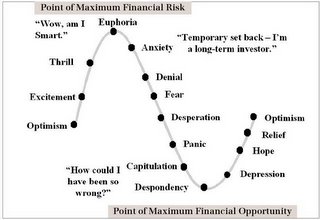

Even the realtors aren't in denial anymore about the bubble bursting. Even if they want us to believe we've already briskly sailed past desperation, panic, capitulation, despondency and depression, that the worst is over, and that we'd be heading back up the curve now. Yeah, right.

Memo to realtors and the masses: It's never different this time.

After this epic and historic ponzi scheme, we must go through each stage. It hath been foretold.

I think looking back on the late great housing bubble in our own minds we can now think back to what each stage before fear felt like. Yes, HP'ers are ahead of the plodding masses. When everyone else was in Euphoria, many of us were in Fear, and got out.

So who's with me? Is America done with the silly Denial days? Is fear here?

It sure smells like it.

October 26, 2006

With 100% confidence I say we've officially moved past Denial and firmly into Fear now

![]()

![]()

Subscribe to:

Post Comments (Atom)

105 comments:

Fear, but they will deny it at the NAR.

Homeflipper said...

Look, the worst is probably over. The Fed have stabilised rates therefore affordability won't get any worse. What is more, by the middle of next year, rates will start to come down. Moreover, home sales have started to recover.

Besides only a tiny minority of people are actually taking a serious financial hit. Most who bought in 2005 are sticking with their new homes and waiting it out.

Five years from now, the market will be appreciating at a steady 5 percent a year. And everyone will have forgotten about this months price data.

salt lake city still selling, austin, bainbridge island wa(seattle). No gloom and doom. Closing today on a condo in salt lake. Purchased last year for 112,000 1 year option arm i/o 5% and rented easily for the last year at 950 per month. Sold today 170,000 in 2 weeks. Could have held and sold for 180,000 to 200,000 but time to move on. 1031 exchange into a fixer sfh in salt lake city. no gloom and doom.

The whole country is no doubt now on the downward slope, spread across the Anxiety, Denial and Fear phases. The Seattle region is just now heading into the denial period.

Still heavily in denial here in Northern VA. Don't talk about it, just a minor blip.... Things will pick up in the spring.

This will be a long winter for the REIC.

salt lake city, austin and bambridge island represent 1% or less of the US population

the other 99% - screwed

Some of the new homes that were built last year at this time and never sold have for rent signs in front of them. The wife and I have been looking at renting one of these for $1500 month. I get to rent a brand new 4bd 3ba house for $1500 month $1000 deposit. I smell fear. My life is great!

WE are totally still in the denial phase. The public has no idea what is coming. It is hard for people paying attention (such as people on housingpanic) to believe that Joe Public doesn't know-but he does not know.

the masses have hardly even reached anxiety at this point.

the majority isn't even aware of the possibility that prices won't be going up next year.

we have YEARS to go on this cycle.

the catalysts will be arm resets, stricter credit standards, and slowdown in consumer spending. it probably will never go off a precipice. it will likely be a slow grind down over the next 5+ years.

unless an exogenous event occurs (like a dollar panic).

More wild hysteria from Keith. Yes, some builders and flippers are gonna get screwed, but by and large there will be no HP that will cause an economic meltdown.

The Fed has the liquidity floodgates wide open and that will permit borrowers to refi out of those idiotic option-ARMs. The BoJ and China's honchos have agreed to keep buying our Treasury debt so interest rates over here can stay reasonable.

Ask yourself this simple question - back in 1995 would you have believed in your wildest dreams that mortgage rates would be under 6% in 2006? Unless rates jump much higher (9%-12%), there isn't going to be any HP.

the last poster thinks we're going to go from right to left on the curve

he he he

I agree with general consensus here that most people have no idea what is coming.

I am of the opinion that this is happening way faster than most thought it would. The ARM resets account for around 20% of the outstanding mortgage debt. How many will be able to refi or sell. The new BK law that the republicants passed will haunt them in 2008 because of all the FBs finding out that they have been screwed.

over 2006 to 2007 it is by most estimates 1.9 to 2.1 trillion of the 10 trillion loaned out. This does not include IOs or POs.

Judging partly by the posts by Homeflipper and Anonymous, I think there are a good many of us still in Denial. But I would say there's a distribution and there are still a lot of people still in the Anxiety, temporary set-back stage.

Fear is too close to the bottom and I don't think we're near the bottom yet. When I see a 10% drop in existing home prices (which is likely to follow new home prices) then I think we will get real Fear. Also, the relatively short time-frame in which this decline has occurred will allow many to tell themselves the setback is temporary.

