Not only am I amazed that "option-ARM" loans are legal, not only am I amazed that in some towns in California 40% of new loans were written this way last year, but I'm also blown away that Congress hasn't stepped in to try to stop this disaster in the making. The California legislature is now at least holding investigations...

Not only am I amazed that "option-ARM" loans are legal, not only am I amazed that in some towns in California 40% of new loans were written this way last year, but I'm also blown away that Congress hasn't stepped in to try to stop this disaster in the making. The California legislature is now at least holding investigations...

People who are not making the necessary payment on their home to cover the interest charges (let alone not paying anything toward principal), while at the same time housing values are tanking, are going to lose their homes, period. Nearly every one of them.

There will be so many foreclosures in California in the next few years, it'll seem like a neutron bomb went off in some cities - the people are gone but the buildings remain standing.

California lawmakers on Wednesday began considering restrictions on unorthodox mortgage-lending practices that have allowed hundreds of thousands of Californians to buy homes they otherwise could not afford.

About half of all new home loans in California are something other than the traditional 30-year fixed loan. They use features such as no money down and variable interest rates, while giving borrowers creative monthly payment options such as paying only the interest or even less than that.

Such low introductory payments or teaser rates are offered in exchange for higher bills that will kick in years later, sometimes tripling or quadrupling monthly payments. Regulators said many of those riskier loans were taken out in 2004 and 2005 and will start resetting to higher rates this year.

"The exposure to these sorts of products, the growth, is unprecedented," Raphael Bostic, an associate professor at the University of Southern California School of Policy, Planning and Development, told a Senate committee. "The regulatory oversight of these types of practices is relatively lax."

About 12.5 percent of riskier mortgages nationwide were delinquent by last fall. Nearly 1 million homeowners nationwide either lost their homes or missed monthly payments from July to September, according to the Mortgage Bankers Association.

"The market did not save them," testified Pam Canada, executive director of Neighborhood Works Home Ownership Center in Sacramento. "This was a nightmare with no happy ending."

The trend will worsen, the Center for Responsible Lending predicted in a December report.

The center estimated that nearly 20 percent of those who took out risky mortgages will lose their homes nationwide. In California, more than 21 percent are likely to default, with a foreclosure rate as high as 25 percent in some areas.

"The problem is that many consumers have not prepared an exit strategy," said Ed Smith Jr., chief executive officer of Plaza Financial Group Inc. of San Diego. "The key is customer education."

February 03, 2007

You know how trends start in California then spread from there? Here's one - everyone loses their home!

![]()

![]()

Subscribe to:

Post Comments (Atom)

15 comments:

.

.

.

No Exit Strategy!

Now let's see...Where have I heard that phrase before?

Can I phone a friend?

Hello,

George can you help me out?

RayNLA

http://www.dailybulletin.com/search/ci_5139390

Lawmakers eye mortgage woes

Committee looks at issues related to housing loans

They may be locking the barn door after the horse has been stolen, but California lawmakers want everyone to know they're very unhappy about these risky mortgages that are starting to go bad.

Home sales are tanking, foreclosures are climbing and housing prices are basically heading sideways.

So Wednesday in Sacramento, the Senate Banking, Finance and Insurance Committee held hearings on less-than-traditional mortgages, including adjustable rates, interest only and sub-prime lending.

Witnesses at the hearing spoke of negative-amortization loans, in which the amount owed actually increases instead of decreases as time passes.

They spoke of lengthier mortgages, some for as much as 50 years, compared with the traditional 15 or 30 years.

They told how in some cases, borrowers were not required to prove they had any income or assets or even a job.

It has become clear that many of those marginal buyers were banking strongly on a continued runup in the housing market, a runup that saw home values more than double in the Inland Empire between 2001 and 2005.

"A lot of people got talked into loans they should not have taken," said regional economist John Husing. "Adjustable rates, big balloon payments, large jumps in interest rates. Housing was sold to them as an investment, and now some of them are losing their houses."

Husing pointed out that whenever there is a period of "speculative craziness," people look at all the money being made and want to get in on it.

"A lot of people got into loans and didn't have a clue what they were really signing," he said

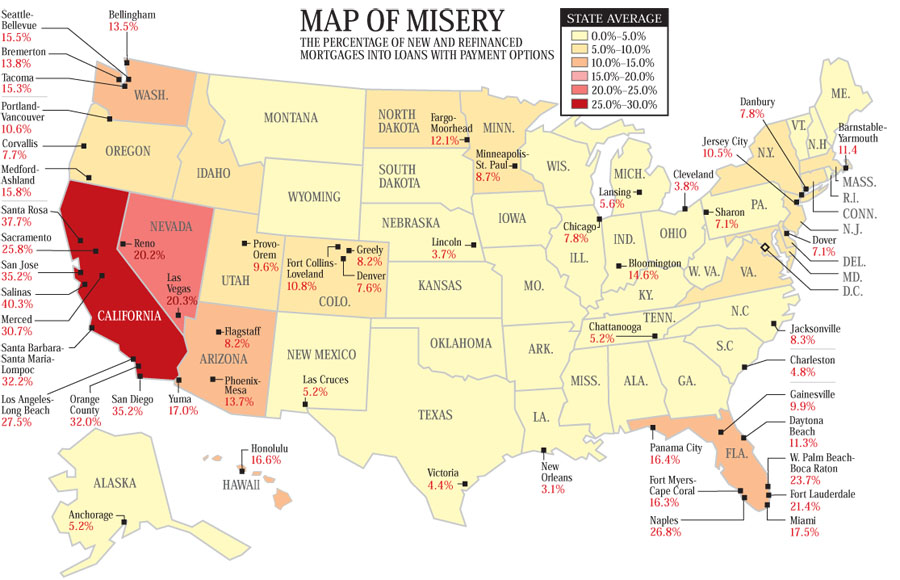

There's no date on that map. How do you know it's for 2006?

