Post any interesting article links here, and have fun with the HousingPanic nominations below. Back Saturday morning (unless something breaks and I can find a net cafe)

I need a guest editor - post here if you want to be considered (Sorry Osman - no R.E.I.C. members!)

Auf Wiedersehen

June 28, 2006

Off to Munich for a couple of days

Nominations for HousingPanic best city awards

Nominations are now open:

1) Best overall US city

2) Best transit

3) Best urban planning

4) Most undervalued

5) Most robust economy

6) Most beautiful houses

7) Best weather

8) Most open minded

9) Least amount of problems

10) Best lifestyle

And my nominations:

1 Boulder, 2 Denver, 3 Portland, 4 None, 5 Seattle, 6 San Fran, 7 Santa Barbara, 8 Boulder, 9 Boise, 10 Boulder

I think Israel has had enough - and so has the housing bubble

Wow - Israeli fighter jets flying over Syria's President's house, an invasion of Gaza, heck, go for the trifecta and take out Iran's nuke plants too.

Wow - Israeli fighter jets flying over Syria's President's house, an invasion of Gaza, heck, go for the trifecta and take out Iran's nuke plants too.

The other shoe is looking for a place to drop. An international conflict could be the final nail in the housing bubble coffin as liquidity dries up, markets fall and consumer confidence plummets.

Nominations for the HousingPanic crappy city awards

Nominations are now open:

1) Worst overall US city

2) Worst sprawl

3) Worst urban planning

4) Most overvalued

5) Fakest economy

6) Ugliest houses

7) Worst weather

8) Most closed minded

9) Worst problems

10) Worst lifestyle

My nominations:

1 Houston, 2 Phoenix, 3Tucson, 4 San Diego, 5 Phoenix, 6 Phoenix, 7 St. Louis, 8 Salt Lake, 9 Detroit, 10 Cleveland

HP'ers: Get familiar with FDIC and their limits - you'll thank me down the road

Got more than $100,000 in any one institution? Got more than $250,000 in any IRA? Got ETF's or funds like GLD? You may want to make sure when the institution(s) who hold your money go belly-up, as so many will during this housing/mortgage debacle, that you don't lose it all

Historically, insured funds are available to depositors within just a few days after the closing of an insured bank. Since the start of the FDIC in 1933, no depositor has ever lost a penny of insured deposits.

Basic Insurance Amount Is $100,000. The FDIC insures deposit accounts such as checking, NOW and savings accounts, money market deposit accounts, and certificates of deposit (CDs). The basic insurance amount is $100,000 per depositor per insured bank.

The FDIC does not insure the money you invest in stocks, bonds, mutual funds, life insurance policies, annuities, or municipal securities, even if you purchased these products from an insured bank.

The FDIC also does not insure U.S. Treasury bills, bonds, or notes. These are backed by the full faith and credit of the United States government.

In addition, federal law provides up to $250,000 in deposit insurance coverage for self-directed retirement accounts, such as Individual Retirement Accounts (IRAs).

Silly question: Did the weather suddenly get nicer in Miami, Tampa, San Diego, LA, Phoenix or Tucson?

I must have missed a memo, because if you listened to realtors, it would seem those are the only cities in the world that people want to live in. A rush of folks who need houses and condos, marching into the sunbelt and Florida to enjoy that great lifestyle that wasn't there 5 years ago, 10 years ago, 20 years ago.

As a matter of fact, I'm not even sure Florida had a beach five years ago - that must be new!

And since so many millions, tens of millions, are rushing there for not only the awesome weather, but the fabulous economy, a million dollars for a house is chump change. It can only go up and up and up!

Not.

Probably the funniest thing is that these cities really don't even have a real economy. People just build houses and sell them to each other. For now.

Housing values, inflated self-worth and the collapse of the consumer

It would seem to me that the collective self-worth of homeowners in the US has soared in the past four years as home values soared. These feelings of good cheer then translated into nice new Hummer H2's with the spinning rims, trips to Antigua and shopping sprees at Nordstroms to name a few.

Cocktail party chatter moved away from "how's the kids doing in school" to "how much have you made on that brilliant decision of yours to buy a new tract home in Mesa?"

People walked around with a spring in their step as they enjoyed their inflated self-worth, and inflated paper-gain "retirement portfolio" consisting of one house.

And some took it to the next step, rushing out to buy "investment property" thus increasing the "paper gains" and feelings of brilliance and self-worth.

Well... how quickly things change....

Now that home values are plummeting, led by second home "investment property", and housing panic is in the air, I would surmise that these feelings of inflated self-worth and good cheer are crashing as well.

Thus, crashing as well shall be the shopping sprees at Nordstroms, purchases of new Hummer H2's with shiny rims, and the reservations to Antigua.

Get ready America. The collapse of the housing myth, and the Real Estate Industrial Complex, are already here. The collapse of consumer confidence and discretionary spending are next.

June 27, 2006

Rampant cancellations - when you're in a hole, quit digging

31% of condo reservations in DC are being cancelled. My only question is, how stupid are the other 69%?

I'd love to see these stats updated by city. Phoenix and Miami have to be crazy. Walk away from $10,000 or sign and lose $100,000? Tough choice

Sold -- or Not: When Home Buyers Walk

Some Will Give Up Thousands to Get Out of This Market

As the housing market cools, builders are reporting that more people are walking away from contracts and from tens of thousands of dollars in deposits.

