured your $2.2 Million in liars loans, and how you got to the point you're at today, is continually fascinating, and is the perfect color commentary to fill in the housing bubble story.

Here's the latest. He also talks about HP'ers being hard on him in the full post

How "Illegal" is it REALLY?

When I mentioned the way I did my loans, I didn't think much of it. I was just being open and honest and shared everything I did - hoping it will help somebody. Yes, on these loans I was technically misrepresenting things like income, cash at closing and owner-occupied issue.

But if you know anything about the state of today's lending industry you will agree that what I did is nothing out of the ordinary.

For more information, see this News Article on Liar Loans or just watch the Liar Loan video. (Now compare to this Wall Street Journal article on the Real Mortgage Fraud). While personally I have always had MORAL issues with these loans, the reality is that Liar Loans are pretty normal.

Consider this:

* Everybody is doing it - just ask your mortgage broker!

* Lenders/banks allow it and turn a 'blind eye' to it.

* The account executives at the banks actually tell the mortgage brokers how to 'sugar coat' the application.

* Lenders make a killing on EXTRA INTEREST and fees for stated income loans - you pay to lie.

Lenders package their loans and sell to mutual funds on wall street. The extra default rate on LIAR LOANS has been pre-calculated. The extra risk is accounted-for in most cases.

For those who are still judging me, I will just say this:

How many of YOU have 'stolen' a music CD or software program by burning a copy of it? Did you NOT know that it's ILLEGAL?

I just had to post it: Rep. Mark Foley (R) Resigns Over Sexually Explicit Messages to Minors

Why is it always the congressmen and religious leaders who are into the freaky stuff?

HP recommendation: Vote Every Incumbent Out (especially the sicko two-faced hypocritical right wing "family values" ones...)

Saying he was "deeply sorry," Congressman Mark Foley (R-FL) resigned from Congress today, hours after ABC News questioned him about sexually explicit internet messages with current and former congressional pages under the age of 18.

A spokesman for Foley, the chairman of the House Caucus on Missing and Exploited Children, said the congressman submitted his resignation in a letter late this afternoon to Speaker of the House Dennis Hastert.

Hours earlier, ABC News had read excerpts of instant messages provided by former male pages who said the congressman, under the AOL Instant Messenger screen name Maf54, made repeated references to sexual organs and acts.

Ladies and Gentlemen, the new National ID Card of the United States of America

Don't furnish a home without it

BUBBLETALK - September thread to discuss the epic housing meltdown underway

Post housing bubble articles here, talk about off-subject topics (in other words, don't threadjack the following threads) and have a good chat. Above all, KEEP IT CLEAN and have fun

Squaring the circle: The two-faced NAR pawn David Lereah's "there is a bubble - there isn't a bubble" confusion

Reading the corrupt Mr. Lereah's latest musings on the bubble, where he "predicted" all along that we'd see an "adjustment", and that we've "now hit bottom", I was reminded of the NAR talking points he put out in December 2005 that said frankly there was no bubble.

Here's the corrupt Mr. Lereah earlier this month:

"We've been anticipating a price correction and now it's here,'' Lereah said. "The price drop has stopped the bleeding for housing sales. We think the housing market has now hit bottom.''

and this:

“The housing boom ended more than a year ago, but sellers are having a tough time accepting that fact, says David Lereah,

Yet here's highlights of the NAR's "there is no housing bubble" talking points he put out in December 2005, for use by his army of 6% minions to convince the last suckers in that their investments would be safe.

Let there be no confusion HP'ers (and the MSM who love to rip-and-read his stuff): David Lereah is a seriously corrupt, never-to-be-trusted, completely discredited pawn of the NAR and REIC.

What is a housing bubble?

As broadly interpreted, a housing bubble refers to an unsustainable gain in home prices. The premise is that a price bubble is at risk of “popping,” resulting in a loss of equity.

Has there ever been a national housing price bubble?

No, not since good recordkeeping began in 1968. There was a national decline in the 1930s during the Great Depression; however, home prices were not a prime concern in that era. The greatest issues were essentials such as food, clothing, employment and shelter of any kind. Declining home prices were a natural result of a general economic collapse caused by the stock market crash in 1929.

Should we be concerned that home prices are rising faster than family income?

No. There are three components to housing affordability: home prices, income, and financing costs – the latter are historically low.

What are the prospects of a housing bubble?

There is virtually no risk of a national housing price bubble, based on the fundamental demand for housing and predictable economic factors. It is possible for local bubbles to surface under the right circumstances, but that also is unlikely in the current environment.

If conditions become unfavorable, home buying may be postponed, but a general price decline remains highly unlikely.

What is likely to happen with home prices?

The forecast is for mortgage interest rates to rise slowly over the next year, which will have a minor breaking effect on home sales. The good news is that will help inventory levels to recover and allow the market to come into a closer balance between buyers and sellers.

In other words, a general slowing in the rate of price growth can be expected, but in many areas inventory shortages will persist and home prices are likely to continue to rise above historic norms.

HousingPanic Stupid Question of the Day

Will crashing house prices cost the Republicans control of the House and/or Senate in November? Or will cheaper gas prices and a new terrorist threat save 'em?

Robert Shiller asks - "If house prices crash in the US, the bastion of capitalism, could it destroy confidence and end the boom in other countries?"

Robert Shiller, yes, my favorite housing bear and truth-teller, had this op-ed today in the Korea Herald, where he raises the point that's been in my head for a bit - can the US housing crash kill housing bubbles throughout the world?

Robert Shiller, yes, my favorite housing bear and truth-teller, had this op-ed today in the Korea Herald, where he raises the point that's been in my head for a bit - can the US housing crash kill housing bubbles throughout the world?

Obviously I'm living in bubble-central, London, England, where I see daily reports now in the papers on the US crash. But Londoners haven't put 2+2 together, and they seem to think what happens "over there" won't affect psychology "over here". Guess what - it will. The exposing of the Ponzi Scheme in the US will draw light and heat to the same Ponzi Scheme anywhere else it's being played. Especially in London.

