Nice job housing doom with the charts again... And to think this Commerce Department and NAR data price this week didn't even include the cash-back-after-closing or massive incentives being used to move dead inventory. Now THAT graph would've truly shocked America.

Nice job housing doom with the charts again... And to think this Commerce Department and NAR data price this week didn't even include the cash-back-after-closing or massive incentives being used to move dead inventory. Now THAT graph would've truly shocked America.

But then again, I don't think they can handle the truth.

December 29, 2006

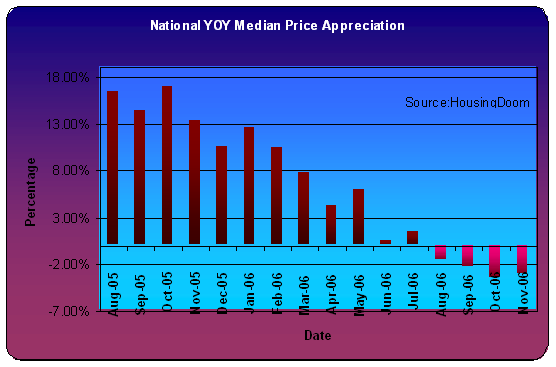

A picture is worth a thousand real estate clerks - here's the graph the NAR or MSM didn't want you to see

![]()

![]()

Subscribe to:

Post Comments (Atom)

52 comments:

looks like a 10% total drop in the last 4 months. Makes sense, my home sale is in the November data & I had to cut price by 35k on a 385k home to get a buyer.

Just means in debt, paycheck to paycheck, Americans will hold off on selling thier homes until prices rise this spring.

The will allow the developers to dump more inventory ASAP and the suckers holding off will take more of the price declines this spring.

Keith,

Would you mind if I rant a little bit on the Orwellian language used to keep the FB'd sheeple blind and ignorant and then show what it REALLY costs to live in a McMansion (McM)?

Thank you.

Let's begin with the Orwellian language and my pet-peeve: the term "Homeowner".

There are NO "homeowners", only "homedebtors. Until one finishes making the ALL of the 360 monthly payments (and assuming NO re-fis!), he or she cannot even begin to pretend to be a "homeowner".

Furthermore, should the sheep ever actually pay all 360 payments, they then become serfs, forever paying property taxes to the state for the privilege of living in the STATE'S property.

Next, let's destroy the "appreciation" myth. When one is dealing with ANY "asset" (in the business sense, which I will explain in a moment), that asset is typically put on a DEPRECIATION schedule.

The reason for this is physical assets wear out, break down, and generally rot, the longer they are in existence. A prime example of this depreciation can be found in business, and specifically the IRS code for commercial property. Even the less-than-generous IRS recognizes that a building is falling apart, day-by-day, as time goes by and allows the holder to deduct from his or her taxes the amount of money the property is losing in value each year.

Therefore, the term "appreciation" (as used by the REIC) is nothing more than a lie as the house is actually slowly decaying. In fact, this "appreciation" is nothing more than the reflection of inflation/debt creation that is manifest in the PRICE of the house, not it's "value".

Finally, there is this whole notion of "profit" that FB/Sheeple BELEIVE they have enjoyed as real estate PRICES (not values!) have gone up, due to the afore-mentioned inflation/debt creation.

My response is: Oh yeah? Here's a little homework assignment for you:

1. Total up all the checks you wrote to live in the house, beginning with the down-payment (if any these days), then moving on through the closing costs, PITI, maintenance, upgrades, HOAs and extra furniture you bought.

2. Subtract the paltry tax write-off for interest deduction (about one-third of the actual amount of interest you paid) and for property taxes (another one-third of the amount paid).

3. Now, take that final number, which is the actual, net, out-of-pocket amount of money you have paid to live in the McMansion and deduct it from the actual, net (after all REIC commissions and fees for selling the house) amount that you received when you sold the place.

4. Betcha it ain't what you thought it would be, is it? In fact, you might have actually PAID in more than you got back, especially if you bought in the last three years or so, and DOUBLY ESPECIALLY if you weren't lucky enough to live in a "Bubble Central" state like CA, MA, or FL.

Now, to be fair, one should also factor in what it would have cost to rent an equivalent place for the duration that the FB/sheeple lived in the house during that same period of time.

So, let's do a quick calculation, shall we?:

1. FB/sheeple puts 10% down on $220k MCMansion, pays closing costs of $3k. (That's $25k out of pocket going in.)

2. Sheeple stays in home five years, pays approx. $1000/mth PITI (figuring fixed-rate 30yr loan, at approx. 6% interest.) (That's another $60k out of pocket.