I think we're looking at another 6 months to a year before we get real Fear. I see a bunch of things happening in Spring and it taking a while for these facts to sink in on FBs. These Spring elements will be: 1) continued increase in foreclosures; 2) increase in inventories from sellers who are currently 'waiting it out'; 3) increased mortgage rates that more correctly reflect risk; 4) a smaller but continued price decline.

In the Summer is when Fear will begin as even the most willfully blind FBs begin to lose faith. I think FBs should be afraid but remember, the reason they are FBs is because it takes them awhile to process these things.

Just my opinion.

I see a bad spring coming for the NAR. As Paule.Math said it will gradually accumulate till it is an elephant in the room.

At the back of the roller coaster are the "Wow am I smart" gang. At the front are the "denial and fear" bunch. Right now the "Wow am I smart" bunch are asking: "What's all that screaming ahead of us all about?".

Oh one more thing, what the people running the ride don't even know is that the coaster is coming off the tracks at the bottom and will decapitate everyone on board.

Pulte remprted miserable earnings and the stock is up today (10/26/06.)

We are still in denial, maybe anxiety.

"That's the second time in two days that somebody has tried to pass that off as "good" news. Excess liquidity = inflation = higher interest rates because borrowers want increased returns on a shrinking dollar. Every time the fed prints money then the money you already have is worth less. Anyway, if the floodgates actually were wide open then we would be in a death spiral of hyperinflation."

If we lived in a closed economy, you might be correct. But in this global economy, other central banks can act to support our monetary policy and keep U.S. interest rates low. That is exactly what the banks in China, Japan, and Korea are doing. Why? To keep their exports flowing -- one hand washes the other. Yes, price inflation will be the ultimate result. But in a perverse way, it will actually help to solve the debt crises facing many public and private borrowers.

As to your doubts about what is happening with the money supply, take a look at:

http://www.nowandfutures.com/key_stats.html

It clearly shows that M3 is on a tear, currently expanding at a 10% annual rate. That's the equivalent of $1.2 trillion every month added to lending reserves. Those option-ARM resets everbody here is worried about will be taken off the books and replaced by longer-term fixed loans. Count on it.

So please look at the facts instead of parroting Keith's doom & gloom scenarios.

People are beginning to see and hear the negative news about the bust and accept it, but they continue to think that their area will not be affected. The whole "it won't happen to me" concept. It amazing the rants that people will go into regarding how wonderful their town, or part of town, or home is and how it won't be affected. Even in the ones that are falling the worst like Vegas and the like.

My bad, correction:

That's the equivalent of $120 billion every month added to lending reserves.

It annualizes to $1.4 trillion

I thought we would be entrenched in the DENIAL stage until The Fed has it's next rate increase which will scare the crap out of the REIC who has been telling everyone prices will go up as soon as The Fed lowers rates. But, I think today's numbers threw us over the edge into the FEAR stage of the crash. There is no denying what today's numbers show and I think tomorrow's news is going to show the S hitting the fan.

At current rates you are correct. However many reputable economists think the FED will be cutting rates in 2007. The FED knows that ARM's are resetting too...

I read an article on yahoo finance today that said that there isn't a single Fed member that is even considering cutting rates anytime in the near future (2007 is considered the near future) and that the consensus is to raise rates after the election.

"True, but mortgage interest rates depend on the interest rate you have to give investors who buy mortgage backed securities. If some of these bond issues default because of a rash of forclosures then the interest rate will go through the roof. The fed rate is not directly connected to mortgage interest rates."

So where are these higher rates? Our combined government and current account deficits are over $1 trillion a year. Five years ago Warren Buffett warned about the demise of the dollar and higher rates. Neither prediction happened. Why? Because the central banks in exporting countries would rather maintain their business with the U.S. than see an economic emergency.

They are buying those bonds knowing full well that they will get screwed in the long term when the U.S. pays them back with devalued dollars. It's all part of the BIGGER DEAL.

Metroplexual has found the best housing head pic yet. 5 points.

"You see the fed's creating trillions of dollars out of thin air as a positive thing, I see it as a bad thing. These are opinions, not facts."

You are absolutely right, and the Austrian economists are all spinning in their graves over this reckless monetary policy. But what is the alternative? Nobody in their right mind (and especially politicians) wants to see a worldwide depression that would erase the debts and cleanse the system.

Instead, the central banks are colluding to keep things bobbing along. I don't like it either, but at the same time, I just don't see any valid reasons why they can't maintain this charade through my lifetime (20+ years).

kkdoughnut...Everyone will change from reset arms to fixed??? The reason people have those arms is because they could no way afford a fixed term with required principal payments and equity down. Many will find they are ineligable because the original loan is more than the asset value of the house. Guess what? No refi then. They're stuck with what they got.

I got out a couple years back. Guess I missed the peak but my invested profit is paying 100% of my rent.

I'm waiting for the credit event to occur. Seems like its fast approaching.