Also, as HP'ers know, Robert Shiller (author of the ultimate bubble book "Irrational Exuberance") is a professor of Economics at Yale, and he looks like he's taken an Economics class or two in his day.

Compare his writings and thought pattern to the incompetent, corrupt and intellectually challenged Nicholas Retsinas, head of Harvard's REIC-polluted Joint Center on Housing Studies, who looks like a struggling freshman at ASU by comparison.

Here are some of Professor Shiller's latest musings on the ongoing housing bust. Read the whole article, and also google him and read his past stuff too. Yes, he was early in calling the bubble (again). But yes, he also got it right.

Many places around the world have been in a housing boom since the late 1990s. As I argued last year, in the second edition of my book "Irrational Exuberance," the boom is rooted in speculative investment by ordinary homebuyers, fueled substantially by the worldwide perception that capitalism has triumphed, and that all people must look out for themselves by acquiring property. Convinced that private ownership has become essential to smart living, buyers bid up home prices.

Moreover, the fear that one must get in on the boom before it is too late often drives people to bid up home prices faster now.

But the boom generated by such beliefs cannot go on forever, because prices can't go up forever, and there are already signs of a hard landing.

In the United States, newspapers and magazines are trumpeting reports in the last few months that the decade-long boom in home prices may be at an end, and that the bubble may be bursting. The psychology has suddenly changed, creating widespread fear of sharp drops in U.S. home prices.

If home prices crash in the United States, the bastion of capitalism, could it destroy confidence and end the boom in other countries? If so, could a worldwide recession follow?

If there's a housing bubble in Billings, MT, you know something is realllllly wrong

| Take Billings off of my "geo-arbitrage" list... | |

September 28, 2006

HP message to the REIC - kiss my blogger butt

To David Lereah, Nicholas Retsinas, Bob Toll, the realtors over at Realtytimes.com, the lazy Catherine Reagor of the Arizona Republic and her rolodex of realtors, the frauds at firstrung.co.uk, the idiot Gregg Swann at Bloodhound Realty, the incompetent MSM, the REIC HP trolls, and all the corrupt realtors, mortgage brokers, appraisers, builders, bankers and politicians involved in furthering the biggest Ponzi Scheme in the history of humanity, the Late Great Housing Bubble, I've got one thing to say.

Kiss my blogger butt.

There's no editor looking over my shoulder, no incentive to keep this bubble going. Blogging has changed the rules of the game, we are the proxy of the people, and your day is done. I look forward to reporting on the REIC jail sentences, the scandals uncovered, and the corruption exposed.

Thank you HP'ers for making taking this blog to over 250,000 views a month. I hope you enjoy the ride - we're just getting started.

We're going to have fun dragging "there is no housing bubble" articles and authors out for years to come

Sure, the corrupt David Lereah is an obvious one. The Henry Blodgett of the latest bubble. And the new town idiot from Harvard will be run out of town no doubt as well, and mocked for a generation.

Sure, the corrupt David Lereah is an obvious one. The Henry Blodgett of the latest bubble. And the new town idiot from Harvard will be run out of town no doubt as well, and mocked for a generation.

Then you have other biased, corrupt members of the REIC like the Bloodhound Realty dolt, Bob Toll, etc. But I understand where their cheerleading came from - their livelihoods rested on the bubble going up and up.

But there are so many more lurking out there. Clueless "experts" who couldn't see the obvious writing on the wall. Nincompoops who never bothered to read about historical manias and crashes, and truly thought "it's different this time" and "the fundamentals don't matter anymore".

Here's just one of many "there is no housing bubble" articles from last year:

There is no housing bubble in the USA: housing activity will remain at high levels in 2005 and beyond by James F. Smith

There is no evidence of a housing "bubble" in the United States and housing demand should stay strong for years to come.

Three major factors lead to this conclusion.

First, the 77 million baby boomers are approaching the peak home ownership ages of 65-75 (over 83.0 percent versus a national average in 2004 of 69.0 percent).

Second, immigrants, a growing share of the U.S. population, tend to buy houses ten years later than people born in the United States of the same income group and family size.

Third, mortgage rates are not likely to go high enough (8.0 percent or more for 30-year fixed rate mortgages) to put a crimp in demand.

Despite some areas of concern, overall homeowners' equity is at record levels above $9 trillion. Delinquencies are still less than one percent of mortgages outstanding.

HousingPanic Stupid Question of the Day

HP'ers, do you get the feeling you know something others don't know?

Or do they know and don't want you to know they now know?

Or do they not know what they don't know because they wouldn't listen to you tell them what you know that they should know?

Or does everyone just now know?

From dot-com to dot-condo: Empty condo towers and panicked investors caught with the hot potato

Folks, no matter what the NAR or Harvard tell you, condo prices are going to drop nationwide.

Folks, no matter what the NAR or Harvard tell you, condo prices are going to drop nationwide.

Why? Because they were swooped up by investors these past few years to daytrade like pets.com. And these investors don't live in 'em, and if they rent 'em out the negative cash flow kills 'em. If they hang on to 'em they lose even more as their value plummets.

In cities like DC, Vegas, Miami, Phoenix and San Diego, I think you'll be looking at 50%+ declines from top to bottom. They'll come down in price to the point where monthly ownership costs equal monthly rental income. It's called The Fundamentals. Something the corrupt Nicholas Retsinas with Harvard doesn't understand, or doesn't want you to know.

The aftermath of condo fever

People camped out for the chance to buy a unit in Radius, a condominium development in Hollywood, Fla. The building's 285 units sold out in just over 10 hours -- half a year before construction was even set to start.

But that was in the summer of 2004, when the red-hot condo market was peaking and money could be made by investing in condos expected to quickly appreciate. Units were often on the market for resale as soon as they were completed. It's a much riskier proposition to flip a condo in some of today's cooling markets.

