It's not "different this time". It never is.

It's not "different this time". It never is.

Hat-tip to patrick.net for the link

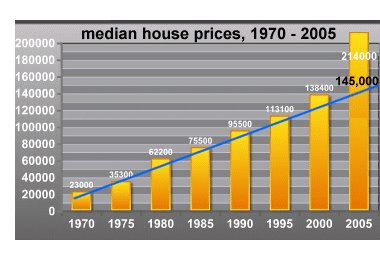

The trendline suggests that the median price of a house will fall from $214,000 to about $145,000 in the next few years--a 32% decline.

There is other evidence to support this valuation target. If you consult the inflation calculator on the Bureau of Labor Statistics page, you'll find that inflation has risen from 1990 to 2006 by 52%. That is, $1 in 1990 is worth $1.52 in today's currency. (Never mind inflation has been understated for years--that's another story I've covered elsewhere.)

That means the median house price of $95,500 in 1990 would equal $145,160 in today's money--remarkably close to the trendline prediction of $145,000.

April 03, 2006

We have our number - just follow the trendline

![]()

![]()

Subscribe to:

Post Comments (Atom)

40 comments:

they told me it's different this time. all the numbers don't matter anymore

twib, that's all well and good until the hypothetical $350k owner tries to sell, and nobody who wants that location/size/market can pay $350k for it. If you try to flip it in 5 years, and you're underwater relative to the 225k "realistic" price...

especially once you factor in broker fees and other fun stuff.

twib - decent arguement but do you know what's going on?

Looking at the price of something in terms of a payment is a losers' game and a great way to stay poor. This game will come to an end quickly when banks refuse to loan money at the payment terms. So what if a $350k house has a $2k payment? If the bank doesn't think it's worth $350k you won't get the loan to make the $2k monthly payment.

Plus interest rates today are on the lower end of "historically low". Just because the payment is less doens't mean the purchase price can be any greater.

The chart shows exactly what has happened - irrational idiots looking at payments instead of purchase prices have pushed the market to it's breaking point.

And remember that many of those idiots have IO, or some wierd hybrid ARM loans. When the resets hit you will see a mess of houses that these folks can't afford.

only a true idiot, a financial dolt, would look at the daily/monthly/annual cost of financing an asset purchase, versus the price of the asset.

But that is indeed where we are, a sea of idiots

reminds me once of when I went to go buy a car. I go to the dealer and I tell him I want to buy his car, and ask what he can sell it to me for. He asks me what I want to pay a month.

I tell him that's meaningless, I want to talk to him about how much cash I'm going to give him for the car.

He says I have to tell him how much a month I want to pay.

See the game? The dealer could get me to my number any way he could - a 7 year vs. a 3 year loan. change the interest rate. Whatever.

But at the end of the day, he wanted me to pay the highest possible price for the asset.

I told him I wanted to pay $1 a month.

So we got by that game, and talked about the price of the asset. As we should have. As anyone should have. And as many don't.

Doomed to poverty. Doomed to Chapter 11.

TWIB, although I understand your point, I respectfully disagree that looking at monthly costs is an accurate LONG TERM assessment of affordability.

Remember the old adage of "house can be 2.5 times your income". Thus if I make 80K a year I can afford a $200k house.

Looking at the monthly cost gets a lot of people into trouble. It's easy to afford a $2000 mortgage for above guy when he's doing I/O. What happens in a couple years when it readjusts and principle payments began? Suddendly the $2000 a month payment (readily affordable) has jumped to $2700. What if the expected job promotion didn't materialize or a recession hits and the guy is now jobless?

What about hurricane in some cases doubling the cost of insurance? Energy costs? Etc....

That my friend is why looking at payment is short sighted. Buy a house with a purchase price that you can live with and then there is less worry about the variable costs.

(On a side note, what car do you think would be most popular if people were required to pay cash for cars? I'd bet on seeing 5 people stuffed in a Kia Rio instead of the 2 per Tahoe that is common today).

Why do are some many condos are being built? You can stack 10 houses on a piece of land makeing the land cost minimal. The cost of the actual building is cheap compared to the selling price of the unit. Your profit on a $500,000 condo will be aroung 65%($325,000 is quite a nice profit per unit). Building materials didnt appreciate at the same level as housing due to the lower interest rates and alot of labor is comming from illegals looking for work. Condos will take the biggest hit, I seen it before when I was in construction and built condos in the late 80's that sold for $200,000 one year and steadily dropped untill they were selling for $50,000 and I never worked in building construction again. I would never buy a condo at the price I could buy a real house for!!

On a different note than the current thread of discussion, I bet that there is going to be a small bubble from all this in state/local government tax receipts. They have been happily going along ratcheting up property tax values and tax receipts to take advantage of the housing boom and planning/depending on that revenue for the future. It is going to be ugly when the housing values start crashing. And this is going to be precisely when people are going to need state/local government services to help them out.