2007 will mark the beginning of the Greatest Depression. People will once again blame the market when it crashes, but we know the real cuplprit. Don't we Mr. Greenspan?

Housing is always going up. So if you don't get in now you will be permanently screwed. You better buy now or you will be priced out of the market.

You really think things are going to drop? Most everyone is going to hold onto their house and onto their asking prices.

If you don't buy now then next year when things rise again 20% or 30% you will be feeling really stupid.

Plus rents are rising now so if you don't buy then you will be totally screwed because you will be paying all that money into thin air.

Better buy now. Right now. Go to the nearest house and make an offer before it's too late.

The bottom line is you just don't know the American public. House prices dropping isn't at all on their radar now.

Everybody I talk to is either a) Looking to buy a house or b) has a ton of equity in their house.

Nobody is worried about house prices crashing. Therefore, they won't crash, it's that simple.

Better buy now ... or you'll be priced out forever.

In fact, Seattle is still rising. Somebody I know in Bothell near Seattle bought a house earlier this year and already flipped it for $100k profit.

I've been vehemently assured by 3 REALTORS and several investors & homeowners in the last 18 hours that prices in Phoenix have leveled off and are going up at 5 - 8 % per year... or more...

and, I've been flogged with the concept that: "It's a great market and there has NEVER been a better time to buy than RIGHT NOW in Phoenix!!"

Maybe I'd better run to the next available house and offer the asking price! Gotta go before someone beats me to it!!!

"Also, consider the elasticity of the demand curve. New home sales jumped 5.3% on the discounting. If the homebuilders are able to clear the inventory, layoff employees, and reduce the number of new homes being built then the supply on the market will fall dramatically."

"Average Joe would rather take his home off the market than discount his price. We come back to the same issue, what will be the catalyst for a real panic??? No one here seems to address that question. If unemployment doesn't rise then why would people stop making mortgage payments?"

What about all those laid off REIC workers? That would increase unemployment. What about the offshoring of many of the better jobs?

"Will the resetting of ARM's really do that much damage?"

Yes, it will. The people buying with suicide financing in the bubble epicenters could barely afford the teaser rates. Now the rates will go up and maybe they'll have to start paying back some principal as well. The result is lots of motivated sellers in the most overpriced markets.

"The last time the housing market turned down unemployment was rising rapidly and the economy was in recession."

OK, this time unemployment is rising rapidly (but of course the new and improved statistics don't reflect that) and the economy is in recession. If you use the real inflation rate, GDP is falling.

GrandInquisitor said...

The only way credit will dry up is if the yield curve inverts and there is no incentive to lend long term.

------------------

It's already mildly inverted, isn't it?

Thanks anon, I am just trying some on.

Metroplexual said...

...

The new BK law that the republicants passed will haunt them in 2008 because of all the FBs finding out that they have been screwed.

------------------

Hopefully the opposition party (do we have one in the US?) will have the guts and brains to keep hammering on this point in 2008.

It's the ownership society, stupid.

GrandInquisitor said...

"Millions of people will see their mortgage payments double in the next 12 months."

At current rates you are correct. However many reputable economists think the FED will be cutting rates in 2007. The FED knows that ARM's are resetting too...

--------------------

The Fed probably WILL cut in 2007, so the payments won't quite double, but it will be bad enough, especially considering that we'll be deeper into recession by then.

Many, many, many FBs will find out that when you "stretch" to buy a home, you are liable to end up tearing something. OUCH!

With all of this talk of the “FED”, I thought that some of you may find this interesting.

AMERICA: FREEDOM TO FASCISM

"FOUR STARS (Highest Rating). The scariest damn film you'll see this year. It will leave you staggering out of the theatre, slack-jawed and trembling.”

Watch the entire film Here!!

bubble trouble said...

People are beginning to see and hear the negative news about the bust and accept it, but they continue to think that their area will not be affected. The whole "it won't happen to me" concept. It amazing the rants that people will go into regarding how wonderful their town, or part of town, or home is and how it won't be affected. Even in the ones that are falling the worst like Vegas and the like.

------------------

Oh yeah, the good old "everyone wants to live here" (whereever that is) thing. Denial with a capital D.

Oh, yeah - I know a guy who made, like $275,000 on one flip and then $150,000 on another flip the same day and then he bought himself a double latte with whipped cream on top!

Gedouttahere.

I am sitting on the sidelines in MI. Just signed a new 6 month lease out of fear. In fear that the crash will not be meaningful around here while the rates go up to combat inflation. A rate increase will F me more than a partial, permanent, correction will help. The simultaneous fear is that rates are cut and that buyers think they get to hold on longer because "rates are down". I would like to see a sharp meaningful crash that quickly stabilizes so things can move on.