"You see some of these communities that investors purchased ... there are no lights on at night," said Bill Donges, chief executive officer of Lane Company, developer of Radius, which is scheduled for completion in the spring.

"The market is clearly oversupplied in many places," said David Seiders, chief economist for the National Association of Home Builders. "The key symptom of that has been on the price front. Prices have taken a hit."

Not wonderful news for those who have invested in condominium units with the intent to sell them quickly -- and are still holding them. According to NAR data, 31% of investment purchases made between 2002 and 2005 were condos.

September 27, 2006

HousingPanic calls for the immediate firing of Nicolas Retsinas, Director of the Joint Center for Housing Studies at Harvard University

As HP'ers may remember from June 2006, Harvard's "Joint Center for Housing Studies" put out a bizarre and incredibly bullish report on housing, much to our amusement and bewilderment, as housing was already well in meltdown mode by then.

So the bubble bloggers did their thing and dug a bit, and sure enough, the "Joint Center for Housing Studies at Harvard" is 100% bought and paid for by the REIC. Their sponsors read like the who's who of the REIC. And King-Bought-and-Paid-For is, of course, as fate would have it, it's head, one Nicolas Retsinas, whose entire livelihood rides on putting out bullish reports to support his masters, the REIC.

So we exposed it, had a great time, and though we nipped that one in the bud. Mr. Retsinas looked silly and stupid then, but I'm sad to say, as of today, he now looks seriously corrupt.

Mr. Retsinas took it upon himself today to put out the strangest of strange articles, again trumpeting housing, and calling naysayers like HP "Cassandras", "Pollyannas" and "Chicken Littles".

Seriously. No, seriously.

No, SERIOUSLY.

He bizarrely uses no data (since he can't - it's all so amazingly ugly as we're in full meltdown mode now), and his arguments are sophomoric at best, frankly smacking of the University of Slippery Rock, not Harvard University for god's sake.

According to the blatantly bought-and-paid-for Mr. Retsinas:

"Cassandra, though, can stop wailing: the expected price corrections mark a slowing in the rate of increase - not a precipitous decline. This will not spark a chain reaction that will devastate homeowners, builders and communities. Contradicting another gloomy seer, Chicken Little, the sky is not falling"

He goes on to state:

"Cassandra can stop wailing, and Pollyanna can stop cheering. Home prices in some regions are moderating, but for a nation inured to CNN's headline-of-the-moment, this moderation does not rate high on the Richter scale of cataclysm."

So, HousingPanic today calls for Harvard to fire Mr. Retsinas, immediately. He is polluting the image and mission of Harvard University. He is bringing disrepute and, frankly, a stench to your fine university.

HousingPanic also calls for Harvard to investigate the personal finances of Mr. Retsinas, who, with his bizarre rantings, has at a minimum the appearance of being on the take from his many REIC masters. We would encourage a hard look at sporting tickets, restaurant tabs, travel expenses, junkets, bank statements and any other quid-pro-quo possibility which would cause such blatant bias and disinformation.

Finally, HousingPanic is requesting Harvard look at the funding and structure of the Joint Center for Housing Studies, so that REIC bias is eliminated from the entity, and a truly unbiased and uncorrupted study of housing may be undertaken in the future.

Harvard is a the pinnacle of American education. To have such REIC corruption within the hallowed halls of Harvard shows just how entrenched the REIC is in American institutions, beyond the Congress, the Media and our financial institutions.

HP'ers, join me in contacting Harvard on this issue:

Joint Center for Housing Studies Harvard University1033 Massachusetts Avenue, 5th Floor Cambridge, MA 02138

Main Number: (617) 495-7908

Fax:(617) 496-9957

Media Relations: Elizabeth England (elizabeth_england@harvard.edu)

Harvard President Derrick Bok (derek_bok@harvard.edu

Harvard Joint Center for Housing Studies Head of REIC Corruption: Nicolas Retsinas (nicolas_retsinas@harvard.edu)

Finally, here is the dirty list of Mr. Retsinas' Real Estate Industrial Complex masters.

Lumber Company

Andersen Windows

Armstrong Holdings, Inc.

Beazer Homes USA

Boise Cascade, LLC

Boral Industries

The Bozzuto Group

Bradco Supply Corporation

Builders FirstSource

Building Materials Holding Corporation

Canfor Corporation

Cendant Corporation

Centex Corporation

CertainTeed Corporation

Champion Enterprises

Countrywide Financial Corporation

Crosswinds Communities

Fannie Mae

Fannie Mae Foundation

Federal Home Loan Bank of Boston

Fortune Brands - Home and Hardware

Freddie Mac

GAF Materials Corporation

Georgia-Pacific Corporation

Gibraltar Industries

Hanley Wood, LLC

Hearthstone

Home Depot

Hovnanian Enterprises

Huttig Building Products

Jeld-Wen

Johns Manville Corporation

KB Home

Kimball Hill Homes

Kohler Company

Lafarge North America

Lanoga Corporation

Lennar Corporation

Louisiana-Pacific Corporation

Marvin Windows and Doors

Masco Corporation

Masonite International Corporation

McGraw-Hill Construction

Meritage Homes Corporation

MI Windows and Doors, Inc.

Move, Inc.

National Gypsum Company

Oldcastle Building Products, Inc.

Owens Corning

Pacific Coast Building Products

Pella Corporation

Pulte Homes

Reed Business Information

Rinker Materials

The Ryland Group

S&B Industrial Materials S.A.

The Sherwin-Williams Company

Stock Building Supply

The Strober Organization

Temple-Inland

UBS Investment Bank

Weyerhaeuser

Whirlpool Corporation

And this from the Harvard website:

The Policy Advisory Board is comprised of senior executives from leading corporations involved in the housing sector, including home building, building materials manufacturing and distribution, housing finance and mortgage banking, design, construction and renovation.

The Chair of the PAB is Thomas C. Nelson of National Gypsum Company and the Vice Chair is Stuart Miller of Lennar Corporation.