I imagine the local banks are going to be in a similar world of hurt with a ton of bad loans coming in, just when people are going to need the liquidity. This'll probably happen even if they have sold off all their mortgages as mortgage backed securities..

foobecca is correct. Low mortgage rates should have made housing cheaper for all but they have had the opposite effect - more expensive for all.

Car prices are down the past couple years adjusted for inflation. Just because the average transaction price has risen doesn't mean the real price has risen. People afforded more expensive cars with cheap financing and they are doing the same with houses to the detriment of their financial health.

Twib,

There are several flaws with your numbers:

- There is no mortgage broker on earth that can get a 5.5% 30-year fixed at 100% financing. The best you could hope for is a 80/20 where the second (20 part) carries a higher interest.

- A 5.5% 30-year fixed at 100% financing on $350k is $1,987, but that's just principal/interest. What about property tax, insurance? Assuming 1% tax and $100 insurance, your payment would be looking closer to $2,400.

To look at historical mortgage rates means you need to also consider historical lending practices. Lenders were much stricter before, some requiring 20% down and most requiring that monthly payment didn't exceed 25% gross income. By that logic, given a $2,400 month mortgage, the household income requirement would have been $115,200/year. In some overpriced areas like Las Vegas, if these rules were enforced 90%+ of the population wouldn't qualify for a loan.

But I agree that if you find a house that you truly love, and you plan on spending a long time there (>15 years), then you are right.

On another note, if speculators and flippers could do the same with autos, they would. Could you imagine, going to the dealership and the lots are cleared? And the car flipper is trying to sell you a 2006 Maxima for $96,000?

Something similar happened with the Mustang and the Miata back in the early 90s, but it was short lived. I remember hearing about people buying up a bunch of Miatas, then trying to flip them for $10k over MSRP.

I can't speak for others, but I'm actually quite optimistic that a housing price correction is imminent.

My problem is the complete lack of logic that made this housing bubble possible -- the loose lending standards, the flippers, the realtors who spin lies that the rapid appreciation is normal. I hope it all goes away soon.

TWIB:

You are failing to understand a point. Lower rates should not lead to higher prices. Using that logic higher rates should lead to higher prices.

The only way lower rates might affect prices is driving more people into the market where traditional supply/demand take over. Once the stimulus is removed the prices will fall back to where they should have been.

What kind of dumbass finances a car for more than 60 months? Car loans are the first foot into a grave of financial servitude....plus all these dumbasses with car loans that trade in after 20 months of a 60 month loan and have underwater balances applied to their new car. Especially do not pity those who buy gaudy SUVs and then cannot afford the gas.

Dammit, I meant "higher rates should lead to lower prices" in my above post.

"Median price will fall to 145K"

I came to a similar conclusion after viewing this chart:

"Home Prices Go Parabolic"

http://www.chartoftheday.com/20060331.htm?T

For each subsequent steeper uptrend since 1997, you can basically plot the reason on this chart:

1997 - change in capital gains tax law

2002 - historically low interest rates

2004 - prevalence of creative mortgages

Drawing a long-term uptrend line from previous lows would indicate a reasonable 2006 median price between 140k and 160k.

Considering median individual income is ~42k, and household income is ~60k, this also lends credibility to the 140-160 appropriate home price; considering 3 X annual income as a correct financing metric.

prof_investor_40

Lower rates lead to higher prices if there is a fixed supply of of something. People don't buy houses as an "asset", maybe they should, but they are pricing it on affordability. If they can afford more of a house, they buy more.

There are't an infinite number of houses to meet the increased demand, so the prices go up. The actual cost to build the house wouldn't have gone up much...the profits accrue to the landowner, or existing house owner.

If rates go up, then houses would go down in price. Same process works in reverse. For people who bought at the "top", it's no problem IF they have a long term mortgage, or don't have to sell (move etc.).

Just because they are underwater on their house doesn't mean they default. Especially if their payments are still fixed at low levels due to a fixed mortgage.

Problem is many speculators bought houses planning to flip them. If prices stop rising they have to finance them and don't have the money to do that. So they all sell at once and it floods the market. Meanwhile people in teaser rate / high risk mortgages also can't afford new payments. So they dump too. The economy slows down and people lose their jobs...they dump too. Kind of a perfect storm.

Hey Keith,

Here's another one (three postings up):

"Anonymous said...

Very nice! I found a place where you can

make some nice extra cash secret shopping. Just go to the site below

and put in your zip to see what's available in your area.

I made over $900 last month having fun!

make extra money

Monday, April 03, 2006 12:23:40 PM"

Is there some way to keep these hucksters off the site?

ok, everyone who doesn't care about the PRICE they pay for an asset, only the MONTHLY PAYMENT on the asset. Here's the deal:

I will offer to give anyone $10,000, cold hard cash. But they must pay me $72,000 over the next 30 years, only $200 a month!

So, everyone, anyone, can have $10,000 right now, today. For only $200 a month!

If you're interested, just say the word and we'll draw up a contract. If you'd like, we can get your payment down to only $100 a month too, and POW, you get $10,000 large handed to you asap!