The FED sticks it hard Part I- Cheap

Money

Part II- New BK Rules

Part III- ALAN Recomends ARMS

Part IV- Alan bows out and leaves Ben holding a flaming bag of sh%%.

Part IV- Alan bows out and leaves Ben holding a flaming bag of sh%%.

Part V- Ben, doing what he must to prevent Revelation, blows into the Bag-o-Shiat and inflates us all home; rewarding the debtors and punishing the savers... Only to be visited at some later date by hyperinflation during the Tribulation.

Veep at my co., very intelligent man: "I understand it's only the flippers who are really going to get burned..."

Maybe a lot of people are out of denial, but thanks to listening only to NAR press releases & MSM, are just not fully informed as to the possible extent of the problem.

Metroplexual, you need to go with the tin foil hat pic. When I saw it I died laughing. I agree with anon, it's the best one I have seen from anyone.

These links are for those of you that are unaware of the fact that foreign banks are moving out of the US $. Also, the two of you posting about how China and Japan will continue to purchase and hold the dollar are ill informed. In fact they are both looking to diversify out of the dollar and into other currencies. Do some research.

What does the fed do when they are seeking to keep foreign interest in the purchasing and holding of dollars? They raise interest rates. You're not keeping up on your reading and your not listening to Bernanke when he says he has no plans to cut rates in the near future.

Costello seeks orderly withdrawl from US $

http://www.smh.com.au/news/business/costello-seeks-orderly-us-withdrawal/2006/10/17/1160850931319.html

Greenspan says dollar now sharing stage with Euro...

http://today.reuters.com/news/articlenews.aspx?type=businessNews&storyid=2006-10-26T142042Z_01_WBT006123_RTRUKOC_0_US-ECONOMY-GREENSPAN-DOLLAR.xml&src=rss&rpc=23

Sorry, I don't know how to do the tiny url thing.

Bottom line: as much as you may wish for the alternative...interest rates will hold steady as long as the feds are able to do this without seeing an exodus from the dollar. The fact that the threat is there alone, will move them in the direction of raising interest rates.

Part VI-

HPer's get free BJ"S because we are so smart. Anybody else agree?

Here are the two URLs that I have changed via tinyurl.

http://tinyurl.com/yzcero

http://tinyurl.com/y4bpxn

To make an address shorter, simply copy the long address, go to www.tinyurl.com, and insert it in the blank slot as shown. Then click the button and a "tiny" address will appear. Finally, copy the tiny address and paste it into a message on this blog.

Based on some of the comments in this blog, I would say we're still in denial. This is the biggest price drop in 35 years for both new and existing homes. That's half a lifetime.

Other than the chimera of lower long-term interest rates, there's nothing on the horizon to slow the fall now that it's begun.

Okguy s we won-how about we get some free BJ"S

I have said it before and I will say it again. Interest rates will be the final blow to this market and will be blamed for the downfall, although housing really just became unaffordable for the masses and that's why the game stopped.

The world works on a global scale and the part that most Americans don't get is that the dollar has traditionally manipulated all markets due to it's stance as a world reserve currency.

Other countries are catching on...the Euro popped up, and these countries are realizing the Euro is more stable than the dollar and seek to invest in it and trade with it rather than the dollar. The issue alone will cause and has caused some serious panicking by the US.

What many of you are missing is the fact that times are changing and we no longer have the dominance over currency and wealth...it's slowly slipping.

Interest rates are not going to be cut for this reason. Do not count on it, because trust me...the fed and the gov care much more about their precious ponzi scheme than you losing your house or really when it comes down to it...the masses losing wealth. Not when you compare it to this larger threat.

No way! We are nowhere near the Fear stage hear in MA (North Shore). Prices have barely budged! Maybe down 5%. Here we are still very solidly in the Denial stage. Sure would like to see some panic, but it's not happening! Houses and condos are still moving, albeit somewhat slower than last year.

i wouldn't have thought we could make it 20+ years in 1990 and here we are.

but there is a limit to what can be done. can they pull another rabbit out of a hat? perhaps.

consumer debt levels are at an extreme. housing prices are at an extreme. debt must be serviced at some point. japan dropped rates to 0% which created a carry trade which blew the bubble bigger. if we drop rates to 0 and negative, who is going to soak that up?

i doubt we have 10 years.

Interest rates are not going to be cut for this reason. Do not count on it, because trust me...the fed and the gov care much more about their precious ponzi scheme than you losing your house or really when it comes down to it...the masses losing wealth. Not when you compare it to this larger threat.

-------

bubble trouble

I agree and no one will listen to me. it is the deer in the headlight stare. or the gov won't let that happen to americans. or the fed bank wants to protect housing and the prez will tell them not to raise interest. these are actual conversations with some people at work! they have helocs and are in bonds.

geez.

NFW are we at Fear. Still way above it. And even if there's a drop in units for sale - -I'll call it that sellers are taking units off the market -- a form of denial.

