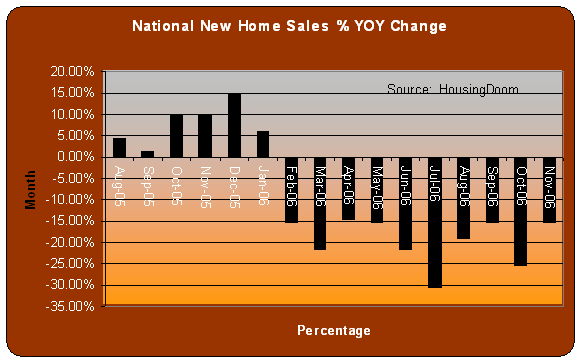

Here's a look at the awesome rise in new home sales celebrated by the REIC-advertising-supported MSM yesterday, care of the consistently good housingdoom:

It's funny when the MSM use change vs. prior month sometimes, and change vs. prior year other times. It's called spin. And I call this one hell of an ugly chart no matter which way you read it...

December 28, 2006

New home sales up! Party on! Good times are here again!

![]()

![]()

Subscribe to:

Post Comments (Atom)

51 comments:

So the real headline should have read "New Home Sales Plummet 15%!"

Wow

Anonymous said...

I have some confusion over the reported 3% gain in sales.

Seems to me that price increases are reported year over year, or at least they were when prices were going up.

I thought the same was true of sales. Don't they normally report YOY sales? It would seem even more important because of the higher volitility of sales related to seasonality. Now I'm hearing sales are up and they seem to be reporting versus last month and not year over year?

Is this a case of moving the yardstick so that sales look better?

Yes, YOY home sales dropped 15%, but the MSM spun it against last month, whereas they increased 3% (from down significantly the year before)

In other words - a total joke and irresponsible reporting at its best

Sickening. I hope the REIC advertisers gave the MSM a nice year end bonus

Year end, or rear end?

A real no brainer. Interests rates went back down around 6% and huge incentives to dump the massive inventory. We'll see how long the spin and revival lasts...

How about the other headline story? Mortgage activity plummeted again as soon as rates rose...

The press should do some research to see if the REIC is playing around (steering) with closing dates to create some good months here and there...

When that story hit the MSM yesterday, I didn't even bother to read it, because I KNEW the spin - when I drove to Las Vegas from SD over Thanksgiving, it was like the Harrods Christmas sale on the I-15 from San Diego to Henderson, NV. Lennar and KB, etc. had huge signs, baloons, givaways (who knows what - hookers, drugs? Hawaii Vacations). . .no downpayments, no payments for a year. Of COURSE new home sales are up. . .people probably bought for a Hawaii Vacation, and will turn the deposit back on the house next month. . .or more likely be a "first mortgage payment default"

Speaking of sales - just came back from Globus . . .wow - 1/2 on a nice Swiss Ski jacket. . .now if there would just be some snow in the Alps.

And yet the Population falls into this BS,, Housing The Dumbing of Society.

But hey if you can Refi out of that toxic mortgage do it now!!No!, no cash back just a term refi...its great to get that check..but it sucks to have to pay it back.

Patch said:"How about the other headline story? Mortgage activity plummeted again as soon as rates rose..."

I saw that. Sounds like the consumer is locked up in debt. Whats going to happen when interest rates have to go up?

Is it possible the fixed rate wont ever get higher than 6.75% when just 10 years ago, 8.25% was commonplace?

HOUSING MARKET IS COLLAPSING IN 2007 !!!

wATCH THE Forbes video: Prof. G. Schilling talks

here

http://www.forbes.com/video/?video=fvn/moneymasters/vj_mm122806&partner=yahootix

The problem is, always has been, prices, not sales. If prices are falling there is no speculative demand. There is less REFI activity possible. Fewer dollars for Hummers and flat screen tvs. People will be underwater in their mortgages.

Whoever is buying now, when prices are falling, has less brains than Terry Schiavo.

Yes Keith. American homeowner, bend over for your Real Estate bonus. Would you like some Vaseline with that?