3. Sheeple also fixes a few things, pays reasonable HOAs of $100/mth, and adds some furniture over that five-year period (Another $25k or so out-of pocket over five years, and that's cheap by my calculation).

So, so far Sammy Sheeple has paid:

$25k to get in the McM.

$60k in PITI

$25k in other stuff

$110k total to dwell in the state's McMansion for five years.

As previously mentioned, the sheep DID get to take the mortgage interest deduction, so we subtract about $20k from the $60k PITI (Figuring interest paid of about $40k times the tax bracket of about 30%.), so now the total out-of pocket is $90k.

Now, let's say the sheep sells the house after five years. And to be fair, let's say the house inflated in price to $300k.

After deducting REIC commissions and fees, the FB sheeple walks with $282k.

Man, are they happy or what?

Oops. Did they forget that there is that little matter of the outstanding balance on the mortgage?

Which is STILL virtually at $200k?

Back to the math board one more time.

So, in summary, here is the financial picture:

Total money out:

ALL check written to dwell in the state's McMansion:

$110k

Less tax deductions:

($20k)

Total out-of-pocket expense:

$90k

Now, onto the sale of the McM:

Total net in-the-pocket:

$282k

Less the balance of the mortgage:

($200k)

Net proceeds:

$82k

Less all the checks the FB/Sheeps wrote to dwell in the state's McM:

($90k)

Net Loss:

($8k)

Again, to be fair, if the sheeps rented an equivalent house for, say, $1.5k/mth, they would have paid $90k, but they would have had NO large down-payments, no illiquid house on their hands, and total flexibility to move on short notice.

So, the FB/Sheeple MIGHT have a case to make here.

except for one other issue:

What if the price of the McM actually went DOWN in the ensuing five years since the sheep moved in, which is happening now?

THEN the numbers above are far, far worse. If the McM drops in price from $220k to $150k, then the FB just paid a total of almost $60k over the five years, which is getting awfully close to the rental amount paid by the carefree renter. And it gets MUCH worse in bubble areas where the houses are losing $100k, 200k, $300k. These FB/sheeple/homedebtors are truly in deep trouble.

In any event, I could go on and on with this premise (and I laready have!), but you get my drift here.

Finally, I urge all the "Flying-Monkey-Jealous-Bitter-Renters" (FMJRBs) on this board to slap every silly FB/sheeple/homedebtor on the planet with the above issues. Not that it will do any good, mind you, for it would be tantamount to reading Shakespeare to your dog.

But, hey we gotta at least try to educate the herd...

Less

First and foremost, it's all about the derivatives markets! Anyone else just hear the Richard Todd interview on CNBC with Steve Leisman? Find the transcript... and PREPARE!!!

PS You'll be telling your grandkids about the government and derivatives-- just don't tell them you spent so much time back in the day arguing about housing...

Subtext to graph (courtesy of the REIC public education division):

January 06: Prices up from last month! Bust? What bust?

May 06: Prices up from last month! Bust over!

July 06: Prices up from last month! There's never been a better time to generate a commission!

November 06: There was a brief pause in year over year price appreciation, but now the bust is really over! The sales are up from last month! Bust over!

What a great post butch.

Thanks.

Richard Todd should be Randall Dodd... oops!

Butch, $1500 a month to rent a $220K house? You're letting the sheeple off too easy. You could rent a $400K house for that much. I currently rent for $1200 a month. The same model across the street is listed for $350K. (However, it's been sitting there empty since last summer so maybe $350K is an overestimate of its true value)

First and foremost, it's all about the derivatives markets! Anyone else just hear the Richard Todd interview on CNBC with Steve Leisman? Find the transcript... and PREPARE!!!

Friday, December 29, 2006 1:43:12 PM

=================================

I'm amazed that this mass of paper called derivatives have not melted down by now. It appeared in 1998 LTCM crash that the whole thing was headed for collapse. And it should collapse! They are just side bets with no equity behind them what so ever.

There must be $700 trillion in notional value world wide. Has this planet gone insane? By the look of the derivatives bubble I would have to say yes.

If I may...

Chapter 2:

They believe rents never go up. Yet they are also convinced hyperinflation is around the corner and are buying gold like nobody's bidnez.

So they think ther $1200 rent will still be $1200 in 10 years while also convinced the dollar will be worthless.