Wall Street analysts say the Washington market is among those seeing the highest percentages of buyers abandoning ship -- more than double last year's rate, according to one research firm, and perhaps as high as one in three new-home buyers in some places. And nationally, some big builders are beginning to report cancellation rates upward of 25 percent.

The survey shows the cancellation rate locally highest in Fairfax County, at 30.9 percent, compared with 0.8 percent a year ago. Half of condominium buyers there canceled, compared with no cancellations a year ago. When the statistics are looked at by a single county or type of housing for one month, however, the number of transactions is small.

People who are buying for investments rather than residences are the most likely to bail out, experts said. They reason that it would be better to lose a deposit than to go ahead with an investment that could lose value, particularly if builders are cutting prices in the same or nearby projects.

I have a friend who bought a $700,000 1-bedroom loft in San Diego last summer because..

He thought it'd make him popular with the ladies. I told him not only would he lose his shirt with depreciation, but he'd be so house-poor even if he became the San Diego Don Juan, he wouldn't be able to afford to take a date out to dinner

A year later, he's weirded out that he still doesn't have any neighbors (the units were bought by flippers), the wine and cheese parties and hot models promised in the marketing materials didn't materialize, his interest-only payment combined with the condo association fee is killing him, and he's thinking of getting out and renting.

This has to be happening around the world. Oh, the photo above is from Toll Brothers. Of couse.

New HousingPanic rule: Only smart people allowed to comment

There. That should take care of it.

Seriously everyone, elevate your game. I realize it's the wild wild west of the internet, but let's all try to learn something here, and learn something from each other.

No, HP's not a left wing tree hugging loony. No, HP's not a right wing hate-filled neocon. No, HP didn't lose any money on gold.

Yes, HP thinks realtors should go away. Yes, HP thinks the bubble has popped and the housing industry is crashing. Yes, HP thinks illegals Mexicans should be deported. Yes, HP thinks we should get the F out of Iraq. Yes, HP thinks the US's fiscal house is a house of cards. And yes, HP thinks Bush is incompetent, Hillary is a joke and the system is corrupt.

I call it like I see it and make my argument. Anyone who uses name calling or swears as their main argument shows their lack of intelligence.

Make your case, keep it clean, add to the discussion, and have some fun on this blog.

June 26, 2006

George Soros says we're in a Gigantic Real Estate Bubble

Via the Piggington blog, from Soros' latest book. I'm going to see Soros at the London School of Economics in a couple of days and I'll ask for his comments on this if I can...

You just know the Soros's, the Buffets etc are way the heck out of real estate and hording cash to buy at distressed prices in a few years. And you know the Trumps are screwed.

I believe we are currently in the midst of a gigantic real estate bubble. It was caused by the determination of the Federal Reserve Bank not to allow a stock market decline in 2001 to turn into a self-reinforcing rout.

The federal funds rate was lowered to 1 percent. Mortgage institutions encouraged mortgage holders to refinance their mortgages and withdraw the excess equity. They lowered their lending standards and introduced new products such as adjustable rate mortgages (ARMs), “interest only” mortgages, and promotional “teaser rates.”

All this encouraged speculation in residential housing units. House prices started to rise at double-digit rates. This served to reinforce speculation, and the rise in house prices made the owners feel rich; the result was a consumption boom that has sustained the economy in recent years.

Again, the bubble can be attributed to a short-circuit between the value of assets and the act of valuation. This short-circuit is called the wealth effect.

The Great Mirage: People actually BELIEVED their homes were worth 50% more than they were a year ago

In Phoenix, where we saw 55% home price appreciation in 2005, people actually still think their homes are worth that much. They got to believe, so certainly, so strongly, that their homes were worth so much more than they were just a few months before

Demographics! Weather! No more land! Cheap versus California! The New Economy!

pa-lease.

It was all just a mirage. It was flippers descending into town and scooping everything up, driving down inventories while driving up prices. Then it was the locals becoming flippers themselves. Then the music ended. And the locals are holding the (overpriced) bag, while the flippers flee.

So now we get to go back to 2004 (or worse) price levels. In Phoenix, that means a 40%+ haircut. And it also means hundreds of thousands of people left unemployed, families destroyed, and an economy in shambles.

All because people believed their homes were worth 50% more than they were just a few months before.

June 25, 2006

Feel some flipper panic - here's a real situation from Tucson, Arizona

From a housing investment board (great insider reading!) - here's a post from a would-be flipper in Tucson. You know this is going on around the country (and perhaps the world). Thanks GF for the link.

I purchased a home in south Tucson (Vail) through Chris Szabo and closed on it 1 month ago. The market is flat and there is now competition and plenty of homes for sale in my neighborhood. I had planned to flip this right away but I have had NO offers and very FEW lookers. I'm feeling seriously burned and need out!

Here are the numbers:

Payments (all inclusive): $2500/mo first payment due 7/1

Loans (100% financing): $299k

Lowest competitor on mkt priced at $298k and not sold.

If I COULD sell it at $299 I would lose the RE commissions and closing costs estimated to be about $14K. Of course, the longer I hold it that $2500/mo starts to really add up. I want to prevent getting even deeper into this.

I need to either dump this asap and take a sickening loss or...? Should I contact the lender and tell them I can't make payments? What would foreclosure/ short payoff/ deed in lieu do to my credit? Given the way the market is going(looks flat) is it worth it to try and lease option? Can you think of any other options?