REUTERS: Florida's overbuilt condo market starts to fizzle

By Jim Loney

MIAMI, Dec 28 (Reuters) - On a piece of prime bayfront property near downtown Miami, weeds climb the steps of the sales office for Onyx 2, a planned waterview condo where apartments were to sell for $500,000 to $2,000,000.

A sign reads "For Sale. Land, plans and permits for Onyx 2. Includes fully equipped sales center."

Three blocks north, the land on which a glassy loft-condo called "Ice" was to rise lies idle. A realtor's Web site says: "This project has been canceled and will not be built."

Developers have pulled the plug on some of Miami's most anticipated condominium developments, a sign the city's sizzling, speculator-driven condo market -- where prices of many apartments doubled or tripled in a few brief years -- has finally chilled.

"This market was too good to be true," said Lewis Goodkin, a Miami economist and real estate analyst. "But it was a market fueled by speculators, so it wasn't a true market."

City officials say 15 condo projects, representing nearly 1,900 units, have been officially pulled from the waning market. But analysts say the numbers are much higher when you consider the rest of Florida's overbuilt condo market.

Miami's building boom, the biggest in the city's history, is far from over. Construction cranes dominate the skyline, as they have for years.

The city of Miami alone still has more than 77,000 units, in nearly 300 projects, under construction or in planning.

But the "for sale" signs are not the only warnings of a fading market.

Statewide sales of existing condos dropped 31 percent in October from the same month last year, according to the Florida Association of Realtors. Median prices fell 2 percent.

In Fort Lauderdale, sales dropped 21 percent in October.

The seller of a Miami Beach waterfront one-bedroom dropped his asking price from $445,000 to $400,000 to $370,000 in a matter of weeks.

POSTER CHILD FOR OVERBUILDING

"We're starting to see projects being canceled almost on a weekly basis," said Jack McCabe, chief executive of McCabe Research & Consulting of Deerfield Beach.

Miami was considered one of the most speculative markets in the years-long U.S. residential real-estate boom. Analysts said up to 80 percent of sales at some condo projects were to speculators who intended to quickly resell, or "flip," the units.

Elie Mimoun, sales director of Midtown Miami, a $1 billion-plus redevelopment of a blighted former railroad yard north of downtown, said the softening represents a natural shakeout of speculators.

"The market is now keeping out the crazy people," he said. "I think if the economy stays the same, the worst is behind us."

Midtown Miami, a key cog in the city's redevelopment plans, is a 56-acre site where developers plan to build more than 3,000 condo units, office space, and some 600,000 square feet of retail shops. Of the nine planned condo buildings, three are under construction and another breaks ground in February.

Midtown's developers offered part of the project for sale this year for $375 million, which some took as a sign they were looking to escape a faltering market.

But Mimoun said the developers were simply trying to find a financial partner and "there was never a question of getting out completely."

Mimoun and other optimists believe the unusual demographics of this Latin-flavored city will keep the Miami market strong. About 20 percent of his buyers are Europeans whose spending is bolstered by a strong euro, and 13 percent are South Americans, traditionally eager consumers of Miami real estate.

But Goodkin said rising building costs, hurricane-fueled homeowners' insurance hikes and property-tax increases caused by exploding prices have made Florida increasingly unaffordable.

"You have to have people buying units to live in. Who are the speculators going to sell these units to?" Goodkin said.

Several years ago, McCabe began mustering funds, or "vulture" capital, to buy apartments when the bubble burst. But he has not yet begun buying and said it may take 5-10 years before prices bottom out and begin to rebound.

What's that smell?

T'is Christmas time grandinquisitor. Be of good cheer.

3% per month price decrease, is, hmmmm let's see, 48% per year!

That's a crash.

The sales slowing down was the result of prices being too high. Sales speeding up means prices are falling and it's prices that we are concerned about.

borkas upper lip!

Ooops, 36% a year. Still a crash. No, your math sucks.

3% per month = 48% per year????

What calendar are you using sport?

DOH!