-------------------------------------

U-Know's Guide: How To Spot The Under-50-IQ Crowd.

Chapter 1

They use words like "sheeple" and "fiat currency."

Stay tuned for Chapter 2!

"...and are buying gold like nobody's bidnez."

I bought gold like nobodys "bidnez" when gold was sitting at $274, now retired...

Oh stupid me, with low IQ.... HAHAHA ROFL!

The fed can "print" $700 trillion with the flip of a switch. What is everyone so worried about? When that money finally trickles down we'll all be rich.

There is a time and place to buy a house. That time is not now. The time probably will be in a year or two after all the people you sold houses to with toxic waste loans and 2-3x inflated prices get foreclosed upon and are moving into shelters and mobile homes.

The term of my rent (which currently costs 1/2 to one third the cost of ownership of the same house) is for 1-2 years. If the hyperinflation kicks in, I buy a house (and the rent payment I owe gets inflated away-- or I sublet for more than my rent). If deflation kicks in, I sign up for another year of rent and watch all of the bubble-toppers die an even more agonizing financial death, waiting to swoop in and feast on the fiscal carcasses.

I sleep very, very well at night, thank you.

The only factor, and it's a huge one, that might bail out the screwed house buyers is massive inflation as the Fed tries to save the economy. All assets will rise in value as the money value is destroyed. Debt will be wiped out as the money owed becomes easier and easier to come by. This is assuming any inflation also results in pay raises it has NOT in the last few years. The "CPI" number used to give "cost of living increases" to workers is completely rigged and doesn't reflect the true increase in costs of living.

I had a friend who "went away" for a year. He just commented how expensive things got while he was away. Things like burgers and fries.

Those of us who have stayed here are like the proverbial frogs in a slowly increasing-to-boiling pot of water. We aren't noticing we are being reamed because it's happening slowly.

I own a home and sleep like a baby myself. Difference between us is I wake up in a beautiful home every morning, you wake up in a 1 bedroom apartment.

Actually I probably sleep better since your mexican/black neighbors above, below, to the left, and to the right probably keep you up blasting the maricachi or rap music.

Oh yeah the In N Out #1 went from $3.99 to $4.29 this year, crazy huh? Oh wait it was $3.99 in 2002 and stayed the same price in '03, '04, and '05. So in 4 years it went up 7.26%...WOW!!!

And holy shit my cable modem just went up from $39.99 to $41.95 a month. Outrageous!! But ding dang it, it was also $39.99 in 2002. How dare they raise the price 5% over 4 years?

And still with this hyperinflation none of your rents has gone up. Interesting.

----------------------------------

"I had a friend who "went away" for a year. He just commented how expensive things got while he was away. Things like burgers and fries."

>> There is a time and place to buy a house. That time is not now.

Bunk. I just put my home up for sale (Central Ohio), and have 2 showings tomorrow. People ARE looking. Stop with the doom & gloom...

Central Ohio... hehe

No wonder she's such an angry bitch.

Or maybe it's the excess fat bulging from the arm pits chaffing.

WAAAAAA!

I own a home and sleep like a baby myself. Difference between us is I wake up in a beautiful home every morning, you wake up in a 1 bedroom apartment.

Actually I probably sleep better since your mexican/black neighbors above, below, to the left, and to the right probably keep you up blasting the maricachi or rap music.

_________________________________

Guess again. The 'rental' I live in is a 6 bed, 3.5 bath 3000 sq ft house in the best neighborhood in 30 miles. Living there for between a third and half the housing cost of ownership makes me wake up with a smile on my face every morning.

And I'm sure none of those music-playing folks you alluded to would ever have the audacity to move next door to your home and disurb your sleep.

>> There is a time and place to buy a house. That time is not now.

Bunk. I just put my home up for sale (Central Ohio), and have 2 showings tomorrow. People ARE looking. Stop with the doom & gloom...

________________________________

Best of luck to you Central Ohio. I truly hope you are able to sell soon and get out near the top. The two greater fools, however, have to take their chances.

I personally have looked at about ten houses in the last two months. Though asking prices here have dropped by 25k-50k since the summer, they still have not met my price point and will continue to look.

Met your price point? Why are you looking for a particular price? The right time to buy will be when the sale prices bottom. If you buy too soon, you'll lose money as the value of your new purchase continues to decline.

Renting has gotten cheaper. In the early 90's before I owned a house a 2 bedroom in Los Angeles was 1200/mo and they wanted first, last, and security deposit to move in, 3600 total.