Nearly 1 million homeowners nationwide either lost their homes or missed monthly payments from July to September, according to the Mortgage Bankers Association.

OK that souds pretty bad. But what was the comparative number July to Sept 2005, 2004, 2003? Just throwing a number out there without any context is meaningless.

And even if last year this number was 100,000, I still don't want the government getting involved. This is a free country and that freedom includes the freedom to be an idiot financially. What's next banning credit cards because some people get in over their heads? Banning car loans because some people buy too much car? Where does it end?

And lumping in "missed payments" with "lost their home" is ridiculous. Missing 1 payment and losing your home are worlds apart in terms of severity. It would be like saying 1 million people visited the doctor for either a heart attack or a cold, not exactly the same thing.

The map is at least 6 months old- that's when I first saw it.

That being said, those vacant homes will be filled with thousands of Chinese immigrants. Remember China has $1 trillion U.S. dollars in reserve thanks to the trade imbalance and a population of 1.3 billion.

I saw a date on that map before, I think it was for 2004 or 2005. I'd love to see an updated one for 2006.

Lenders are increasing credit requirement for borrowers, especially for Option ARMs. IndyMac Bank now requires a 640 score for subprime. Lenders don't need Government to tell them what to do. They have to restrict or perish.

"The key is customer education."

------------------

The government doesn't need to do a darn thing. The market will take care of the "educating" all by itself.

But then, the govt. has to appear like it is doing something, hence all the headline drama.

"bake mcbride:

Not only am I amazed that "option-ARM" loans are legal, not only am I amazed that in some towns in California 40% of new loans were written this way last year, but I'm also blown away that Congress hasn't stepped in to try to stop this disaster in the making.

********************************************

I'm not a fan of these loans, but in the right circumstances they make sense for some. Congress should not be involved...it's a free market and smart people will step up where stupid people F'd up."

The problem is the country is caught between talk of free markets on the one hand and the residue of the welfare state of the past on the other. Our educational system is still a relic of the past. Few Americans have any financial or economic education at all. Economic literacy is actually undesireable if the state runs the show.

Because of the past, many people are still conditioned to think our government is operating for the benefit of the greatest number. Since this is untrue, people's naivete sets them up as marks.

The supposed transition into free markets and globalization is equally confusing and equally misleading as all data proves blatant interference by everything from Fed interest rate and money supply manipulation to tax policy to currency battles to the push for empire. This is anything but a "free market".

The game is rigged and the house wins. Hindsight is the only thing that will show whether we were fortunate with our bets.

"those vacant homes will be filled with thousands of Chinese immigrants. Remember China has $1 trillion U.S. dollars in reserve thanks to the trade imbalance and a population of 1.3 billion."

I came across an article that theorized the Chinese have already used their $1 trillion US dollars in contracts sewing up future commodity supply - for YEARS. Not to mention the various mines and energy companies they've already purchased outright. That seems a lot more likely than thinking they'll buy up housing in this country that is already starting to fall apart at the seams due to poor construction.

Bake McBride and one anon poster believe the free market rules, and the rest of us shouldn't care about option ARM misdeeds and "financial idiots." Sorry, guys, but I disagree. The gov't is everywhere you look in this game. Could the banking system as we know it exist without federal deposit insurance? Would there be all this available mortgage money without Fannie and Freddie? (I know, they're not really government agencies. They're just creatures of Congress, owned by their shareholders. Just a quirk of history that they are exempt from local income taxes. Just another quirk that they haven't been delisted, even though their books are in such disarray that they can't comply with SEC reporting requirements.)

As others have pointed out, the American taxpayer is on the hook big-time for this mess. And yes, the credit card industry and other loan sharks should be regulated more. We need to return to the concept of usury.

What's the over-under 93.5% of the pay-option mortgages go into default?

Hopefully the ethnic violence currently going on in LA will spread as well.

People in WA. State have their heads so deep in the sand it's unbelievable.

Just LOOK at the color of WA. on that map!

I haven't seen anyone do an analysis of the "Center for Responsible Lending" report. It is WAY too conservative.

They look at subprime loans issued from 1998 to 2004 or so, notice that about 20% of these loans either ended in foreclosure or in what they call distressed prepayment - refinancing or selling after at least one payment was late.

They note that if the market is tanking fewer people will be able to sell or refi, they pretend to adjust for greater risk of "adjustible rate" loans (and other risks) - and come out with that 20% foreclosure risk.

It doesn't really take into account HOW much more toxic an option arm mortgage is than the regular old ARM's of the past - nor does it consider the additional effect of no-down-payment mortgages.

My model: there are 5 risk classes:

1) IO or negative amortization

2) adjustible rate

3) no down payment

4) no or low doc

5) subprime borrower

If three of these apply, there will be at least a 90% chance of default in a declining or steady price environment.

Any two still gives about a 65% risk of foreclosure.

I would guess the odds are still about 20% for any ONE risk factor above.

I used to call risks 1 through 4 the four horsemen of the housing apocalypse, but with the fifth factor, I'll have to think of another catch phrase.

Post a Comment