Hmmmm. Market refuses to acknowledge good news about housing. All indices down.

Is this the beginning of the end? Of Western Civilization I mean. Granted, that's a worse case scenario.

I guess I should have said, "You do the math".

The NAR released the numbers on existing home sales. Original Press Release is at :

http://tinyurl.com/y6e9oe

The spin in the MSM focuses on the month to month number, an increase in sales of 0.6% in Nov. over Oct.

To their credit, while the NAR states this number, in the SAME sentence, not hidden way somewhere deep in the release, they state that the YoY was -10.7%.

Perhaps its the MSM that's at fault here, not the trade associations at all - certainly in their written statements. Its the breathless, credulous, boosteridiots in the MSM that distort the narrative and visual patterns behind the dry numbers.

Conspiracy or Cockup ? I veer towards ignorance at this moment. Perhaps all the bright, top of the class journalists go off to do social injustice, political news, whereas the 3rd rate, lazy, ,dumb, kegsters ones do business news ?

The ones who fail to graduate probably go and become local news anchors...

-K

The FAREC (Florida Assoc. Real Estate Clerks) have further fudged their numbers for Jacksonville. Their latest numbers show a 19% YOY decline in existing home sales and the same YOY median price. All numbers have been adjusted and are the final numbers.

Well... If you pull out the numbers from 2005 and do the math, the actual numbers that they reported show a 27% YOY decline in existing home sales and a 4.21% decline in YOY median home prices. I keep track of the reported numbers each month and this is the first "mistake" they have made in all of the numbers I have (since 2000).

There was a huge marketing push for home sales here in JAX over the last two months. I don't think they wanted to show a loss after their huge campaign so they fudged the numbers to show a wash in prices. It's rediculous.

Here's a good article from Clinton's top economic advisor, painting a very different picture about housing inventories and what 2007 may hold for housing and the economy in general.

http://tinyurl.com/ydxhmf

This is a dead cat bounce.

"It's rediculous."

What is truly ridiculous is the level of spelling here.

3% drop month over month doesn't translate to 36% per year and certainly not 48%.

doh.

Why not? In HP land math is irrelevant. a 3% drop in a month can mean a 300% yearly drop if you want it to.

For once I'll say something good about David Lereah, because he's even came out and admitted this is going to be a huge problem. The press seldom mentions this:

"The slight drop in median home price was of little comfort to first-time homebuyers. The Maryland Association of Realtors’ First Time Homebuyers Affordability index rose slightly in October, the latest data available. The October Index was 44.9 percent, up from 44.5 percent in September. October’s index level means that the average homebuyer had only 44.9 percent of the income needed to buy the typical starter home."

"We welcome any improvement in affordability,” she said, ‘‘but when first-time homebuyers have less than half the income they need to become homeowners, it’s clear we are a long way from giving them the opportunity to buy.”

Until the asset returns to an affordable price, it's over, and it's gonna take a long time to go down. Or if it doesn't go down, then it's just gonna sit at its current price for the next 15-20 years. Take your pick...

Housing will not crash in nominal values.

It will however crash relative to gold.

Massive inflation will keep housing up,

as well as the stock market rising. However,

this will really be an illusion, caused by

the falling dollar. Most will not realize

it untill it is way too late.

-mc

A 3% drop every month for 12 months would be a 31% drop for the year FYI

http://www.cepr.net/documents/publications/forecast_2006_11.pdf

That report (above) says nothing about

money supply, which IS infaltion. Anyone

here have a clue what M3 is running at??

-mc

RE: M3

For those who don't already know, The Fed. stopped publishing M3 in Nov. 05 - their excuses were that to save money ( a lousy 500,000 year) and because it could be put together from other sources. Well big guys perhaps can but average Joe?

Nov. 05 is also when the money supply started accelerating.

Luckily shadowstats.com does out the M3 together. They've backtested the proxy measure and its got 99.99x% correlation to the real historic measure. Here's the tiny url link to their M3:

http://tinyurl.com/zyey9

M3 is running at 10%. Enough said - people should draw their own conclusions.