Last year I rented an apartment close to a contract site where I was working. The rent was the same $1200 for a two bedroom but they only wanted $300 in addition to move in, not $2400.

That shows the desperation to rent has increased. The ratio of abodes to people is going up rapidly. Prices will come down to meet demand.

This is at least the third time Lereah has declared a bottom:

http://tinyurl.com/sfexb

David

David Lereah Watch

"Bunk. I just put my home up for sale (Central Ohio), and have 2 showings tomorrow. People ARE looking. Stop with the doom & gloom...

"

Looking, is ALL they are going to do! The best time to sell, was LAST YEAR.

I have my home up as well. It's been for sale since mid-October. From then to 1st week of December I had 2 showings. Since Dec 10th, I've had 4 showings. One of them ended up buying down the street. I know the owners and the house as I have been there a couple of times. Basically the same house as mine but with an extra bedroom whereas mine has an open den/study in that space. I think the open option looks a hell of a lot better, but oh well each to their own.

My asking price is $495,000. Buyer agrred to $485,000 and it was listed at $499,000. Closing in late January.

I know until I actually sell doesn't matter if I have 2 or 200 showings. But to go from 2 showings in 2 months to 4 in 2 weeks is encouraging.

I have my home up as well. It's been for sale since mid-October. From then to 1st week of December I had 2 showings. Since Dec 10th, I've had 4 showings.........

_________________________________

Good for you and I hope your home sells at a price agreeable to you.

But also consider that this represents a 3% price drop in the two month period the domicile has been on the market. Also realize that many people have extra time to fill in during the vacations that many people take during the holidays.

Best of luck in selling your house.

I have my home up as well. It's been for sale since mid-October. From then to 1st week of December I had 2 showings.....

-------------

Not to mention that the house they bought technically has one more bedroom than yours, and may be able to commmand a proportionately higher price.

I'm not saying it's going to sell tomorrow, I said things are looking better now than they did a month or 2 ago.

I bought the thing for $200K. If I have to drop the price to $450K, it's not the end of the world.

As for the extra bedroom, yeah I guess you're right, although my lot is bigger which should even things out.

Dnd how do you figure a 3% drop, based on selling to asking price ratio? Listing price is irrelevant. What counts is the sales price.

>> they still have not met my price point and will continue to look.

Oh, so somehow because it's YOUR number, it's right?!? Neither your price, or the owner's asking price, have anything to do with reality. Let me guess: your "price point" has something to do with comps, right?

I'll be SO glad when this madness, including "comps", is over...

apartments are going begging around here (north of Boston). some rents are too high--there's a huge new complex in Woburn that looks half empty probably because they want $1450/mo for a 1br which is absurd, and it's right on I-93 with all the traffic noise--but overall they're stable.

if you look on craigslist the same apartments are listed for weeks. I'm moving from Malden to Lowell next month for a much nicer apartment that's $100 less with $500 security and a 10-minute commute. I talked to a condo flipper trying to rent his place and it sounded nice but he couldn't afford to wait til the end of January and there's no reason for me to pay rent on two places. sucks to be him I guess.

They are converting condo projects to apartments here in OC, not to mention the brand new 3000 sq ft investor owned houses that can be rented cheaply in the next county over. I don't see rents going up here.

This is the worst time of year to sell a house. I would disregard any statistics. However, how anyone can expect prices that are so far out of whack to continue upward is dreaming. Things will not be nice and smooth either. Housing panic is named right.

Even though it's the worst time of year to sell a house, I'll bet it's as good as it's going to get. Come spring when the expected resurgence fails to appear, that is when the true panic will start.

*****NEED SOME HELP*****

I am testing the waters with foreclosure listings in my area. From what I have read here I should take late 90's values, etc. and then add some sort of percentage to reach a stable market value? I'm not sure if I understand how to do it correctly and would like some help on this. How would I figure a stable market value for a home sold after 2000 at an inflated price, that is currently in foreclosure? Any help greatly appreciated. Will post back as to what sort of replies, if any, I get from banks. Hahahahaha

Butch,

Great job! I really enjoyed reading your post.

Therefore, the term "appreciation" (as used by the REIC) is nothing more than a lie as the house is actually slowly decaying.

---------

Thank you jesus! try telling that to the face of a homedebtor! if they don't try to punch you in the face, they will storm away in a huf!

anon

Basically the same house as mine but with an extra bedroom whereas mine has an open den/study in that space. I think the open option looks a hell of a lot better, but oh well each to their own.

