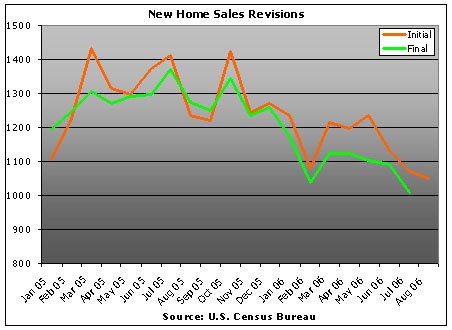

You know that new homes sales report that we mock every month, where they report houses sold and then revise the number downward every month? Here's how it looks charted - thanks to Mish

* Report the number - check

* US media run with it as fact - check

* Fool Americans into thinking it's not as bad as it is - check

* Revise to correct number - check

* MSM doesn't report the correction - check

* American's remain clueless as to what's really going on - check

* Let out a diabolical laugh - ba ha ha ha, bah ha haha - check

September 30, 2006

If you knew your number was wrong and overstated every month, wouldn't you try to fix it?

![]()

![]()

Subscribe to:

Post Comments (Atom)

12 comments:

For an even better chart of what we are facing, please check out the link below (Sorry, I don't know how to properly put this in HTML):

http://www.grandinite.com/2006/09/08/nahb-housing-index-vs-the-sp-500

This chart shows the irrefutable evidence that the S&P follows the Housing Index (with a lag) in lock-step fashion.

And all the "adjustments" and "revisions" in the world won't save the S&P

Interesting link butch, thanks

http://tinyurl.com/gw9sq

here is Butch's link.

Butch,

tinyurl.com

Caroline Baum recently addressed this issue in a well-written Bloomberg article. Watch the cancellations my friends!

http://tinyurl.com/mtqbn

the trend is the same whether you follow the initial number or the revised ones.

Irrefutable?

This is only about 9 years of data!

Statistically its irrelevant. The major indeces are not fueled by all these middle class people who got suckered into dumb loans. They don't participate in the mkts.

Money will migrate out of real estate and back into equities.

RE is dead, bonds are dead, and after 6 years, equities will again take center stage. Big global companies are doing well, have tons of cash for M&A and will move on grinding the little guys into oblivion.

Your analysis is too simple and data mined to fit your conclusion.

All economic statistical numbers are tweaked, manipulated and revised each week or month.

Have you ever paid attention to unemployment numbers? What a joke. If you think housing numbers are manipulated, unemployment numbers are stretched and tweaked every which way for political gain.

Benjamin Disraeli said it best, "There are lies, damn lies and statistics."

Salt Lake Mortgages

That chart on the Grandinite website was in the news a few weeks ago. If you go back to the 1980's there is no correlation whatsover, so it can probably be disregarded.

Keith/Mish: THANK YOU! This is the perfect illustration of what I've been trying to say. It's incredibly hard to find the pre-revised numbers and put together a chart like this after the fact (shock!). Everyone should pay close attention to the "revisions" on almost every stat coming out of the govt/REIC: it's getting farcical, nay illegal.

Mish does some good work -- I had missed this one of his somehow.

The correlation between S&P and house prices can be argued to be stronger now than ever before, and have more relevance year after year, because more and more of America is using house price appreciation to finance non-house purchases. While the short timespan of the chart is perhaps misleading, no one can deny that falling house prices will have an enormous negative wealth effect on the consumer. And the consumer is 70% of the economy.

Anon is wrong. If you agree there will be a housing price stall or decline (even a slight one, but over a long period), then you must properly analyze the effect this will have on American stock prices.

Stocks are not the next bubble. The only thing that could save the USEconomy is another bubble. There is no other bubble left to blow that won't simultaneously kill the USEcon! Commodities? Sure, blow it up, but it will kill via CPI + higher 10y.

The next bubble cannot be stocks for the simple facts that a) people still remember and are sore from 1999/2000 and b) stocks are not cheap on trailing 5y/10y avg earnings and c) no consumer equals no spending equals no growth.

Think it through!

Show me the next possible logical bubble and I'll gladly change my mind (and buy buckets of equities in it)! But stocks, my friends, are not it. Can someone say 16 year secular bear market starting 2000?

(Hint: you do not have a bull market when after 6 years the Dow is barely even, S&P still down, and NASDAQ down over 50%!)

"Money will migrate out of real estate and back into equities."

++++++++++++

I think this is what the Feds are hoping, but IMHO there are a couple of problems. First, a lot of Boomers who got burned in the 2001 stock market collapse put their remaining money into real estate; they're the ones who bought their second homes as investments. Now, as the housing bubble collapses, these speculators are about to lose some if not all of their money (depending on how they financed their purchases). My guess is they will keep their few remaining dolalrs in cash and bonds for their retirement.

As for the under-40 generations, it's been reported they're so far in debt they don't have the money to invest on stocks.

So who's gonna be investing in the stock market in the future?

Post a Comment