-K

Hmmm never thought of that. Wonder if I can buy, get the free Benz then cancel. Think they'll let me keep the car? Oooh even better. I report the car stolen, get insurance money, blow it all on a 3 day Vegas weekend complete with all you can eat hookers/drugs.

NICE!!

"no downpayments, no payments for a year. Of COURSE new home sales are up. . .people probably bought for a Hawaii Vacation, and will turn the deposit back on the house next month. . .or more likely be a "first mortgage payment default"

Keith says, "It's funny when the MSM use change vs. prior month sometimes, and change vs. prior year other times. It's called spin."

And HP is different? How many times have I asked people to look at statistics and try and put some perspective on the numbers instead of the SPIN and people refuse because it doesn't support their view?

If people won't use inflation adjustments for prices or cost to build per ft, comparing apples with apples, adjusting for population changes (eg Phoenix foreclosures numerically may be the highest since a given date but adjusted for population is still low). So everyone gives their own SPIN on what is happening because it seems most don't want meaningful discussion or search for truth but just to support their views.

My question is: will there be forclosures available to smart people, not the suckers who fall victim to discount real estate dreams, plunking down thousands of dollars to learn forclosure secrets? There are so many of these suckers -- I expect Casey Serin to turn his lemons into this kind of lemonade shortly. You heard it here first.

foxwood,

You are the lone voice of reason in this wilderness of fools. Thank you sir.

Thanks annonymous. Where you from? Why don't you pick a name? What is your take on where we are, where we are headed?

I'm glad there are lots of reasonable posts here and discussions that seek to find the truth beyond the hype.

I'm just now getting to that age where I finally get my parent's! Youth is blind and gullible. Now I understand how my parents could smile and say, "you'll get over her." or "things will always be someway."

I was a teen during the 70s stagflation/house bubble, a young adult during the Carter bust with high interest rates and then again in my late 30s with the 1989-1992 crunch so having seen the cycles and thirty years of doom and gloom and predictions of the end of the dollar, the end of our economy, the end of the world, a 36,000 dow, a 3,000 dow, and hype after hype, you finally understand why your parent's just smiled.

And this from the kid who told my parent's in the 70s, sell your house, the bubble is going to pop and you'll loose all that equity! Thirty years later they still live in that $17,000 house bought in 1962 that is now selling for a million and they smile as I say, sell that house! As far as they are concerned prices can drop 75% and they'd not be concerned nor would it be the end of the world...for them at least...maybe their neighbor who bought last year but who knows, maybe they'll be smiling too 30 years from now.

Foxwood,

I don't pick a name because it annoys the wingnuts. Silly I know, but what the heck.

My take is that the housing downturn is real. I am not some moron who thinks appreciation will be 20% a year every year. The housing market went up like a bitch in the past 5 years and it has come back some what. Depending on how you measure prices (using incentives, cash backs, free payments for a year, free Hummers, etc) prices have fallen anywhere from 5 to 15% from the peak of 2005 depending on the market. But we're done I think.

I see it like this. In 2004 and 2005 every magazine had a cover story about flipping. Time, Newsweek, Money, Business Week, you name it. At that point you know the exact opposite will happen. We are at the same point now only in reverse. Every magazine is talking about the downturn. This means the exact opposite will happen.

I'm not saying 2007 wil see 20% appreciation again. I predict a 1 or 2% appreciation nationally with some markets in low single digit declines.

Despite the spin here, sales of new homes were up 3% last month and resales were up 0.6%. If these numbers are questioned, then every number including the numbers showing a derease need to be questioned. If report X says 20% decrease in July sales and then the same report says 3% increase in November, you can't dismiss November's report while embracing July's. But that is exactly what has been happening here yesterday and today. It is intelectually dishonest and Keith & Co. know it.

Your parents' situation mirrors my parents. They bought a home in 1976 for $65,000 which was a lot of money for a house back then. They still live there 30 years later. If they wanted to, they could get $850,000 tomorrow. If they waited they could probably get $1M. Sure, I suppose a year ago they could probably have sold for $1.1M. But so what? They still have an aset that is paid off and is worth somehwere in the neighborhood of $1M. You think they're glad they didn't rent?