--------------

guess you were wrong huh?

Not much difference between a home debtor and a renter. Renters get ready to pay through the nose as the bubble bursts. Added demand for housing will increase your monthly cost.

Just to back up those whose rent hasn't increased at all, I personally have been in the same 1,200 Sq foot apt. in Boston paying $1,200/mo for the past 6 years.

Simply have a landlord that is very cool and appreciates the fact he has my check in time every month and I never bug him.

Hell, I buy the guy Xmas presents every year.

He told me he'll never raise rent on me either. Naturally, he could change his tune but even if he did I wouldn't complain too much.

If I were to actually BUY my place right now, it would probably cost me $475K and I'd probably be paying 3X my rent payment.

Central Ohio-

I'm "looking" here in WA. State too, as are some of my friends.

We are observing prices going down from month to month. It warms our hearts.

When stuff gets cheap enough - 2 to 3 X income- we'll all buy.

It's got a ways to go! But it sure is fun looking and watching prices gradually creep down!

Rents are falling near me as empty homes become rentals

rent will not go down in Chicago. TOO MANY CONDOS!!! Flippers got caught. They will need any kind of income.

"And still with this hyperinflation none of your rents has gone up. Interesting."

In Weimar Germany, the government imposed rent capping.

Although the price of bread went from 1 mark to 37trillion marks in the space of 3 years, rents stayed the same.

Another nugget of useless info is that although people paid off their mortgage for less than the price of a loaf, once stability resumed, they were taxed the shit out of.

If you think that because the price of computers have dropped lately there's no such thing as inflation, you're living in a fantasy world.

If the price of raw materials doubles (and they have) you can't keep selling finished goods at the old price.

There comes a time where either to stay in business you have to pass on increased cost to your customers (which is inflationary) or you go out of business, thus causing a reduction in supply (also inflationary)

Oh so now we're in Weimar Germany. OOOOOOHHHHH KAAAAYYYYY

Oh so now we're in Weimar Germany. OOOOOOHHHHH KAAAAYYYYY

================================

I would agree that that is an accurate analogy. The money supply just keeps getting bigger. This was the bankers policy response to the collapse of LTCM in 1998. They went with what they called a "Wall of Money" policy to keep the financial system from collapse.

Bill Clinton and Robert Rubin had a different policy as stated by Clinton in September 1998 at a presentation at the CFR. In response to learning that Clinton intended to take the bankers system from them they responded with Monica Lewinksy and the impeachment.

Thats real history folks!

(Note: In the following text "billion" equals 1,000 million.)

(begin transcript)

THE PRESIDENT: Thank you very much, Pete. Hillary and I are delighted

to be here with you and Joan, and I'm glad to be joined by Secretary

Rubin and Jim Harmon, Gene Sperling, other members of our team. I'm

glad to see Dick Holbrooke over here. I hope, if we can overcome the

inertia of Congress, he will soon be a member of the team again.

(Applause.) And I thank David Rockefeller and Les Gelb and others who

welcomed us here today.

The subject that I want to discuss -- let me just say one thing in

advance -- I'm going to give you my best thoughts. We have been

working on this for three years at some level of intensity or another,

going back to the Naples G-7 meeting in the aftermath of the Mexican

financial crisis. I have done everything I could do personally to

reach out across the country, and indeed across the world, for any new

ideas from any source. I'm going to give you my best thinking today

about what we can do, but I want you to know that I'm here, and if I

had my druthers, this would be about a three-hour session where I'd

give this talk and then I would listen for the rest of the time.

So I want to encourage you, if you think we're right, to support us.

But if you have any ideas, for goodness sake, share them, because I

agree with what Pete said: this is the biggest financial challenge

facing the world in a half-century. And the United States has an

absolutely inescapable obligation to lead, and to lead in a way that's

consistent with our values and our obligation to see that what we're

doing helps lift the lives of ordinary people here at home and all

around the world.

From Sept 14, 1998 Council of Foreign Relations i.e. Bankers

Phoenix metro market. A friend just closed on new construction.

Listed 172,900. Sold 125,000. Had to close by last thurs. at 11 am. Year end close-out.

Condo?

-------------------------------------

Listed 172,900. Sold 125,000. Had to close by last thurs. at 11 am. Year end close-out.

(re:Phoenix market sale)No not a condo. A house.3 beds, two baths.

East side of metro area.2k down.

new house for $125K? Sorry I call bullshit on this one.

Post a Comment