I acknowledge I have made a huge mistake so please no flames. I know there are great minds on this board so any help would be greatly appreciated.

and this follow-up

No exit strategy. Bought on speculation and made big mistake. Will never do this again! $1500/mo will kill me over a period of a few years. Reduction in price seems to be a reasonable strategy. Hope it works!

The corrupt David Lereah has a new book out

So when does he get the pie-in-the-face treatment at a speech? When does the MSM start referring to him as "the discredited David Lereah". HP'ers know I only refer to him as "the corrupt David Lereah" (TCDL for short)

It'll be fun to watch him defend himself at the 2008 Senate Housing Bubble Hearings.

Hat-tip to HP'er Damon for the work

Here comes the stories about homebuilders not paying the subcontractors and the Mexicans getting pissed

When the Phoenix economy hit the skids in 2001, you saw some housing developments go kaput right in the middle of construction.

When the Phoenix economy hit the skids in 2001, you saw some housing developments go kaput right in the middle of construction.

When the builder is in trouble, they stop paying their subs. Then the subs can't pay the illegal Mexicans. Oops, I mean carpenters. And as HP predicts, when the layoffs and stop-payments hit this community, watch out. Here's the first of many articles to come. Yes, folks, it's all connected.

Firm is failing to pay its carpenters - Says it awaits cash from home builders

More than 100 workers at a Scottsdale construction framing company haven't been paid in several weeks, and that has Latino community advocates concerned that some employers are taking advantage of workers.

Veemac Framing Corp., a subcontractor for some of the Valley's top home builders, acknowledged that it has not paid the workers, who are owed three to five weeks of back pay. Company officials blamed a financial dispute with two home builders and a third company that is hindering its cash flow. Veemac said it would pay the workers as soon as the dispute is worked out.

The company plans to pay the workers as soon as it negotiates payment from two of its customers, U.S. Home and Richmond American Homes.

The unpaid workers, most of whom have work permits and are authorized to work here, began showing up at radio station La Campesina last week.

HP'ers - Contact HousingBubble2 and let Ben know he should (finally) add HP to his blogroll

Hey, it's only been a year. Seems like Ben would (finally) see HP as a peer, a brother in arms, not as competition. And I know a lot of HP'ers visit HB2 (with my strong recommendation), and I know a lot of HB2'ers visit HP (even though Ben may not like it).

Contact him at thehousingbubble@gmail.com or click here. A hundred emails from HP'ers might do the trick. Kum Ba Ya.

My take is that Ben reports the news, Wall Street Journal-like, while HP is an over-the-top, immature, irreverent and in your face news and opinion rag, Fox News-like. If ya know what I mean. Plus I have funny pictures.

The bubble blog world is big enough for 'em both

Where in the US will home values will not drop over the next 4 years?

Is there a safe haven in the US? A place where you can still buy a house and rent it out for positive cash flow if you needed to? A place that if you bought today you wouldn't be upside down four years from now?

Make your case here. Find me that place.

It's Sunday - everyone go hit some open houses (you know it's lonely out there)

Oh dear god I wish I was in Phoenix this weekend to run around the new condo developments, submitting low-ball offers of say 60% below asking. Just to see the reaction (and the counter-offer)

Boy, it'd be fun to go to a new housing development in say Queen Creek, or Maricopa, 50 miles out of the city, and ask the builder if they'd be willing to throw in a Prius and free gas for a year to close the deal.

Someone go have some fun and report back. I'm jealous.

I'd bring the realtors milk and cookies though... it's probably been awhile since they last ate

June 24, 2006

Don't look at the home's price - ONLY look at what the monthly payment is

Yes, there truly is a sucker born every minute. Around the world, the financially ignorant masses could care less what the home's price is - they only care if they can afford the (current) monthly payment - on the house, on the Lexus, or on that new furniture set.

Here's a website (thanks JohnFC) that perfectly illustrates this stupidity - all the houses featured show only the monthly payment - an NOT the price. But hey, who cares about the price, even if it's plummeting. It's the monthly payment that matters!

Plus they've got a really cool logo - so trustworthy and prestigious, those guys at Presidents!

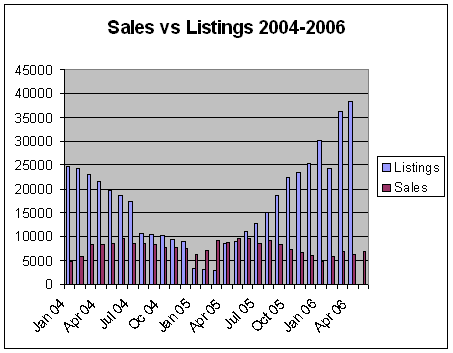

Home inventory piling up while sales dry up. Care to wager a guess on what comes next?

Phoenix is now at 50,000 unsold listings and gaining. Sales volume is plummeting. Builders keep delivering new unsold units to the market, while slashing prices and adding huge incentives. Yet homeowners keep their houses on the market at last year's price. This scenario repeated in cities across the US.

Well, the question is not IF this situation will change - it's a question of WHEN the standoff will end. The smart folks in the room will lower their price NOW - take anything they can get and get out, even at a steep loss. The stupid and greedy ones? They'll hold out and hold out until they lose everything. Having felt they "deserved" the price their neighbor got last year, or that their realtor/appraiser/lender/Zillow told them their house was worth.

There'll be interesting negotiations and decisions taking place throughout the country, where upside-down owners have to consider offers that will leave them with a debt to pay off for years. There's folks out there who just bought - in the past 12 months or so - that today are thinking of getting out already.