Phones aren't ringing at all at the shithole realtor office in my bldg. But they're still scheming and beaming -trying to put a good face on it. Still a few marks coming in they fawn all over.

- Mr. PoPlicki

Or you could do this and this.

Although tiny can be quite handy at times as well.

Points control my life

Because I caved to my wife

She went down, so I bought into this town.

Points control my life

My mind keeps returning to Paul Volker and the recession in the early 1980s. I'm curious to know if how the government calculates inflation in 2006 [4.0] differs significantly from how it was calculated in 1980 [13.50].

We may have to take our medicine.

The day I signed,

I crossed the line.

First through the door,

Now I will be poor.

The agent was my best bud,

now he pounds his pud.

I look around,

to hear the sound,

of my last purchase,

a single live round.

My mind keeps returning to Paul Volker and the recession in the early 1980s. I'm curious to know if how the government calculates inflation in 2006 [4.0] differs significantly from how it was calculated in 1980 [13.50].

We may have to take our medicine.

--------------------

Oh, it certainly is very very different. Hedonic adjustments and other trickery are used to produce the lowest numbers possible.

Didn't Volcker say (fairly recently) that, long-term, the only direction for the dollar is down?

Listen!

Just drink the *$&%*(# Kool-Aid and buy a house!

Thank you,

A. REALTOR

Gold,

My friend. Shiny heavy metal.

You will save my arse when the shiat flies.

You will keep me safe.

When the presses run wild.

When the grown men cry.

I long for your return from behind the curtain.

When green is used for wiping my bung, you will get it done.

Deliver us.

We're in fear and that stage could last a year or more

BTW, I too suffer from a fear of heights.

I'm definitely afraid.

Afraid of HP flying monkeys flinging a bunch of crap about impending doom.

FlyingMonkeyWarrior said...

Interest rates are not going to be cut for this reason. Do not count on it, because trust me...the fed and the gov care much more about their precious ponzi scheme than you losing your house or really when it comes down to it...the masses losing wealth. Not when you compare it to this larger threat.

-------

bubble trouble

I agree and no one will listen to me. it is the deer in the headlight stare. or the gov won't let that happen to americans. or the fed bank wants to protect housing and the prez will tell them not to raise interest. these are actual conversations with some people at work! they have helocs and are in bonds.

geez.

-------------------------

Will Helicopter Ben allow a full-on deflationary housing depression just to prop up the dollar? I really don't think so. There will be sufficient injections of liquidity (interest rate cuts, debt monetization) to keep *nominal* home prices from falling too far or too fast. Of course real values will be dropping like a rock for years and years. Keep in mind that the government owes a huge amount of dollars and thus prefers to have inflation, especially if the amount of inflation can be convincingly underreported. Uncle Scam is the biggest debtor in the world.

I predict that we are in for a long stagflationary recession as the Fed tries to steer some sort of a middle course (loose but not too loose) in terms of monetary policy. Note that this is definitely NOT the same as the Fed dropping $1000 bills out of helicopters to bail out in-duh-vidual homedebtors.

By this time next year, the benchmark rate will almost certainly be lower than 5.25%. The housing situation and general economy will have gotten so bad that Helicopter Ben will have little choice but to cut rates.

The dollar will drop in value vs. other fiats, but the dollar is toast anyway. It could easily drop another 40%.

There is no way I'd have a large percentage of my savings/ investments in long dated dollar denominated bonds. A 5% yield vs. likely inflation of 10-15%? No thanks.

keith, you gotta get one of these.

This is what stagflation might look like:

- Actual inflation: 12%

- Reported inflation: 6%

- Joe Sixpack's raise: 5%

- Actual unemployment rate: 15%

- Reported unemployment rate: 7%

- Actual GDP growth: -4%

- Reported GDP growth: 2%

- Nominal home price change: 0%

- Real home price change (reported inflation): -6%

- Real home price change (actual inflation): -12%

From the posts it looks like no bubble exists. After all consumer sentiment drives perceived value. Joe Six-pack, feel free to buy your dream home.

"fear"???? what are you smoking keith? I see no fear in the air hear in SF Bay Area

prices are steady and sales picking up. 1 bedroom 700k condos in SF with NO parking are selling in 3 weeks

AT LEAST THIS IS NOT A PROBLEM...

Central banks in China, Japan, Taiwan, South Korea and Hong Kong have channelled immense foreign reserves into American government bonds, helping to prop up the US dollar and hold down American interest rates.

Mr Costello said "the strategy had changed" and Chinese central bankers were now looking for alternative investments

Hahaha. No, we aren't even close to fear yet. We are still in the top of the first inning of the crash.

Salt Lake City Cheerleaders, Things just take a while to settle in, and yes you can sell at a profit as long as someone else has confidence in the future of the market. Long term SLC will go the way of the rest of the country.