There are a few generally accepted facts of life. One of them is that over the long run owning a home is better than renting. The wingnuts here look at 2004 prices vs 2006 prices and say AHA!! owning is a bad idea, see renting is better. OK fine, for a 2 year period they are right. But I will bet that anyone who bought in 2004 will be glad they did in 2014 and will be doing cartwheels in 2034 like my parents and like yours.

Now speaking of parents, my in-laws are in town and I need to go start drinking heavily :)

'Youth is blind and gullible. Now I understand how my parents could smile and say, "you'll get over her." or "things will always be someway." '

Well, you're one of the lucky ones with nice parents.

My parents, however, never recovered from their business losses (and property foreclosure) during the late 80s. Nothing's ever been the same and the blame game goes on indefinitely.

So the indiscretions of youth (with wise parents who've seen it all), isn't a universal truism. Sometimes, 'from the mouth of babes' holds more truth than the all knowing parents.

Annonymous said, "ut that is exactly what has been happening here yesterday and today. It is intelectually dishonest and Keith & Co. know it."

Yes, totally agree. Does sound like your parent's and mine have showed us that eventually owning makes sense over renting. I know my friend in Phoenix who wouldn't sell his first home and twice lost a lot of equity looks smart now (not to say had he sold and reinvested he'd not had made more) that the house is five years away from a payoff and it is a rental so when he is 57 the entire rent will be income to add to his retirement.

My parent's told me three things, never divorce, never sell your first home, and never have children. Do these three things and you're guarenteed to retire young. I did two to them...no kids, no divorce! Sold my first house, and my second, third, fourth, fifth, and sixth, and seventh...no intentions to sell the current one even when I build my retirement home. I was in the AF so not much choice to sell my first home when transfered to Korea and then Germany as didn't really make enough money to take the risk of renting it out from a distance.

But agree about your comment about intellectual dishonesty and chosing numbers when they suite your agenda. I just want honest, balanced input to help guide my choices as well as honesty about local conditions and that not all markets are the same.

Sometimes from people responses you'd think I was saying home prices were going to rise 5 or 6% a year for the next ten years....in some markets and depending on inflation, maybe...but in general I think there will be markets that willl see 3-5% yearly declines for maybe five years mixed with higher inflation to offset their bubble values and other markets may appreciate at 1-2% a year and others not at all. Every market will be dictated by their current value and relationship to incomes and rents.

I'm just amazed that people talk bubble and then (now Keith) talk about buying in Tokyo? Give me a break. A 1500 sq ft house in Phoenix for $225,000 is a bubble but $250,000 for a 350 sq ft cracker box in Tokyo is a deal?

Keith stokes the issue because this blog makes money for him. He'd stoke it even if he were out flipping houses as it is just an angle for him to get a market in the blogsphere and advertisement money. If porn sells, sell it. If fear of a house meltdown sells, then sell it. If flipping houses sells, then flip houses.

I'd just expect those who come here to discuss the topic to be more honest.

House prices will only be buoyed by inflation if salaries and wages go up to pay for them. So far, I don't see anyone making any big wage gains. The Wall Street crack pushers are walking away with all the new money so luckily most of the inflation will occur in New York City.

I heard to day that 10,000 new jobs were created in New York city by Hollywood movie studios leaving LA and doing production in New York. That's 10,000 fewer jobs in Los Angeles. Oh my. Whose going to pay for all the houses that have tripled in value over the last 6 years.

Maybe the ultra rich will keep Belair and Beverly Hills going up the rest of this place is going to crash and crash hard. It takes 3 hours now to drive 60 miles on a freeway in the afternoon. All the people who live in Victorville but work in Los Angeles are plugging up the 15 freeway permanently.

3 month tresury yield was up 0.30 bringing it to 50.00

30 year up same to 48.10

Still an inverse curve.