There are some renters who think FINALLY - let's go jump into this cold market with lowball offers - only to buy a house that keeps depreciating like the falling knife it is.

You'll see condo developers slash their prices, getting sued by the current depositers who'll be underwater when or if they close. You'll see Bob Toll selling more stock before it hits $0.

Feel free to get on record with your guess of price declines. Catherine Reagor, the lazy Arizona Republic writer, made up an unsourced number of Phoenix falling 10% from the peak. I'll stick with 33% minimum as we get back to the mean.

Price declines - the next stage of the bubble. We predicted the euphoria stage, we predicted the exploding inventory, we predicted the denial, now comes the panic and significant price cuts.

June 23, 2006

Time to start a condo project dead pool?

So many of these condo projects will be cancelled - construction halted, deposits returned, developers sued - it'll be near impossible to keep up.

In Vegas, we've already seen the death of Icon, Las Ramblas, Ivana, Aqua Blue, Hard Rock, Liberty and more.

In Phoenix, there are many projects that are so horrificly thought out or overpriced that should have been stopped (Playa del Norte, The Vale, X10 Wine Lofts, ...) and in Miami a total condo disaster is about to unfold with the insane overbuilding.

So, nominate your favorite White Elephant, the most outrageously overpriced, stereotypically marketed, last-sucker-in, height of stupidity candidates here

Oh, boy, how we'll wonder "what were we thinking" just hours or days from now...

The most important question on most people's lips is - where does the line start to get the deposit back?

Are there any safe havens left?

For those that simply want to protect capital, it's getting tougher and tougher.

Any thoughts or recommendations?

Dollar is looking good right now vs. the British Pound - 1.815. Why? Fed keeps raising while the Bank of England stays put - and their notes said they didn't raise because the stock market dropped. Amazing. Inflation? Who cares? Making sure stocks don't drop - priority #1 for England's central bank. Making sure the Housing Ponzi Scheme doesn't end in England is priority #2 here too. Policy aimed at satisfying the voters versus keeping inflation tame will result in a financial disaster here.

Wankers.

Laughable.

Proof that realtors are really stupid - the Bubble Fence

David at BubbleMeter submits this proof - the Bubble Fence. Would any sane person buy a condo in a development where it looks as if every owner wants the heck out of dodge?

What this shouts to me is:

1) Desperation

2) Panic

3) Stupidity

4) Lowball Offers Accepted!

What a housing bubble burst sounds like: "The market isn't soft. It isn't even slow. It's dead."

Pop. It's over. Ding dong, the housing bubble is dead. Even David Lereah can't lie his way out of this one. Now comes the panic. Thanks 200 mbps for the link. From New York:

It's over.

The crazed phase of frenetic home buying in Westchester, Rockland and Putnam counties has screeched to a halt — leaving some industry experts wondering if the sound they hear now is the housing bubble bursting.

"The market isn't soft. It isn't even slow. It's dead," said Liz Rosenblatt, an agent with Fuerst & Fuerst Inc., a real estate firm in New Hempstead.

Scott Stiefvater, a broker-owner at Stiefvater Real Estate Inc. in Pelham, said prospective homeowners are still looking at properties. "They just aren't buying," he said. "I'm getting a little worried."

After nearly seven years of unprecedented strength, the housing market has taken an unexpectedly steep slide, real estate professionals throughout the Lower Hudson Valley concur. It's gone from multiple offers for more than asking price just hours after properties were listed for sale to no offers at all, even after price reductions.

At least some homeowners, however, are panicking. Worried that increased supply will lead to rapid price deceleration, they are rushing to put their homes up for sale. Some of them think the market will only get worse, real estate agents said.

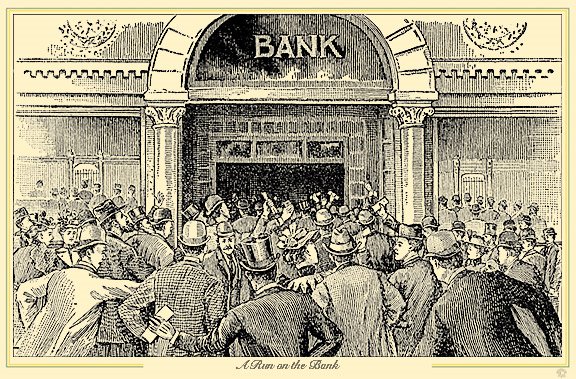

Could the banking system be on the verge of failure?

The Great Depression saw typically leveraged margin accounts go bad, leading to a long series of consequences. The Great Housing Depression upon us will see insanely leveraged margin accounts go bad (today called "no-down home mortgages"), and boy, will there be consequences.

Someone made those loans. Someone holds those loans - and not just in the US, but around the world. Someone believes the collateral (the house) against the loan will protect them.

Well, when the loans go bad (payments stop) and the asset value plummets (house price declines), we got ourselves a heap of trouble.

Because of the lack of oversight on these loans (hello Fannie and Freddie), we basically have a system of unregulated, unwatched margin accounts being distributed to the masses, not even the educated speculator as in the 20's.

And the bagholders are going to get killed. And I don't think our highly leveraged, debt-addicted government can bail them out.

Panic in the 20's resulted in a run on the banks. Panic in the 2000's will see people trying to dump their houses at any price. Then as banks start to fail, a run on the banks themselves and use of FDIC's $100,000 insurance.

You'll see a slippery slope, you'll see momentum take over, and you'll see a Great Unwinding.

What will the unemployed homebuilding illegals do now?