FLASH: As predicted, Casey Serin and Iamfacingforeclosure.com is baaaaaack

Two words: States Evidence. OK, two more words: Mainstream Media. Watch the kid score some bigtime stories (Time, Newsweek, Jay Leno?). Watch Congress subpoena him to testify - now THAT would be good theatre.

Casey will someday be seen as the human face of an out-of-control mortgage lending spiral that took the nation on a joyride ending in a horrific, historic and epic crash. No matter what Harvard University's Joint Center for Housing Studies tried to tell you.

Here's a snippet of Casey's latest. I'm glad the kid's back - he adds to the bubble story HP'ers - like it or not.

You see, Sunday morning I published the previous article “Am I going to Jail For Mortgage Fraud?“. Not only did I publish it, but I also sent an email to all my contacts to update everybody on my blog. I wanted to encourage feedback and I was also asking for referrals to good real estate / bankruptcy attorneys. I did get some good feedback, thank you to everyone who replied.

Right after I sent the email out I got a call from an associate. He urged me to take the site down immediately because:

* People will not want to do business with you. Because who knows what Casey might write about me on the Internet? If I do a deal with Casey and he doesn’t like something, what if he will try to “expose” me?? Who knows what Casey’s intentions are anyway?

* You will have a bad reputation for talking too much. We can’t trust Casey. We better not invite him to any meetings. Most definitely we better not share anything about our deals or Casey might think something is “shady” and want to “expose” it on his blog.

* If there is an investigation everybody involved will be hurt. All the well-meaning real estate professionals who helped Casey do the deals will now be in jeopardy because Casey is talking too much! Even if a person is proven innocent, just being in the negative spotlight is often enough to destroy a good reputation.

* Somebody will go after you! Being public and being controversial is inviting trouble. Admitting to doing “shady loans” is double trouble. If somebody’s income stream will be affected by your exposing of “shadiness” they may try to shut you down. There are a lot of just plain angry people out there. You may step on someone’s toes with your “honesty”.

* You spend too much time blogging. What about selling your properties, rebuilding your business or looking for a job?

Very valid points… Thanks to the associate who made that phone call for opening my eyes to the range of negative possibilities. I am known for taking risks and I am also known for sometimes taking dumb risks. I don’t want to hurt people around me with my risks. I don’t want to have a bad reputation among the investors in Sacramento.

So that’s why I pulled the plug.

In the end, the Late Great Housing Bubble will be just a blip on the radar

Sure, bad news for those who bought a home from 2002 to 2006 (to live in or to flip) and didn't heed the warnings to sell, and those who sucked fake equity out of their house and blew it.

Everyone else, they might not have the riches and windfall they thought they had, but for the most part, they'll be OK.

Unless they work at Countrywide. Or Home Depot. Or are realtors. Or work for homebuilder-ad supported newspapers. Or that donut shop. Or have anything to do with the REIC. Or live in Phoenix, or Miami, or San Diego, or DC.

Well, for that matter, maybe a lot of them won't be just fine.

But in the end, just a blip on the radar folks. The biggest blip ever, but just a blip on the radar...

Classic Bubble: Money just raining down from the sky - buckets-full for anyone and everyone to use in the biggest Ponzi Scheme of all time

I found my way to this typical yet sickening mortgage broker's site today, pretty standard stuff I'd imagine. But it really amazes me how easy it is to go out and borrow say $500,000 today, with no income, no job, no credit, no ability to pay back the loan, and no oversight.

A classic trait of any financial bubble is the over-use of credit and leverage:

The abundance of credit, coupled with leverage (buying with borrowed money), accelerates this process and buying leads to more buying. Then comes the panic: some event shakes confidence and wakes up investors to the mania that has clouded their judgment. This panic leads to a crash: borrowed money needs to be repaid and investors will sell anything at any price to meet the bankers' needs.

This bubble folks saw credit and leverage amounts never before seen in the history of humanity. The series of events that led to this point is just amazing - the commoditization of loans, the growth of the unregulated "mortgage broker" channel, the complete lack of oversight by local banks, the no-cap-gains law written by a corrupted Congress, and the willingness of millions to break the law and lie on mortgage applications.

This easy money led to the bubble, period. Without this access to credit and lack of oversight, prices never would have been able to get to the point they did.

But here's a scary thought - it's not over. I could still go out today and lie on a loan, get $500,00, and buy a condo. The bubble will be dead only when this system is fully put down. And that'll take Congressional hearings, new laws, and new oversight. So stay tuned...

"How The Mortgage Loan Financing Process Can Be The Most Pleasurable Experience of Your Life, Bringing you to the Height of Ecstasy and Sending You into Mortgage Loan Nirvana..."

It Is My Goal To Be "Your Lender For Life" By Giving You The Best Service and The Most Pleasurable Mortgage Loan Buying Experience, No Matter What that Means To You, The First Time and Everytime...

No Asset, No Income, No Employment Verification Loans

FICO Scores all the way down to 500 accepted

1% "pick-a-pay", 40 year amortization loans and 125% LTV loans available

FLASH: Homebuilder firesale produces 4.1% increase in unit sales (maybe - nobody knows), prices tumble to unknown level due to rampant incentives

While the MSM is reporting home sales rebounding, and a 4.1% increase in new home sales, HP of course gives you the correct headline. This report is statistically meaningless, fraught with error, reports a totally bogus price number, and really isn't worth the paper it's printed on. Yet we all report it for some reason..

Here's one report that at least took the time to mention the issues, versus the rest of the rip-and-read lazy MSM

New home sales rise 4.1% to 1.05 million pace - Median sales price down 1.3%, first yearly decline in three years

WASHINGTON (MarketWatch) -- Sales of new homes unexpectedly increased 4.1% in August to a seasonally adjusted annual rate of 1.05 million from a three-year low in July, the Commerce Department reported Wednesday.

Sales are down 17.4% in the past year and are down 23% from the peak last July.

Sales in May, June and July were revised sharply lower. July's sales pace was revised to 1.009 million, the lowest since March 2003, from an earlier 1.072 million.