I have been watching the inventory in Utah and it has been steadily rising for several months at about 150 dwellings per week.

Even if people are offered a low interest fix rate refi. How are they going to feel paying $4000/mo when the same house down the street is going for half that?

That would be real depressing in my opinion. Imprisoned in your house.

You just don't get it...there is more at stake if the fed does not raise interest rates. Do they want more countries looking to trade oil in dollars? NO. Do they want China, Japan, and the like to transition more and more into other currencies? NO.

They will not cut rates to save your pansy ass.

The housing bust will happen so painfully slow that there will be no drama...I agree with the others that are talking about a slow decline over the next few years, maybe some sort of Japan like senario. There will be no sort of OMG the sky is falling and the feds must rescue us as a people. There will be a recession. Let me say that again...there will be a recession, but we have had recessions before. Why do people think that cannot happen...because the fed and the gov will take care of it. Give me a freaking break.

There will be sectors that have downturns and we are already seeing that, the fed does not care about the minority. Bush even said, when a women once asked him how her son was going to buy a house, being that everything is so unaffordable..."markets take care of themselves". He did'nt say don't worry honey, we will take care of you and your family. Now that the tables have turned and the downturn in housing has started because "the markets take care of themselves" there is certainly a whole lot of irrational bargaining going on in people's heads...when people actively wish for things to happen based on nothing of merit. Also, a lot of really huge egos, if you're really thinking...well if I can't afford my house because my ARM resets, than the fed will just drop rates.

Bubbles are followed by busts, by a retraction, a correction, however you want to say it.

It really is a no-brainer, if you have an ARM, refi...if you can't refi because you won't be able to afford it, sell your freaking house. Or start thinking about that second job or finding some nice people to be your roomates. If you think that the fed or the gov will take care of you, you are a fool. Please don't be one of the foolish.

We "bubbleheads" don't want to see individual people suffer, but we do want to see people wake up before they get worked. Well at least that is how I feel about it. The MSM, the REIC, the seller, even your neighbors will say anything (spin, cheerlead, etc.) to make a buck and/or save their asses.

http://www.zillow.com/HomeDetails.htm?city=Glendale&o=North&state=CA&zprop=20836012921

Family sold this property, estate sale for 740k last year. Just sold for 999k a year later.

A year later? This is flipper activity. As long as a bigger flipper fool comes along fine.

The house is a 1927 wreck.

Whoever bought it, just signed their own financial death warrant.

Keith, you have to check this guy out. Big real estate pumper con artist. Can't believe this guy is for real pumping real estate in Phoenix as we speak.

http://www.geraldromine.com/

"so, will the fed prop up housing over the dollar?"

yes. yes they would. they HAVE been.

Bernanke is buying the long bond.

Real long rates are NEGATIVE

think people

You folks on this website, Keith especially don't really get what is happening.

The issue is NOT that housing is overvalued, in a bubble.

the REAL issue is that the dollar is worth LESS relative to housing and every other basic living expense -energy, food, tuition, medical etc etc etc etc etc.

Housing is NOT in a bubble. Housing is NOT overvalued.

the REAL issue that is going on is that the dollar is being DEVALUED and the middle class is DISAPPEARING.

people can't afford a house because THEY ARE NO LONGER MIDDLE CLASS!

it is the dollar stupid!

Bubbleshaker said, "since this is the biggest bubble in all of history, I would look at Japan as the model, 15 years of depreciation in housing and getting weaker, nice try though."

You sound like Sadaam with the "mother of all wars". The war in Iraq doesn't come close to WWI, WWII, Korea or Vietnam let alone the wars waged in Europe in the 1600-1800s. As for the the current bubble being the biggest bubble in all of history, do your homework. The USA is ranked way down the list of Industrial and even Second world economies for price and cost ratios.

Japan? Get a clue. The value in Yen and in US dollars in 1990 was outrageous by any standard (but maybe not as ludicrous as th Tulip mania bubble). Take thos 1990 prices in dollars and calculate what that would be in 2006 and our prices look paltry in comparison. If you think 2006 prices in Tokyo at up to 60% off their 1990 highs are some how now so much more affordable you don't have a clue. $800,000 and up is the norm for an efficiency flat, though you can find some bargains in less desired areas or buildings for a mere $600,000. Imagine what that price was before the decline in 1990 dollars adjusted for inflation? Something like $3million for 500 sq ft? And that wasn't a luxery suite or location.