Here's a letter to the editor today in the Arizona Republic. File this under "unintended consequences" and boy, what a tinder box we sit on today. Remember when Paris was burning earlier this year with immigrant anger?

Well, America is about to see millions of unemployed illegal aliens inside its borders. Get ready for a wave of crime, rioting and protests. People get really mad when they can't work or eat.

Another problem passed along

Jun. 23, 2006

With the downturn in the construction industry, what do the construction companies plan to do with the illegals they just had to have to operate? Or is that now our problem? -A. Turberfield, Surprise

June 22, 2006

Where'd The Banker go? Anyone else see a trend here with Toll Brothers?

Boy, nice timing on those sales last summer by the corrupt and evil Bob Toll. And anyone remember The Banker and his boasts about making a killing betting against HP and on the Real Estate Industrial Complex?

I hope he didn't jump.

Pop. The end of the American dream?

Charles Hugh Smith makes some great points here about equity extraction, the decline of the middle class, and the fakeness of the current "boom" - a $4 Trillion debt fueled orgy of greed.

Charles Hugh Smith makes some great points here about equity extraction, the decline of the middle class, and the fakeness of the current "boom" - a $4 Trillion debt fueled orgy of greed.

Now the music has stopped, and reality is setting in. Doom and gloom you may say. Reality I say.

And I'm especially pissed off at the Bush Administration's "Ownership Society" push on the lower classes. Yup, go buy a house from rich whitey right when its value peaked. The rich got richer, and the poor, well, F the poor.

(Extra HP credit for any discussion of the photo)

A great con has been played on the most vulnerable aspirants to the American Dream--those striving mightliy to join the middle class. Just buy a house, the doctrinaire pitch has it, and soon, thanks to rising housing prices, you'll have equity and thus some measure of wealth. After all, house values never drop, they only rise.

Only there was one little problem: millions of households didn't have the traditional 20% down payment--a standard which became ever more unattainable as housing prices exploded.

American homeowners are no longer sitting on paid-in-full homes; they're sitting on heavily leveraged mortgages they've taken out.

The cheerleaders are missing one key point. The collapse of the housing bubble won't just take out an isolated 10% of households; it will take them out first and then move down the economic chain in domino-like fashion

You do see where this is going, don't you? A political revolution is brewing. Not a violent revolution, of course, but one fueled by the catastrophic loss not just of whatever small capital those 150 million people (half of our nation's population of 300 million) might have acquired, but more importantly, perhaps, the loss of their belief in the American Dream--of home ownership and a life of luxury paid for by painless extraction of ever-rising equity.

Renters and Bubble Sitters - are these now the happiest days of your lives?

Breaking down the Arizona Republic piece a bit more

I reread the article a couple of times. Couldn't believe the frankness of the first stanza - shocking to see the MSM report any semblance of the truth - especially funny since when I pulled the article up, there's a big KB Homes advertisement on the top banner. Too funny.

But then you really get into the meat of the article, and you could just hear Catherine Reagor's editor over her shoulder saying "Cat, no, we just CAN'T be that strong. Water it down a bit - give us some wiggle room. We have a BUSINESS to run here don't forget (nudge nudge)."

Also, as HP'ers know, I've been very critical of this reporter's work - calling it frankly lazy, as she rushes out to get Real Estate Industrial Complex quotes, and never adds a disclaimer or even questions the quote. Here's some doozies from the piece and my commentary:

"economists say it looks as if the slide will continue for at least the next six months, possibly pulling down home values as much as 10 percent before it's done" - WHO, CAT? WHAT WONDERFUL STABLE OF SOURCES DO YOU USE TO MAX OUT AT 10%? L-A-Z-Y.

"No one is calling for the Valley's housing market to crash as it did in 1990" - WRONG - HOUSINGPANIC WHICH YOU READ IS CALLING FOR A CRASH CAT.

Valley home values will drop a little," Sullivan said. "Look at demand and supply. - OK CAT, HERE WAS YOUR BIG CHANCE. DEFINE "A LITTLE". ASK A FOLLOW UP QUESTION. REPORT FOR GODS SAKE.

A drop in home prices alone won't be a crushing blow to the Valley's housing market. - UH, CAT, NICE THROW-AWAY SENTENCE FROM YOU HERE. IS THAT YOUR OPINION? THEN SAY 'THIS REPORTER BELIEVES'. AS YOU KNOW, HP BELIEVES THE DROP IN HOME PRICES IN PHOENIX WILL DEAL A DEVASTATING BLOW TO THE VALLEY'S HOUSING MARKET AS WELL AS THE VALLEY'S TOTAL ECONOMY.

"The only people who will really be affected are those who purchased last year, when there was fluff in the market," said Elliott Pollack, - FOLLOW UP CAT! THE ONLY PEOPLE? OK, I GUESS THE ILLEGAL MEXICAN LABORERS WON'T BE AFFECTED, EH? I GUESS THE TENS OF THOUSANDS TO LOSE THEIR JOBS WON'T BE AFFECTED? I GUESS EVERY HOMEOWNER IN PHOENIX WHO LOST PAPER WEALTH WON'T CARE EH? I GUESS FOLKS WHO CASHED OUT THEIR EQUITY AND NOW HAVE CRUSHING DEBT AREN'T AFFECTED? WHAT A JOKE

I could go on and on, and maybe I will on another post. I'm happy to see the article written, but I continue to be saddened by the poor reporting skills of Catherine Reagor and her Arizona Republic editors

June 20, 2006

FLASH: Arizona Republic finally reports the truth about the Phoenix housing crash underway

FINALLY!!! Catherine Reagor, lead housing bubble reporter for the Republic, still too fond of using realtor quotes, after numerous emails from yours truly at Housing Panic, FINALLY reports in frank terms the housing panic underway in Phoenix (thanks Eco). Of course, no mention of HP or housingbubble2, even though I've gotta believe she's reading...