The median sales price of a new home fell 1.3% year-on-year to $237,000, the first year-on-year decline since 2003. The reported sales price does not account for the massive incentives builders have been offering to close deals.

Despite the sales increase in August, there's little reason for near-term optimism about new home sales, economists said.

"Builders are extremely pessimistic," Brian Bethune and Nigel Gault, economists for Global Insight, said ahead of the report. The home builders' sentiment index has plunged to a 15-year low, while housing starts have fallen 19.8% in the past year to a three-year low.

The government cautions that its housing data are subject to large sampling and other statistical errors. Large revisions are common. The standard error is so high, in fact, that the government cannot be sure sales increased at all in August. The 4.1% increase is statistically meaningless.

Oh, the humanity. Countrywide cuts 6,000 more jobs, but more importantly, no more Free Donut Fridays

No more free donuts! I'm outta here!

My only question is what do the other 56,000 Countrywide employees do now that housing has fallen off the cliff? Well, besides read HousingPanic at work and get their resumes ready?

My prediction - 30,000+ Countrywide layoffs by the time this meltdown is over, seeing that they added 22,000 since 2003 alone. Easy come, easy go.

Oh, and more importantly, and more sadly, I'd predict two layoffs at the local Calabasas donut shop.

Countrywide Financial Corp., Calabasas, Calif., the nation's largest residential lender, has confirmed that it will cut up to 10% of its "general and administrative" work force in the coming months.

A Countrywide spokesman confirmed the job cuts to MortgageWire but could not offer a head count for the reduction. Layoffs have already begun, he said. Countrywide employs about 56,000 nationwide. He stressed that the layoffs -- which the company hopes to achieve mostly through attrition -- will not affect the lender's sales staff.

One source told MW that the company has even canceled its regular practice of providing employees with free doughnuts on the last Friday of every month.

Shocking, disgusting and predictable expose on "Liar Loans"

Just watch the video.

We're going to hell in a handbasket.

What the heck happened in this country that allowed things to spin this out of control?

Nice to see the MSM (finally) doing their job and digging into this ponzi scheme now. My only question is - what took so long?

Thanks Darrell for the link.

Now that the bubble has burst and the meltdown has started, anyone practicing or thinking of doing Geo-Arbitrage?

HP'ers may remember this conversation from February, the idea of selling you overpriced sh*tbox in Arizona or California, cashing in at the top, putting the $ in CD's and moving somewhere real. Somewhere where homes didn't go crazy (usually the middle of the country, like Montana, maybe a town in Kansas).

Live the simple life. Stop working, or working so hard. Stop going to flipping Pottery Barn every weekend to buy more junk. Sell the Lexus and get a pickup truck. You get the picture.

So, anyone do it? Anyone regret not doing it by now?

I intend to do it, but that little city won't be in the US, it'll be over here somewhere. We'll see. Give me an internet connection and a phone line, and I'm good to go. Oh, and good train connections, so I can still get to symphonies, opera, the airport and the sea.

From the inspiring Moments of Clarity blog, done by a guy who did just this, here you go:

On Geographic Arbitrage and Corn Fields

Thank you Rich Karlgaard http://www.life2where.com/ for helping me finally pull the trigger on the big move from the "skyrocketing coastal markets" to the flyover country. Reading Karlgaard's book "Life 2.0" and Po Bronson's "What Should I Do With My Life", have really helped me to grasp what it means to exit the California race for AM freeway position and enjoy a fuller life. Now, I'm taking my CA income and job to Des Moines Iowa.

We were able to spend some time there and my business travels keep me in the Midwest quite often and I've come to enjoy it. I realize that living there, snow, cold, etc. will be a shock for a while. But, as I frequently say to friends and family, "I don't know about you...but I tend to drive 2 hours a day to work inside an office after exiting a climate controlled car and then it's too jammed on the freeway all weekend long to actually go anywhere without popping a vein and I have 2 kids under 3....so what am I missing by moving to a different climate???"

As discussed in Life 2.0, we'll probably find a very nice house of roughly 2.5 X the size for about $250k. Yes, you can write a check for houses like that coming from CA. I wont but the thought of saying, "I'll write you a check right now if you take $25k off so I can go buy the Volvo instead of the Hyundai" feels nice.

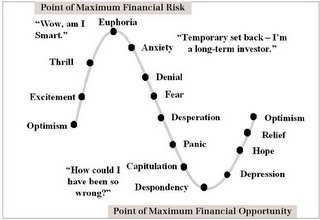

Oh dear god tell me we've moved past denial and are sailing into fear harbor by now

Seriously, is anyone in the US, ANYONE, still in denial that the bubble has burst? Is anyone, ANYONE, still in Euphoria or Anxiety mode?

Seriously, is anyone in the US, ANYONE, still in denial that the bubble has burst? Is anyone, ANYONE, still in Euphoria or Anxiety mode?

Come on!

We have to be, just have to be, in Fear mode by now as a country, with many others already way past that and into Desperation, Panic, and for sellers cutting their price to get out from under their housing financial deathtrap before Mr. Foreclosure shows up, Capitulation mode for sure.

Of course, this blog hits its zenith when we move into Panic mode, but even I think that'll be a year or so from now, when the blood is really in the streets, and not just with housing, but with everything. Yes, everything.

September 26, 2006

I flipping lost it when I got this one. Ladies and Gentlemen, I give you David Lereah

The hat-tip of the year to HP'er Nick for the really awful photoshop job. It's the thought that counts!

Who wants a T-shirt?