And have you been outside the USA? Do you really know what it costs to live in parts of Europe? Have you seen what you get in Madrid, Barcelona, Paris, London, Rome, Milan, Venice? Have you been in the small villages of Andalucia or coastal Spain or Tuscany etc? In small villages an hour from the coast of Spain in Andalusia a small village house runs you $250-500,000 Euros (so at 30% in dollars) and this is in areas that are predominately agricultural/tourist economies. You get away from the major population centers in most of the USA and you can find plenty of houses, larger and more modern, for under $100,000 and I can tell you that in most of western Europe you can't find much of anything for 70,000 Euros that is habitable.

So many HPers are so pathetic and desperate. Everyone needs to keep a perspective that there are multiple markets in every economy and city in the USA. I don't care if you bought and tried to sell in LA during their hot market if you overpaid for a house to start with and then dumped a couple hundred thousand into fixing it up and then thought you deserved to get every penny back and make $150,000 or more in profit when you tried to sell is pure insanity.

You have to start with a sound investment from the start and as one person said here about feedback on Austin, SLC, etc that they represent only 1% of the total market, well remember that out of all the millions of homes sold in the past six years a small portion were bought at the peak and if you take all homeowners the same applies to those who took out all their equity.

Correction in the market place? Yes. Some people going to get hurt from their decisions driven by greed and not sound economic principles? Yes. Maybe a recession? Yes. Maybe some markets seeing a significant drop in price? Yes, but remember only tose who buy at the top are hurt the most. So get a grip and stop being like fundamentalists that see the end of the world in every small earthquake or natural disaster.

Yes...the fed did prop up the housing market. The fact that they kept the rates so low is one of the major reasons why the housing boom happened. What is happening now is that other countries, banks and individuals have caught on to the fact that the dollar is and has been spiraling downward and America is no longer a safe place to invest, the dollar is not a good hold. So much so that countries begin to take notice. Where do they want to go? To the Euro. What happens if there is an exodus to the Euro and any other country bound to expand? A glut of dollars on the market resulting in hyperinflation and the end to the quality of life for the masses vs. some pain for a smaller group for the relative short term (5 years or so) while keeping the overall game going for a little while longer.

If the fed chooses to allow this mass exodus, than your senario will ring true. The question is...will they? I'm betting against it. If the fed does allow this to happen, it won't matter where housing goes...we will all wake up to the reality of a third world country like scenario.

All I'm saying is the game is different this time around and why would the fed choose a worse case scenario?

Please tell me...anybody...why? Make your case.

foxwoodlief,

I can counter that and say...the US is not comparable to other countries for many reasons. The most important, however is the fact that 70% of our economy is based on consumption. If more and more people spend more and more money on housing, there is less and less for spending on all the shit we don't need but can't live without, which means that Joe Blow down at the PlasticMart loses his job and/or does not get a salary raise, thus furthering the downside of the economy. Soon enough Joe Blow can't pay his mortgage...and forecloses or has to sell to get rid of his debt at a lower price. Nice try with the comparisons...if only our economy were that simple.

It's the debt, not the dollar. Artificially low rates, an unregulated mortgage derivatives industry and ignorance of economic fundamentals is responsible for this bubble.

The days of very low rates and easy credit are near their end. This market is going to fall regardless of the conspiracy theories or the ignorant optimism from those who are sitting on paper profits. All these people have to do is ask themselves if they could afford the high price their house is supposedly worth on paper with little equity down. The answer to that is mostly no. Therefore, prices have to correct to reflect the current economic fundamentals. I am astonished that so many homeowners and bubble apologists don't recognize this.

"Lets see. So when home prices shot up from 450K to 875K in just 3 1/2 years in my neighborhood that was just the dollar devaluing. I wouldn't be calling folks stupid if I were you."

Could you afford your $875K house now with little equity down, current mortgage rates and your current salary? Tell the truth now....

Keith,

Geez, can I at least get a little credit for helping you start this thread? Here's my posting from Thursday about 6-8 hours before you posted this thread.

Anonymous said...

I WANT TO BE THE FIRST TO OFFICALLY ANNOUNCE IT.

TODAY, OCTOBER 25TH, 2006, WE HAVE OFFICALLY MOVED FROM DENIAL TO FEAR ON KEITHS CHART.

THE TRUE HOUSING PANIC IS LESS THAN 6 MONTHS AWAY!

THAT IS ALL.

HAVE A NICE DAY.

OR JUST TRY NOT TO KILL YOURSELF IF YOU'VE BOUGHT A HOUSE IN THE LAST 18 MONTHS. REMEMBER, ITS ONLY YOUR LIFE'S SAVINGS.

Thursday, October 26, 2006 12:26:26 AM

billy bond this prop is for you

after every horrible monthly number release though, we discuss the chart...

this one was the ugliest by far. -10%, historic crash, never in 35 years, etc

denial is no longer possible

I wonder what the next month's YOY numbers will look like? Will they be even worse? Will the stock market take a dump as a result?

As for denial, I think plenty are still in this stage -- because they are not well informed (understatement). Joe Sixpack knows a lot more about his favorite sports teams than what's going on with the economy.