10% decline though? I don't think so. We're going down 20%+, and I'd predict all the way back down to pre-bubble, which means a 33% haircut to wipe out the 50% bubble gain last year.

Had to interrupt my vacation for this one. I couldn't be happier to see the MSM actually reporting the story. This is a sea change. The panic that this article will cause in Phoenix will actually speed the declines now. Phoenix HP'ers - please report any reactions from the ground.

You can email your regards to the reporter here or catherine.reagor@arizonarepublic.com

How low will it go? - Home prices may dip 10% as fear grips Valley market

Catherine Reagor The Arizona Republic Jun. 18, 2006 12:00 AM

Greed drove metropolitan Phoenix's home prices and sales to new records in 2005. Fear is driving the market this year.

Home buyers are worried about paying too much and are waiting to purchase. Concerned about dropping home values, some owners are trying to cash out. Builders, struggling to sell even deeply discounted new homes, are scaling back production and warning of lower profits. Each day more people, from contractors and mortgage firms to real estate agents, are losing jobs or money in the metropolitan Phoenix's rapidly slowing real estate market.

Until recently, the market's slowdown had been considered a necessary, short-term hardship to offset last year's wild run-up in prices. But now many analysts and economists say it looks as if the slide will continue for at least the next six months, possibly pulling down home values as much as 10 percent before it's done.

"There's a psychological umbrella of fear in Phoenix's housing market now," said Tim Sullivan, a national housing analyst with San Diego-based Sullivan Group. "Buyers are uncertain."The big question is, how much more will the market slow?

The only people who will really be affected are those who purchased last year, when there was fluff in the market," said Elliott Pollack, an Arizona economist and real estate investor. "But they will be OK if they stay in their homes for a little while."

"My sense is the worst is behind us, and the housing market will have stabilized with smaller jumps in listings and more steady sales by October," said John Foltz, president of Realty Executives.

June 19, 2006

Gonna be in France for a couple of days - chat away!

Man, you get away from the internet, newspapers and TV for a few days and you forget all about this little thing called the Housing Bubble.

Then I'll be walking down a street in Paris and see a flat for sale for 800,000 Euros, and remember our little friend is alive and well

Chat away - I'll be back Wednesday night... Market tanking again? Oh, FYI, I picked up puts in SOLD on Friday - they're gonna get KILLED by Zillow.com

Cheers

June 17, 2006

Do they live in the same city? Here's the housing market conditions report from Phoenix from "The Realist" and "The Snake"

The Realist (nice to see some honesty from the realtor profession - I'd hire this guy if I wanted to use one)

Currently there are 43,345 residential homes for sale in the Phoenix area in the Multiple Listing Service. This is an all-time high record for the Phoenix area. 3,347 or 8% of them have been on the market for more than 180 days. 9,655 or 23% of them have been on the market for 90 days but less than 180 days. That means that 13,002 or 31% of the homes for sale have been on the market for at least 90 days and have not sold. (Thank you Mr. Shaw for the accurate data and honesty. You are a gem in a pile of dung)

The Snake (tells his clients this stuff in a desperate attempt to find the last sucker in. Talks out of both sides of his mouth. If you'd like to send him a note or heck, buy a house from this guy (snicker snicker), do so here)

Phoenix is attracting the largest amount of new residents in the US: 30,000 "new neighbors" in just one year! Climate and job opportunities are two of the biggest lures to Phoenix and why more and more people are willing to move their homes to "The Valley of the Sun".

The media's hype that the real-estate market's bubble has burst is simply NOT TRUE. (NAR talking point used nicely)

Don't be fooled! What we are experiencing right now is a NORMAL Buyer's market. Housing prices have started to slow down which is helping keep housing affordable to everyone. (Huh - you said there's no bubble?)

IMPORTANT!!!! If you are looking to buy, NOW is the time to do so since there are many homes that have been on the market for several months. (Why would I buy if the value will drop even more? Huh?)

Open houses are "popping" up everywhere, and Seller's are anxious to sell their homes quickly since they are used to last year's market. (Dude, bubble, or no bubble - keep your lies straight)

If you are looking for a house don't wait until the bidding wars start again, buy now when the market is in your favor! (You'll never see bidding wars again in your lifetime sport. And learn from the honest guy above - that's how you earn business and stay in business. For you? Start looking for new work, you're a deceptive snake.)

BUBBLE TALK: Newest thread to talk about the bubble

Ah, nothing like a good housing bubble discussion to get your day started

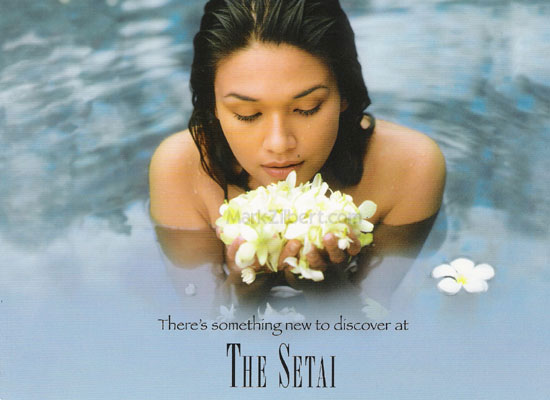

Two year old South Beach condo project - 25% of units for sale, $750,000 to $29 Million

Took a peak at CondoFlip to see if someone is still turning on the lights there. Found this one - two years later, 46 of the 163 units looking for a buyer, at rates that nobody could ever cash flow by renting 'em out. Not to mention the $1000+ per month maintenance fee. Unreal.