The Great Housing Crash is here: "The speed of the (housing) collapse has been astonishing - prices and volumes have a long way to fall"

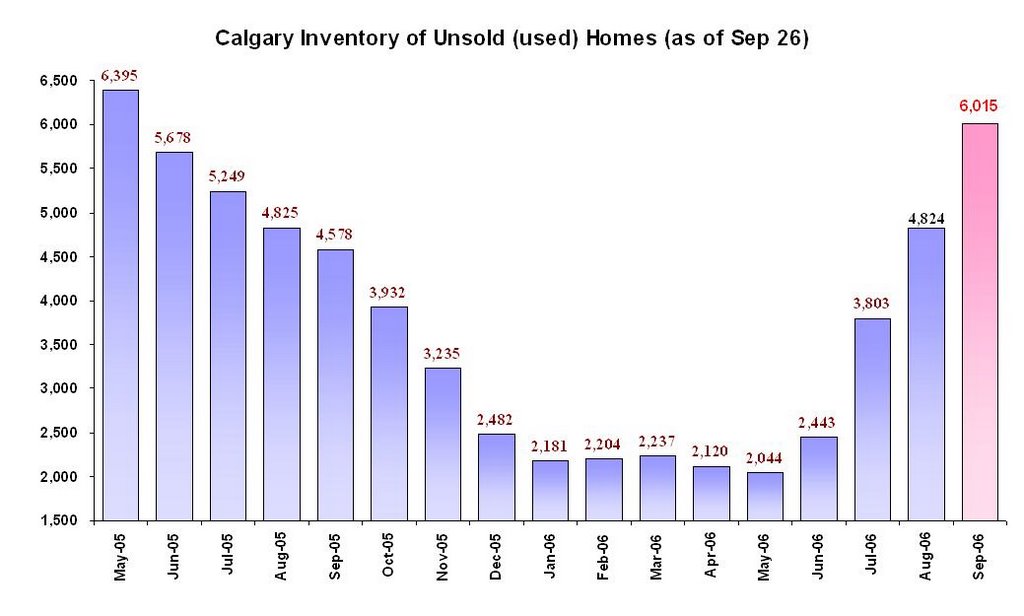

HP'ers - What's your local paper's housing meltdown headline today?

I'm not surprised to see some of the headlines - that small "official" drop in YoY prices caught people's attentions.

However, wouldn't the REALLY be surprised if they knew the truth - that prices are likely down 15% or so already, once you take into account the rampant use of incentives and cash-back at closing to move dead housing inventory.

I enjoyed this quote from Ian Shepherdson of High Frequency Economics picked up in a few papers:

The pace of the downturn has surprised several economists, including Ian Shepherdson of High Frequency Economics. "The speed of the collapse has been astonishing," he said. "This time last year, single-family home prices were up 16.4 percent. With inventory still rising, there is no chance of any short-term relief. Prices and volumes have a long way to fall"

I also saw this quote from the corrupt David Lereah. He must have been drinking a bit at the end of a bad day and let one go:

“If we have prices drop for the rest of the year and sales also continue to drop, then we will have a bad situation in housing of balloons popping rather than air coming out,” Lereah says

Here's a brief selection of headlines around the world. Just wait until the real fun starts....

Home prices likely to fall more - USA Today

US house prices take a tumble - The Age (Australia)

Analyst says of new data: 'Pop goes housing bubble' - Houston Chronicle

US house prices could drop another 10% - The Globe and Mail (Canada)

Home prices drop for first time in decade - Pittsburgh Post Gazette

Looks like the California NAR head dude didn't get Lereah's talking points...

Yes, folks, this is what a housing crash looks like. "Hitting bottom" as the corrupt David Lereah would have you believe? Nope. We're just getting started...

Home sales fall dramatically in California

Home sales in California fell 30.1 percent in August compared to a year earlier, the most dramatic annual decline since 1982, it was reported on Monday.

"We experienced the greatest year-to-year sales decline last month since August 1982, when sales fell 30.4 percent," said California Association of Realtors (CAR) President Vince Malta.

"This is another indication that we're in the initial stages of a long-anticipated adjustment in the market. Buyers today have a much greater selection of properties from which to choose, while some sellers are still clinging to price expectations that are no longer valid in today's market."

I also liked this quote today:

"Pop goes the housing bubble," said Joel Naroff, chief economist at Naroff Economic Advisors. He predicted prices will fall further as home sellers struggle with a record glut of unsold homes.

HousingPanic Message to the Mainstream Media: The Corrupt David Lereah is a Lying Hack - Stop Quoting Him Without a Disclaimer

MSM - enough is enough. Your use of David Lereah rip-and-read press release quotes with no disclaimer should be banned.

By giving this corrupt hack of the National Association of Realtors free-reign, you are allowing propaganda on the highest scale. He is the Tony Snow of real estate. The Iraqi Information Minister of the Housing Bubble.

Did any of you go to journalism school? Ever here of vetting your sources? Ever hear of challenging statements that are made with facts?

David Lereah is a paid pawn of the NAR. He makes money on the side by selling books on how real estate values will only go up and up. Every word out of this man's mouth is a lie at best, corrupt at worst.

Every time you are tempted to use a David Lereah quote, think - who is the source? What does he have to gain here? Is what he is saying backed up by facts? What is his track history with predictions? Who pays him? How does he make his money? What motivations does he have to lie?

I recommend this disclaimer:

"David Lereah, discredited based on prior predictions that have not proven to be true, paid by the NAR to make claims about real estate that may or many not be based on facts, and the author of "Are You Missing the Real Estate Boom, ......"

So I'm thinking I need to write a book - "HousingPanic's Guide to the Housing Bubble Collapse - The End of the Late Great Housing Ponzi Scheme"

Or something like that... Basically HousingPanic - The Book

Only problem is I'm just too damned busy (yet lazy) to tackle it. But I figure with almost 2,000 posts since we launched, nearly 2 Million page views, an active and growing HP community, and a very timely and impactful issue, a book would be a pretty cool thing to put out at this point. But I want HP'ers feedback before I even give it any serious thought.

The blog itself serves as a great base, with all the articles and comments (and funny pictures) that could be drawn upon to form the book and tell the story, hopefully with some humor balancing out the scary stuff.