No doubt, some will wonder if now is a good time to buy. What stage is that? Befuddlement?

How can it be fear with interest rates still at 6%? We're still in the anxiety phase and denial is starting to creep in. Denial is seller's not lowering their prices.

Fear is when the seller has drastically reduced the price (-40%) and no buyers are even looking at houses. That's real fear.

think digital cameras and vcr's where this price bubble is headed. it took a long time but i can remember when the first in line for the new thing V.C.R.'s were paying big bucks back 20+ years ago. if you told a kid today that people were paying $1500 or $2000 for a V.C.R. back then, they would not believe you. Remember Sony Beta machines? Big bucks now obsolete as well as a VCR. Digital cameras that were selling a few years ago for several hundreds of dollars are now below $200 and you get a free gas card to boot. Only problem is that the housing bubble has lots more bucks involved, a lot of those bucks are borrowed bucks and the folks who lent those bucks out were under the impression they could not lose because they had real estate collateral - those involved in the more risky end of the business are in for a rude awakening but it is going to be a train wreck in slo-mo. Look at what the companies involved are doing (not saying). They are laying off people because they know that they will not need employees for a long while to come. If this was just a temporary set-back, they would just put together some make work projects, keep those folks around and start doing to Dew in the Spring. The insiders know the jig is up, the news is out, they finally found me, the renegade who had it made ... oh, I digress.

in northern virgina we are still in the denial phase.

i know a few "flippers" and they are deep in denial.

Fear is when you loose your job or your business fails in the midst of a housing crash. Neg equity, neg income, neg savings. Mommy, can I have my old room back?

Take the long view. We still have over 24 months of Bushbuck economics. Real estate just started to come down in the late Reagan years. It didnt crash till Daddy Bush took office and paid the piper for Reagans money printing. Clinton got a blow job which relieved presidental stress, put inflation in check, and made Hillary look pretty damn ugly. Problem solved.

Anxiety is when your neighbor loses his job,

Panic is when you lose yours!

San Diego's North County inland,

Still Plenty of Denial to go around, With Tons of Arrogance as well!

Alot of people would rather DIE than let anyone know about their bad spending habits especially on over priced S**T in a Boom Market! And there will be plenty!

If the fed chooses to allow this mass exodus, than your senario will ring true. The question is...will they? I'm betting against it. If the fed does allow this to happen, it won't matter where housing goes...we will all wake up to the reality of a third world country like scenario.

-----

Are $100.00 rolls of toilet paper in our future?

The Fed will not protect the usa homeowners.

Duh

Although, they wear it proudly as they drive along in their new Hummer or whatever!

Ahem ahem, As I stated in a previous post (one that is no longer here), the housing market in my immediate vicinity is still appreciating at about an 8% clip annually. I believe this is due to white people moving here, in great numbers, from the two major cities in our state. The families that I have personally talked to, said that they were moving away from the cities because of the massive crime epidemic, they went on to further explain that there are a great many whites in these cities getting violently attacked by blacks (rapings, robbings, muggings and shootings). Do we have to ignore this important factor in the value of a certain housing market?

not buying the bubble said...

"Better buy now ... or you'll be priced out forever."

"Priced out forever" is an impossibility. 1st time buyers are the base of the pyramid. How could anyone by a bigger home if they can't sell their current house b/c no one can can afford it since they've all been "priced out forever"? That's what you'd call gridlock. Get it?

----------------

Oh, and ther's still a lot of denial in L.A.

Honica Jewinski - you are right, white flight from urban hellholes is a factor. I live in a small city with low diversity (6%), and RE sales here are booming. Expensive houses (over $500K) are not selling as fast as last year, but the mid-range market is hot and every house under $300K is sold as soon as it's completed.

Keith,

U da man.

some groups of people may be in the 'fear' stage. (over-extended investors, or awake & aware people), but the idiot masses aren't anywhere near there.

at best they might be entering 'anxiety'. I'd define anxiety as understanding that something isn't quite right, but they haven't spent too much time thinking about it yet. 'denial' would be next.

Nah, not past denial. Many friends in trouble. (1) Bought 2BR 2005 $450K coastal CA I/O ARM, persistently ignored my suggestion that the house be auctioned off asap. (2) Bought $400K 2001 nice LA burb, put on market $890K, reduced to $790K, thinking of "adding on to improve the comps", i.e. putting MORE money into an illiquid asset. (3) Bought 2004 on Maine island resort, believes auction sellers are "taking a bath" by not getting what their houses are "really worth". ?!?!?! (4) Bought B before selling A, renting out A to cover about half the cost of owning A, "until the market improves". (5) Built spec house that I am living in; my rent covers 1/3 of the builder's debt service. Why price not reduced?duh

Post a Comment