Check out unit #3806 - $3.1 Million for 1306 square feet. Plus $40,000 a year maintenance fee. I don't think anyone is this dumb, are they?

Wonder what HUD will end up getting these for?

Developer: Setai Group, LLCArchitect: Alayo & Denniston InternationalBuilder: Skanska USAYear Built: 2004Number of Units: 163Number of Units Listed For Sale: 46Unit Sizes: From 847 to 5800 s.f.Sales Data as of 6/16/2006Lowest Available Price: $750,000Highest Available Price: $29,000,000

Shiller: U.S. housing boom is biggest since 1890. HousingPanic: US housing bust will be the biggest in history

What goes up must come down. Everything reverts to the mean. It's not different this time - it's never different. And periods of speculative craziness always end badly.

What goes up must come down. Everything reverts to the mean. It's not different this time - it's never different. And periods of speculative craziness always end badly.

This time, with the vast majority of the US population involved, and infinite margin (no-down loans) in many cases, the bust will be horrific.

The recent housing boom is the biggest the United States has ever seen, but its underlying reasons may have been psychological, economist Robert J. Shiller said on Friday. New data also suggest the market might be at the end of a cycle, he added.

The only time since 1890 that compares to the recent residential real estate market is just after World War II, the Yale University professor said during a presentation on U.S. home prices, held at Standard & Poor's in New York and broadcast to journalists on the Web.

"After World War II, the soldiers came back and they wanted houses and started the baby boom. And when you had babies, you wanted houses with at least two bedrooms -- and that wasn't so common back then. They went on a buying spree and it pushed home prices up," he said.

The recent boom, however, doesn't have the same fundamental variables causing prices to soar, he said, adding that variation in such things as building costs, population and interest rates doesn't adequately explain the reason for the housing boom.

"I don't see why home prices should be shooting up that strongly," Shiller said, adding that speculation may have played a role. "It's a sign of concern."

June 16, 2006

The corrupt and bloated Dennis Hastert enriches himself by $2,000,000 on land deal tied to highway bill

Nice to see the corrupt and bloated Dennis Hastert cash in on a $2 Million profit on a land deal in Illinois made possible by the highway bill he had drawn up and passed.

Throw the bums out. All of 'em. Let's start over in 2006. This bunch stinks. And I think there should be an investigation of every member of Congress's land and house deals over the past five years. There's gotta be more Hastert and Cunningham deals out there. Jail time awaits so many.

Speaker of the House Dennis Hastert (R-IL) realized an estimated $2 million dollar profit last year on an Illinois land deal that included acreage near a future interstate highway Hastert pushed to build.

The land was sold just five months after Hastert inserted a $207 million appropriation bill for the Prairie Parkway highway during a closed-door Congressional budget conference.

The deal, representing a 300 per cent return on investment, was reported in Hastert's financial disclosure form filed this week, although the role of a secret trust set up by Hastert to sell the land was not disclosed.

A spokesman for Hastert, Ron Bonjean, confirmed the details, which were first reported by Bill Allison of the Sunlight Foundation, an on-line political watchdog group. The Speaker's spokesman said land in the Plano, Illinois area is "booming," and the future highway had no impact on the price.

FLASH: David Lereah says something honest - prices to fall, then predicts "hordes of buyers"

Anyone check the temperature readings in hell today?

He said the first slightly honest thing I've ever heard him say, that prices are gonna fall. But 10% to 15%? Try 30% to 60% Mr. Lereah.

He then followed it up by the same smarmy stuff - saying he's gonna buy some investment property in Florida, and that hordes of buyers will descend on Florida. Yeah, right.

By the way, it's bad enough he's corrupted by his paycheck from the NAR, but I'd also hope people know he pumps the bubble because he has housing investments himself. CNBC now has to disclose analyst and broker conflicts of interest. The media should do the same for the corrupt David Lereah.

Thanks David at DavidLereahWatch for the link

The housing standoff between buyers and sellers in South Florida will continue for another six months, and then prices in some areas will fall, a real estate trade group economist predicted Tuesday.

In some cases prices may fall by 10 percent to 15 percent, said David Lereah, the National Association of Realtors' chief economist, who spoke Tuesday in Coral Gables. But in many areas prices will still rise modestly this year, by 4 percent to 5 percent, he said. And when sellers finally bring asking prices down, pent-up demand will likely result in hordes of new buyers in South Florida.

The long-expected shakeout of the real estate market now underway is healthy for a region both overbuilt with new condominiums and overrun by speculators, Lereah said. Unlike in previous real estate downturns, the economic and demographic fundamentals underpinning South Florida real estate remain strong, he added.

So strong, in fact, that the Washington, D.C.-based economist is looking to buy some investment properties here himself.

Why does Texas real estate suck?

I've always been amazed at the comparitively low prices in Houston, Dallas, San Antonio and even Austin (although that one is rising). Here's a report from the #1 most undervalued market in a recent study - College Station.

Even the flippers haven't got prices up by selling to each other.

So what is it about Texas real estate that keeps is in the doldrums?