Anonymous said...

foxwood,

You are the lone voice of reason in this wilderness of fools. Thank you sir.

Thursday, December 28, 2006 11:43:13 PM

Quit talking to yourself, foxwood.

How? The majority of the ads here are for mortgages and other real estate related services. How does he make money from click throughs for mortgage ads when all his readers are renters who think buying a home is financial suicide?

I've posed this question to Keith before with no reply.

-------------------------------

foxwood said:

Keith stokes the issue because this blog makes money for him

bozonian,

Did you grow up in a small town all your life where everyone walked to work or something? Your comment about commutes in LA baffle me.

My father commuted 35 miles to work into the city every day for 20+ years. He'd be out the door at 7:30am and home around 7:00pm. He was a corporate lawyer, made more money than God but still put himself through te bumber to bumper traffic. Living closer to the city meant living with blacks and that was not an option. Had nothing to do with affordability.

Why do people think that because the MSM is reporting the bust, that it must be almost over? Housing is sticky on the way down - this is common sense! OMG !! People remove their properties from the market/ rent them rather than sell. At some point, when things shake out further, people will be forced to accept reality.

Two other comments:

When bubble sitting renters start buying this will not increase demand by much... after all, they leave the rental house empty.

If people really want affordable housing (and prices dont drop enough) they will just leave the high cost coastal area en masse. It is already happening folks. We compete globally by decreasing our operational costs (salaries) which means we become peasants or the employers relocate.

Annonymous said, "If people really want affordable housing (and prices dont drop enough) they will just leave the high cost coastal area en masse. It is already happening folks. We compete globally by decreasing our operational costs (salaries) which means we become peasants or the employers relocate."

I totally agree with you. I think a lot of people on this site confuse their markets as the norm rather than the abberation. Kind of hard to feel sorry for those states that started this bubble and profited from it for the past 40 years (like California) and now complain about how expensive their homes are and that they can't afford them. Who in their right mind goes to an open house and buys a house they can't afford with interest only loans (many for some reason thinking that is zero interest) and then pays a premium over asking price and then cries when they loose money?

How many sane people would walk into Dillards and tell the sales clerk they want to pay a 20% premium on the shoes they are buying?

At some point American companies will relocate to lower cost cities. Now low cost alone won't drive say Wall Street away from New York nor will low cost cities like Detroit keep Ford Motor but at some point they move either overseas or to the interior of America. Of course government policy has a strong impack. How many have been given tax payer incentives to relocate within the USA or worse overseas?

Of course if there were a massive outflow to the interior then they just bring their bubble with them and ruin the smaller communities in America.

One reason I left Phoenix was that outflow from the midwest and California (yes, surprisingly the midwest sent more people to Arizona than California) was ruining the quality of life, increasing crime, congestion, air pollution and eroding the cost of living. The other was natural disasters. Katrina was a prime example of the disruption to other communites by the sudden arrival of displaced people. Houston took the brunt and still pays for it and Katrina isn't even close to what would happen if a 9.5 quake hit central LA. Imagine a couple hundred thousand refugees coming to Phoenix in a matter of days? And then the disruption in the supply chain? Most of our products and gas and food comes from LA. When the gas pipeline burst outside Tucson (gas from El Paso) Phoenix was plunged into a 1970s style gas shortage. Imagine that multiplied and lasting longer.

Still, there are plenty of affordable homes in at least 40 states to choose from.

Foxwood,

Usually you make sense but not this time.

1. You saw what Houston went through due to Katrina so to avoid that you moved to....AUSTIN? If a Katrina hits Houston, where do you think the refugees will go? Austin is the closest city to Houston. And if you're going to think like that, no matter where you go mother nature can mess you up. Hurricanes in the SE and TX. Tornadoes in TX, OK, KS. Eartquakes on the west coast. Blizzards in the north. Mt. St Helens. Anywhere you go, something could happen.

2. Most people don't have the luxury of moving at the drop of a hat. The millions of people on the coasts are there because of jobs. Silicon Valley, Hollywood, Wall St, colleges in Boston, government jobs in DC/NoVa.