And, as loyal HP'ers know, I tend to say a few controversial things here and there. So I think it'd be an interesting read, especially in a time of super-slick, do-nothing politicians, lies and more lies from the NAR and REIC, and a mainstream media looking for someone to blame for this debacle.

So, any aspiring writers out there who would like to collaborate on a book, as a ghost-writer or "as told to" kind of thing, let me know. Or anyone involved in publishing, I'll be looking for advice.

I figured we'd hit all the hot buttons and try to tie it together in a neat little bow, including off the top of my head:

The corrupt REIC

Mortgage brokers

Realtors

Builders

Appraisers

The Bubblicious Fed

Greenspan's bubbles and call to ARMs

No-down, negative-am, "liar's loans", interest only

Bush's misguided ownership society

The Fannie/Freddie disaster

Our corrupted Congress

Stupid tax policy

The rip-and-read MSM

Brainwashed/Braindead/American-Idol Americans

The problem with commoditized loans

24-year old speculators

Classic bubbles and manias

Human greed and denial

The out of control consumer / debt fueled society

Building standards, sprawl, urban planning and the exburban nation

Wal-Mart/China/Trade Imbalance/Interest Rates

Poor financial knowledge of Americans

The manufacturing jobs we've lost, never to regain

Illegal immigration

Iran/Iraq/Gas Prices

US Debt/$$ crisis

Social Security/Medicare/Medicaid/The Bankrupt USA

What'd I leave out?

And would you buy the book?

September 25, 2006

Let the blame game begin: How the Fed failed to prevent the housing bubble

It's a bit strange, to go from a voice in the wilderness, mocked, laughed at, discredited, to being spot-on and going mainstream.

Housing Panic is here folks. You, the loyal HP'ers, are vindicated. Victory is ours, and it is sweet, yet it is so painful, so, so painful...

Get ready HP'ers. The time is neigh. The hour of the Great Reckoning is here.

How the Fed failed to prevent the housing bubble

There is total detachment from the bad news now pouring out of the US economy. For several years, the booming housing market has made the difference between recession and recovery for the US economy. Zooming house valuations provided private households with the collateral that allowed them to replace the missing income growth with a borrowing binge.

But as the housing market is sagging, this major source of higher consumer spending is plainly drying up, and most obviously and importantly, income growth is by no means catching up.

In 2005, real disposable incomes of private households in the United States increased $93.8 billion, or 1.2%, while their debts grew $1,208.6 billion, or 11.7%. Total consumer spending on goods, services and new housing accounted for 92% of real GDP growth.

Most economic data have softened, with the downtrend accelerating. In the face of this fact, it could not be doubted that Mr Ben Bernanke and most others in the Federal Reserve were anxious to stop their rate hikes. In question was only whether they would dare to do so in view of the high and rising inflation rates. They dared.

They even disappointed those who had predicted the combination of a declared “pause” with hawkish remarks about fighting inflation.

Present American folklore has it that a protracted slump in house prices is impossible. Let us say for many people it is unthinkable. And that is precisely one reason why this housing bubble could go to such unprecedented excess. The little historical knowledge we have about bursting housing bubbles is from a study published by the International Monetary Fund in its World Economic Outlook of April 2003. It presents past experience in a very different light. Here are some excerpts on decisive points:

“To qualify as a bust, a housing price contraction had to exceed 14%, compared with 37% for equities. Housing price busts were slightly less frequent than equity price crashes...Most housing price busts clustered around 1980-82 and 1989-92, while equity price busts were more evenly distributed across time...

"Housing price crashes differ from equity price busts also in other three important dimensions. First, the price corrections during house price busts averaged 30%, reflecting the lower volatility of housing prices and the lower liquidity in housing markets. Second, housing price crashes lasted about four years, about 11/2 years longer than equity price busts. Third, the association between booms and busts was stronger for housing than for equity prices.”

HousingPanic Exclusive: The Iamfacingforeclosure.com kid is gonna put his site back up, was threatened by his mortgage broker

He might have to blog from the safety of Russia, but I believe the kid is going to go back up. Got scared off after his corrupt mortgage broker tried to put the screws to him

"If I go down you go down" - isn't that how it plays out in the movies?

Seth at Motley Fool picked the story up today (tipped off by HP but didn't credit us). Here's the full article. Nice to see HP having an impact, even if we're not properly credited by the MSM...

24 Years Old, $2 Million in the Hole

So, have you heard the one about the 24-year-old "real estate investor" who's $2 million in debt and still hasn't gone back to his day job? No? Alas, you may never get the full story. Last week, a Californian named Casey Serin started a blog called "Iamfacingforclosure.com," detailing how he got himself half a dozen sinking properties and $2 million in debt. By today, he'd pulled it off the Net, with good reason.

The quick version of the story is this. After taking some courses in real estate investing, this eager kid lied his way into a slew of loans he, admittedly, didn't deserve, and now that he's bleeding to the tune of $20,000 a month, and the housing market is crashing around his ears, he thought taking his story to the Web might somehow help.

A part of me still wonders whether or not this wasn't just a somewhat elaborate hoax, but if it's not, this kid is in deep trouble. Admitting to serial lying on loan applications might be enough to get forgiveness from our short-attention-span society, and it might get you a few "attaboys" from the easily impressed. But I doubt this kind of naive, public forthrightness will serve Casey so well should any of these lenders haul him into court for fraud. (For those who just have to see what was there, a few Web searches will still turn up cached pages.)

Denial: Not an African waterway Even if this is/was just a piece of Web 2.0 performance art, it's not too tough to believe that there are other people in the same situation. If you read between the "Dude, you're going to jail" comments on the site, you might have gotten the uneasy feeling, as I did, that the lesson's not sinking in.

Try this on for size. "You can't buy this kind of experience," wrote one reader. "Seriously it's not the end of the world. No one who ever amounted to anything did it first crack out of the box." It wasn't the only comment along those lines.

With attitudes like this so prevalent, why don't I believe things are going to clear up for people like this any time soon?

Gekko was wrong. Greed ain't good. The problem here isn't real estate per se, nor bad lending.