When economists in Cleveland and Boston recently ran the numbers, they concluded that houses in this college town were a huge bargain.

The analysis by National City Corp., a Cleveland banking concern, and Global Insight Inc., a Boston consulting firm, ranked the adjacent towns of Bryan and College Station -- home of Texas A&M University -- as the most "undervalued" housing market in the country in this year's first quarter. So, as the real-estate market cools along the East and West Coasts, are savvy investors racing here to buy every house in sight?

On a recent afternoon, there was little sign of a stampede.

Janet Higgins, a veteran real-estate broker here, drives a visitor past a four-bedroom home custom-built seven years ago, with marble floors and a "gourmet" kitchen. It is on sale for about $420,000, down from $440,000 last year. "It's a wonderful house," Mrs. Higgins sighs. "It's got all the whistles and bells." But she says it is tough competing with new homes on the edge of town. A few hundred feet away, she points to another mini-mansion: "This house they almost gave away."

Open thread for Real Estate Industrial Complex members to defend their profession

Give it a whirl. Show me how I'm wrong, that the whole system isn't corrupt and in need of Senate hearings and regulation

Survey: Baby boomers own 57% of all second homes, but 75% not prepared for retirement

HP survey reaction: The baby boomer generation was the greediest, most self-centered generation in the history of mankind. Period. And they're heading for some awful reality now that they've spent all the money.

HP survey reaction: The baby boomer generation was the greediest, most self-centered generation in the history of mankind. Period. And they're heading for some awful reality now that they've spent all the money.

Yes, there are many wonderful, decent baby boomers who rejected the me-first, over-consumption, debt-fueled, screw-the-next-generation mentality of the majority and their leaders, although I don't believe history will be kind to this generation as a whole.

Especially when in comparison to the Greatest Generation. And especially when they're out looking for (even more) government handouts as the housing market and stock market collapse.

Get ready for some serious generational warfare. And some serious baby boomer strife. I'm not sure how we, or they, dig ourselves out of the problems they have caused.

Though the baby-boomer market remains a significant source of buyers for Realtors and builders, David Lereah, the association's chief economist, said marketing to this generation has been and can be a challenge.

While boomers appear to have "an almost insatiable desire" for real estate, many have not adequately planned for retirement, Lereah said.

"What should not be overlooked are the discretionary spending interests of this generation, and their appreciation of housing as a great investment," he said.

A Realtors association analysis shows baby boomers are proportionately more active in the second-home market, owning 57 percent of all vacation/seasonal homes and 58 percent of rental property.

Only 29 percent of the boomers surveyed said they were not at all likely to work after getting Social Security benefits, while three in four said they are not financially prepared for retirement.

Questions for HP Homeowners and HP Renters

HP Homeowners: Do you go to bed wishing you had sold, and fearful that you are losing paper wealth every night?

HP Renters: Do you go to bed with a big sh*t-eating grin on your face, knowing that homeowners are losing paper wealth every day while you rent their homes for pennies on the dollar?

A chainsaw I'd say: Buyers know they have edge

You thought realtors were unpopular today? Well, blame the messengers, they're likely telling homeowners across the country, and Phoenix, to rapidly and significantly lower their asking prices if they want to find a sucker (oops I meant buyer).

Lowballs are likely the only offers being seen in some areas too - especially Phoenix, Vegas and Miami...

Here's an article from the real estate hellhole of Detroit. I love the realtor quotes. Why dear god why does the MSM do it?

Metro Detroit home buyers have the edge over sellers right now and they know it.

"The market is positioned a little more in the buyer's favor right now," said Jeanette Schneider, vice president and co-regional director of RE/ MAX Southeastern Michigan. "With many homes on the market to choose from and favorable interest rates, the time is right for buyers to find the home of their dreams."

In both Oakland and Wayne counties, 18 percent of homeowners said they expect their homes to sit on the market for at least five to six months once they list them. That was the most-given answer in both counties.

In Metro Detroit, homes are taking four months to sell, on average, according to RE/MAX. The higher the asking price, the longer a home takes to sell, in general.

"The misconception held by many is that the real estate market is doing poorly and has hit a slump," Schneider said. "The truth of the matter is that, in recent years, the market was at a record high. Today, the market has leveled out and is back to normal market levels, which are still impressive numbers."

Homes sat on the market for an average 113.3 days in the first quarter, compared with 69.7 days in first-quarter 2005. The number of homes on the market at the end of the quarter was 16,795, versus 11,006 at the end of firstquarter 2005.

When the music stops - KB Homes announces the end of the speculative housing bubble

Builders selling to speculators fueled the fake numbers. Now builders are competing with the very speculators who bought their homes to see who can dump their inventory (without fire sale pricing) the fastest.

The builders will blink first, racing to the price needed to move the inventory. They can absorb the hit as their profit margin is much higher than Billy the Speculator.

But the builders' stocks are sure in for a ride, and we'll see consolidation now in this arena...

We are now operating in a more difficult market environment," KB Chairman and Chief Executive Bruce Karatz said in a statement. "The country's current-year home sales will likely fall well short of the record rates we have seen in the recent past as the market works through inventory build-ups, including a spike in investor/speculator resale inventory, higher interest rates and higher cancellation rates."

New orders during the quarter fell 19 percent to 9,908 chiefly from more prospective buyers canceling their orders.

"These conditions will likely persist at least through the remainder of 2006," Karatz said.

Subscribe to:

Posts (Atom)

{kind=link}

{kind=link}