Aaple and google aren't relocating to Omaha any time soon. Harvard or the Department of Energy aren't setting up shop in Des Moines. All those employees won't give up their careers to move to Omaha or Des Moines because they can buy a cheap home.

Sure there will be branch offices and things like that. But new tech companies will sprout up in NorCal. Movies will be made in SoCal. Elite colleges will be in the Northeast etc.

I agree with you Annonymous. And yes, I was aware of how Rita did force thousands of Houstonites to flee to Dallas and Austin (most went to Dallas/Ft Worth but I imagine that was because there were more places for them to stay. Not a lot of hotels in Austin to accomodate that many people. A reason I chose Austin. Also, as Baton Rogue saw people with money snap up homes after Katrina Austin seemed a natural place to buy for the same reasons.

I also agree that it takes longer than twenty or thirty years for most power centers to die and new ones appear to take their places and I have no doubts that SF, LA, Seattle, NY City, Boston, Chicago, will remain important centers of trade and job opportunities. For many on the up those are the cities to be, just like London or Shanghai. I'm 52 so my priorities are different now. Just want a nice place to live where I feel safe, secure, and a medium size city to live that won't get too big if I live to be 75.

I do agree that some people can't afford to move at the drop of a hat but those are mostly choices. It all depends on priorities and desires. If a person isn't ready to drop out of the rat race, the consumption race, the drive to make lots of money then of course you have to go where the money is. It takes money to make money and you are not usually going to make it in some small town.

Texas is also a power house in its own right. 23.5 million people and number one in actual numbers of people moving here though Arizona and Nevada are one and two for percentage since they have smaller populations. A lot of high tech firms continue to relocate here for quality of life and cost of living reasons and Austin has four outstanding universities and colleges plus a few others within commuting distance. UT Austin is a very respected college.

West Austin in the hills is as pretty as any place. Quality of life consistently has been ranked in the top ten, and frequently number one among cities of all sizes.

I worry that in the future it may not matter where any of us live in the USA or wether homes are affordable or if we have good schools or???? Our government has been off course for a long time and our national debt, our dependance on foreign oil, and I believe that our currency will bring us down quicker than home prices can collapse.

The forces at work in the world are not friendly toward America and we are doing nothing to save ourselves. France, the jealous sister and other european nations who have resented our domination of the world since WWII ended are anxious to see us fail so they can rise again to dominate the world. I fear less those countries that outright express hatred toward us like Iran. It is our so called allies I fear most.

After sixty years of helping rebuild a war ruined continent, helping to push for a United States of Europe, to pus for a unified European currency, that lion is ready to turn on us.

I've been amazed at our history, our folly. What other nation in the world has made other nations stronger at her own expense? Rebuilt her enemies (Japan, Germany, China), quick to aid others in need or disaster, to fight other peoples wars, to drain its wealth for what? Europe wouldn't have done the same for us.

How many humans throughout the ages have learned too late that once the fame, the power, the money runs out their so-called friends vanish?

2007 will be a year of dynamic change in the world. I feel 2006 has been nothing but the calm before the storm. Next year we could see major earthquakes, more hurricanes, a continued rise in the Euro as a major reserve currency leading to a decline in our dollar and increased inflation. A government intent on printing its way out of all its obligations and us becoming another Argentina.

That being said I recognize that anything can happen. Even as we see chaos in Iraq we fail to remember that 80% of Iraq is secure and that their economy is better today than under Saddam and so too here we'll have those who win and those who loose and those of us on this site are just trying to figure out how to stay afloat.

As much as I am cautious, usually optimistic seeing the cup half full rather than half empty all the events that have transpired, all the risks in the global economy that can go wrong, it is easy for me to succomb to the biblical verse "When they say peace and safety then sudden destruction shall come upon them.' Things on the surface look good over-all but who knows when that new car's engine could throw a rod and your stuck dead on the side of the road?

I hope 2007 is prosperous and shows the world move toward peace. But who knows?

Post a Comment