Well, let's back up a step. If the information on that blog was genuine, Countrywide Financial(NYSE: CFC) and Citigroup(NYSE: C) made some very stupid loans. If Countrywide did, as alleged, make two loans to an overextended "self-employed" 24-year-old with nearly zero assets, will anyone else out there be surprised if its loan book becomes absolutely rank in a few months?

Greed makes you stupid. On a more philosophical level, here's the real problem: People can't help themselves when they think they know how to get rich quick. How quickly they forget. In 1999 and 2000, everyone was a tech-stock wizard. Everyone knew that the bandwidth appetite would keep Cisco(Nasdaq: CSCO) stock shooting toward the moon. Everyone knew that the emphasis on network architecture would make Sun Microsystems(Nasdaq: SUNW) the next IBM(NYSE: IBM), only better.

Of course, the crash proved that the only thing we really had was a rising tide floating all those boats. And it receded at warp speed, leaving plenty of amateurs stuck in the muck. I suspect we're going to see a similar problem in real estate, as more amateur flippers like Casey find themselves backed into a corner. The difference is that this might take longer to unwind, and the consequences could be a lot worse.

After all, real estate isn't so liquid. Sellers anchor to what they paid. Buyers have no reason to rush in at the front end of the crash. Incentive schemes dreamed up by realtors, sellers, and homebuilders like Ryland(NYSE: RYL) prop up prices. Lennar(NYSE: LEN) keeps building despite the writing on the wall. As a result, it will be months before we see a real "correction."

Moreover, unlike most amateur stock players, who are only gambling with cash on hand, the new real estate speculators depend on huge slugs of leverage. Lose everything on your pile of tech stocks, and you're back to zero. Lose everything on leveraged real estate, and you move deep into negative territory. There's nothing like owing $600,000 on a home that's now worth $470,000 to make you wonder why they invented the option ARM, or the 40-year mortgage. You think it was to do you any favors?

Foolish bottom line Let me break it down for you. If you're a twentysomething out to make it big in the world, do yourself a favor and slow down. If you're wearing flip-flops and low-riding jeans to closing, I'm talking to you. Real riches come over time, not overnight. You need to start with a clean financial house, make smart bets, and save your money sensibly.

Twenty-four years old and $2 million in debt is no way to start your future. It's amazing to me that anyone could ever think otherwise.

Contrarian Chronicles: Voodoo debt and the coming recession

HP'ers, don't you feel like you know something that the regular American doesn't? That you've been given a glimpse of the (ugly) financial future we face, yet almost everyone else you know has no flipping idea what's going on?

Well, here's yet another jolt of reality. And again, my only advice at this point is get ready. Whatever ready means.

With debt piled high in a variety of voodoo mortgages, the declining economy will soon turn into a bobsled ride to tears.

Proceeding to the front of the housing ATM food chain, I'd like to spend a moment on how folks' appetite for risk has been enabled by all of this mortgage exotica.

Author Robert Campbell writes: "I always figured the deflation of the housing bubble would resemble a slow train wreck, but there is new evidence that makes me think the correction may occur more rapidly. This is because there is compelling evidence that a recession is dead ahead. … Now that housing prices are going sideways to down -- and incomes and jobs are still sagging -- this 'debt-fueled' artificial-life-support system for continued consumer spending (and an expanding U.S. economy) is running out of gas.

"In the long run, housing prices cannot continue compounding faster than incomes. We are now facing this economic reality. People cannot continue buying homes with creative, voodoo mortgage-loan financing -- that, in the end -- they can't afford.

I don't know who has been more irresponsible, real estate agents, mortgage lenders, borrowers, or banking regulators -- but I do know that the lending standards for mortgage borrowing have dropped to a zero setting for the past five years. If people weren't in prison or earned more than the minimum wage, money essentially was free to all -- whether they could ever hope to pay it back or not."

No happy ending for housing Continuing on, he says: "The United States has experienced the greatest real estate boom in history, but the boom is now turning into a bust, and the aftermath is not going to be pretty.

"The coming recession is not only going to dispel that hope, but it's going to speed up the fall. … The sad fact is that we're living in a debt-fueled economy, as opposed to an income-fueled economy.

Housing prices cannot continue to compound faster than incomes forever. This incredible rise in prices has been driven by artificial demand (ultra-low interest rates and ultra-loose credit), as opposed to real demand (rising incomes and rents)."

He concludes: "Loose mortgage loans that prolonged the boom will worsen the bust. Homebuyers are now going to pay the price for their 'buy now, worry later' spending spree. … With market manias, self-feeding greed on the way up turns into self-feeding fear on the way down. That time is near."

My comment: Yes, it is.

FLASH: Used home sales fall again, bogus price number shows first year-over-year price decline since 1995, Lereah predicts market has hit bottom

HA HA HA HA HA HA HA

Oh, man, this is hilarious.

The corrupt David Lereah just predicted the housing market has "hit bottom". Maybe for realtors (the six percenters), who are only interested in transaction volume and their commissions, and not pricing, but for the other 99% of people who only care about pricing, we're a looooooooooooooooooonnnnng way from bottom.

The corrupt Lereah says this:

``We've been anticipating a price correction and now it's here,'' Lereah said. ``The price drop has stopped the bleeding for housing sales. We think the housing market has now hit bottom.''

And the corrupt NAR President Stevens says this:

NAR President Thomas M. Stevens from Vienna, Va., said sellers need to price to current market conditions if they want to sell within a reasonable amount of time. “In some areas home sellers are not making sufficient adjustments in their listing price, so their homes are staying on the market and contributing to the build up in inventory”

While a real economist says this:

``The housing bubble has burst and housing is in full retreat,'' said Steven Wood, president of Insight Economics LLC in Danville, California. ``What was a sellers' market has become a buyers' market. The housing correction still has a long way to run.''

So who do you believe HP'ers? It goes without asking.

HA HA HA HA HA HA HA HA

{kind=link}