This realtor scares me. She has pierced into my soul, and is trying to draw out my inner flipper!!?? NO.... PLEASE... IT'S TOO STRONG... HELP...!

panicearly:

The modern incantation of the mortgage interest deduction started with the Tax Reform Act of 1986. I'm not sure how far back it really goes, however.

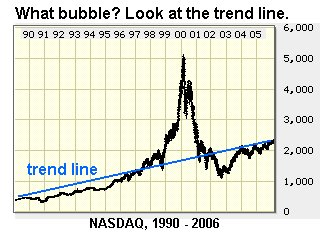

It is very common with plotted price charts, (such as this one), that a great deal of time is spent BELOW the trend.

Price movement is very likely to "overshoot" to the downside and return back UP to the trend.... in a decade.

oy vey!

for the love of statistical sensibility, take the damn logarithms!!

it is almost always dumb to plot a long-time series in nominal dollars without taking logarithms.

A straight line on a plot with a logarithmic y-axis (price) and linear in time, will show a straight line for a fixed *percentage per year* return. That is what economic sense means, and lets you compare fairly against bonds and inflation and things like that.

Same thing for Nasdaq.

Please please please.

It is logical for the price of any capital good to vary inversely with the interest rate. For a bond, the price is the inverse of the interest rate by definition. For other capital goods, you have yield on investment - earnings in case of stocks, rents (either actual or imputed) in the case of housing. These compete with bonds for investment. Thus their price will go up and down in the same direction as bonds - inversely to the interest rate. Economics 101.

I have been following a site now for almost 2 years and I have found it to be both reliable and profitable. They post daily and their stock trades have been beating

the indexes easily.

Take a look at Wallstreetwinnersonline.com

RickJ

Hello Friend! I just came across your blog and wanted to

drop you a note telling you how impressed I was with

the information you have posted here.

Keep up the great work, you are providing a great resource on the Internet here!

If you have a moment, please make a visit to my arm mortgage rates site.

Good luck in your endeavors!

Hello Friend! I just came across your blog and wanted to

drop you a note telling you how impressed I was with

the information you have posted here.

Keep up the great work, you are providing a great resource on the Internet here!

If you have a moment, please make a visit to my arm mortgage rates site.

Good luck in your endeavors!

Hey Fellow, you have a top-notch blog here!

If you have a moment, please have a look at my automobile insurance florida site.

Good luck!

Your blog I found to be very interesting!

I just came across your blog and wanted to

drop you a note telling you how impressed I was with

the information you have posted here.

I have a automobile insurance rental cars

site.

Come and check it out if you get time :-)

Best regards!

Hi there Blogger, a real useful blog.Keep with the good work.

If you have a moment, please visit my automobile insurance ratings site.

I send you warm regards and wishes of continued success.

Hey Fellow, you have a top-notch blog here!

If you have a moment, please have a look at my automobile no fault insurance site.

Good luck!

Hi Blogger, I found your blog quite informative.

I just came across your blog and wanted to

drop you a note telling you how impressed I was with it.

I give you my best wishes for your future endeavors.

If you have a moment, please visit my auto loans interest rates site.

Have a great week!

Hi there Blogger, a real useful blog.Keep with the good work.

If you have a moment, please visit my automotive insurance quotes site.

I send you warm regards and wishes of continued success.

Hi there Blogger, a real useful blog.Keep with the good work.

If you have a moment, please visit my bad bankruptcy credit mortgage site.

I send you warm regards and wishes of continued success.

Hi there Blogger, a real useful blog.Keep with the good work.

If you have a moment, please visit my bad california credit loan mortgage site.

I send you warm regards and wishes of continued success.

Hi there Blogger, a real useful blog.Keep with the good work.

If you have a moment, please visit my bad california credit loan mortgage site.

I send you warm regards and wishes of continued success.

A fantastic blog yours. Keep it up.

If you have a moment, please visit my stock beta calculation site.

I send you warm regards and wish you continued success.

Hi Fellow! I was just searching blogs,and I found yours! I like it!

If you have a moment, please visit my brick nj automobile insurance business site.

Good luck!

Hey, you have a great blog here! I'm definitely going to bookmark you!

I have a bad credit loan mortgage need site.

Come and check it out if you get time :-)

Greetings.

Hi Friend! You have a great blog over here!

Please accept my compliments and wishes for your happiness and success!

If you have a moment, please take a look at my calgary motorcycle insurance site.

Have a great day!

Hi Blogger, I found your blog quite informative.

I just came across your blog and wanted to

drop you a note telling you how impressed I was with it.

I give you my best wishes for your future endeavors.

If you have a moment, please visit my california automobile insurance site.

Have a great week!

keith,

I saw your post

regarding best internet make money online .

You are welcome to place a link to

your blog or website on my high

traffic website for free. See:

http://www.thefreeadforum.com

The Free Ad Forum is a forum where you may

post your permanent search engine friendly ads daily for

free. I hope you take advantage of this free advertising

opportunity, We have a special section just for best internet make money online .

Thank you,

John,

http://www.thefreeadforum.com

The Free Advertising Forum.

Post a Comment